Launch Interactive Tool How to Think About Tax Competition

Executive Summary

The TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. Foundation’s State Business Tax Climate Index enables business leaders, government policymakers, and taxpayers to gauge how their states’ tax systems compare. While there are many ways to show how much is collected in taxes by state governments, the Index is designed to show how well states structure their tax systems and provides a road map for improvement.

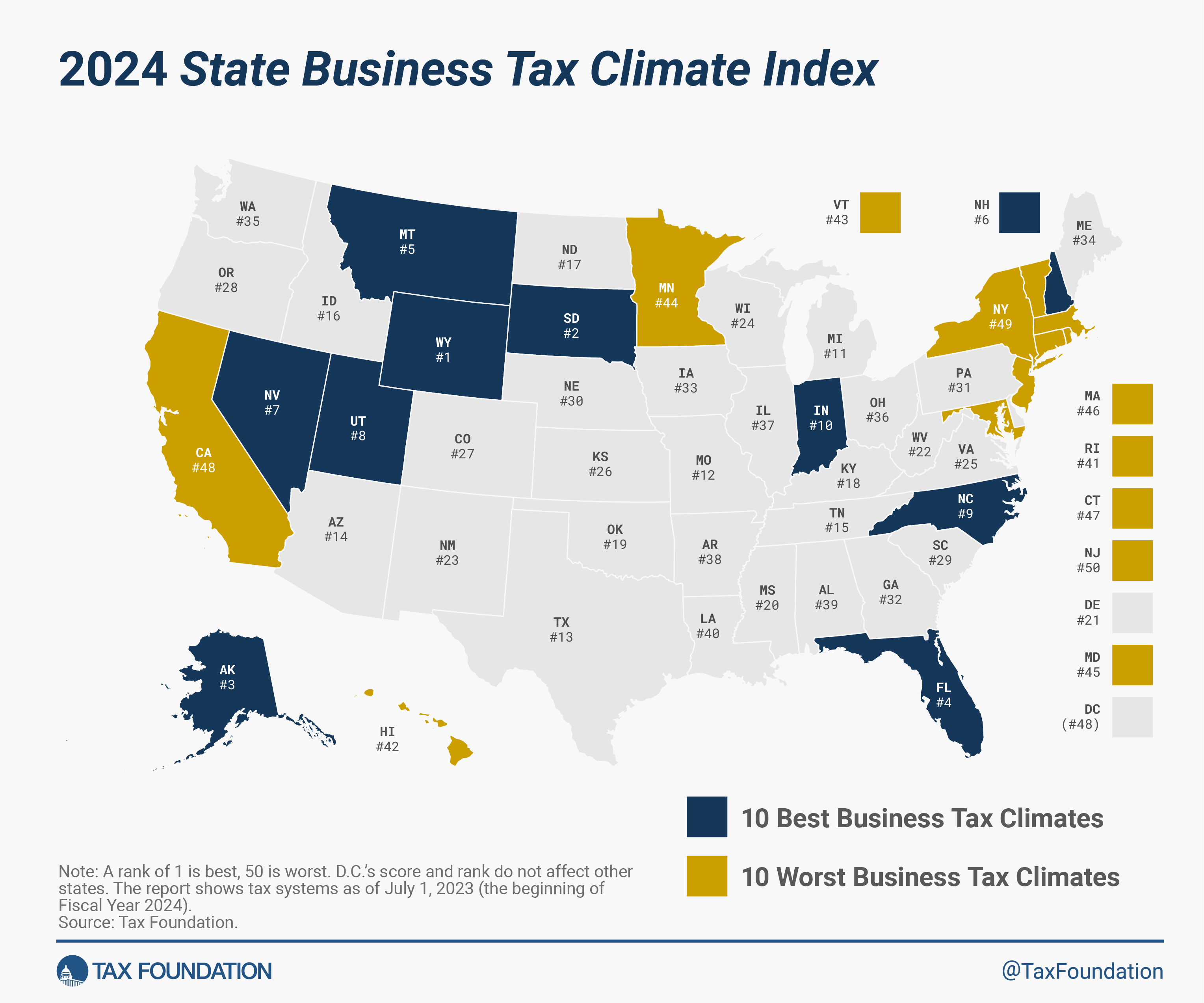

The 10 best states in this year’s Index are:

The absence of a major tax is a common factor among many of the top 10 states. Property taxes and unemployment insurance taxes are levied in every state, but there are several states that do without one or more of the major taxes: the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. , the individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S. , or the sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding. . Nevada, South Dakota, and Wyoming have no corporate or individual income tax (though Nevada imposes gross receipts taxes); Alaska has no individual income or state-level sales tax; Florida has no individual income tax; and New Hampshire and Montana have no sales tax.

This does not mean, however, that a state cannot rank in the top 10 while still levying all the major taxes. Indiana and Utah, for example, levy all the major tax types but do so with low rates on broad bases.

The 10 lowest-ranked, or worst, states in this year’s Index are:

- Rhode Island

- Hawaii

- Vermont

- Minnesota

- Maryland

- Massachusetts

- Connecticut

- California

- New York

- New Jersey

The states in the bottom 10 tend to have a number of afflictions in common: complex, nonneutral taxes with comparatively high rates. New Jersey, for example, is hampered by some of the highest property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services. burdens in the country, has the highest-rate corporate income taxes in the country, and has one of the highest-rate individual income taxes. Additionally, the state has a particularly aggressive treatment of international income, levies an inheritance taxAn inheritance tax is levied upon an individual’s estate at death or upon the assets transferred from the decedent’s estate to their heirs. Unlike estate taxes, inheritance tax exemptions apply to the size of the gift rather than the size of the estate. , and maintains some of the nation’s worst-structured individual income taxes.

Table 1. 2024 State Business Tax Climate Index Ranks and Component Tax Ranks

| State | Overall Rank | Corporate Tax Rank | Individual Income Tax Rank | Sales Tax Rank | Property Tax Rank | Unemployment Insurance Tax Rank |

|---|---|---|---|---|---|---|

| Alabama | 39 | 19 | 33 | 50 | 17 | 15 |

| Alaska | 3 | 26 | 1 | 5 | 27 | 48 |

| Arizona | 14 | 22 | 9 | 41 | 11 | 10 |

| Arkansas | 38 | 28 | 37 | 44 | 24 | 24 |

| California | 48 | 45 | 49 | 47 | 22 | 30 |

| Colorado | 27 | 7 | 13 | 40 | 38 | 44 |

| Connecticut | 47 | 30 | 46 | 23 | 50 | 26 |

| Delaware | 21 | 50 | 43 | 2 | 6 | 1 |

| Florida | 4 | 11 | 1 | 19 | 13 | 4 |

| Georgia | 32 | 9 | 35 | 28 | 28 | 34 |

| Hawaii | 42 | 18 | 47 | 26 | 31 | 41 |

| Idaho | 16 | 27 | 17 | 11 | 2 | 47 |

| Illinois | 37 | 43 | 14 | 39 | 45 | 42 |

| Indiana | 10 | 12 | 16 | 18 | 3 | 25 |

| Iowa | 33 | 29 | 22 | 15 | 41 | 32 |

| Kansas | 26 | 21 | 27 | 29 | 18 | 16 |

| Kentucky | 18 | 15 | 18 | 13 | 23 | 46 |

| Louisiana | 40 | 34 | 29 | 48 | 21 | 13 |

| Maine | 34 | 35 | 26 | 8 | 46 | 29 |

| Maryland | 45 | 33 | 45 | 34 | 42 | 43 |

| Massachusetts | 46 | 36 | 44 | 14 | 47 | 50 |

| Michigan | 11 | 20 | 12 | 12 | 26 | 7 |

| Minnesota | 44 | 47 | 42 | 31 | 32 | 31 |

| Mississippi | 20 | 8 | 19 | 25 | 37 | 5 |

| Missouri | 12 | 3 | 20 | 30 | 9 | 3 |

| Montana | 5 | 23 | 28 | 3 | 19 | 22 |

| Nebraska | 30 | 31 | 32 | 9 | 40 | 9 |

| Nevada | 7 | 25 | 5 | 45 | 4 | 45 |

| New Hampshire | 6 | 44 | 10 | 1 | 43 | 40 |

| New Jersey | 50 | 48 | 48 | 43 | 44 | 37 |

| New Mexico | 23 | 13 | 36 | 35 | 1 | 11 |

| New York | 49 | 24 | 50 | 42 | 49 | 39 |

| North Carolina | 9 | 5 | 15 | 20 | 12 | 6 |

| North Dakota | 17 | 10 | 21 | 32 | 7 | 14 |

| Ohio | 36 | 39 | 40 | 36 | 5 | 12 |

| Oklahoma | 19 | 4 | 24 | 38 | 15 | 2 |

| Oregon | 28 | 49 | 41 | 4 | 20 | 38 |

| Pennsylvania | 31 | 41 | 23 | 16 | 14 | 21 |

| Rhode Island | 41 | 40 | 31 | 22 | 35 | 49 |

| South Carolina | 29 | 6 | 30 | 33 | 36 | 27 |

| South Dakota | 2 | 1 | 1 | 27 | 30 | 35 |

| Tennessee | 15 | 42 | 6 | 46 | 33 | 20 |

| Texas | 13 | 46 | 7 | 37 | 39 | 8 |

| Utah | 8 | 14 | 11 | 21 | 8 | 17 |

| Vermont | 43 | 38 | 39 | 17 | 48 | 18 |

| Virginia | 25 | 16 | 34 | 10 | 29 | 36 |

| Washington | 35 | 37 | 8 | 49 | 25 | 19 |

| West Virginia | 22 | 17 | 25 | 24 | 10 | 33 |

| Wisconsin | 24 | 32 | 38 | 6 | 16 | 28 |

| Wyoming | 1 | 1 | 1 | 7 | 34 | 23 |

| District of Columbia | 48 | 30 | 48 | 38 | 50 | 38 |

Source: Tax Foundation.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

SubscribeNotable Ranking Changes in this Year’s Index

Arizona

Arizona transitioned from a two-bracket, graduated-rate individual income tax system with a top rate of 2.98 percent to a flat taxAn income tax is referred to as a “flat tax” when all taxable income is subject to the same tax rate, regardless of income level or assets. rate of 2.5 percent, becoming one of the 11 states with a flat individual income tax structure. Among those 11 states, Arizona now has the lowest individual income tax rate. This major development helped the state improve seven places on the individual income tax component and five places overall, from 19th to 14th.

Colorado

Colorado maintained its already competitive 7th-place standing on the individual tax component by reducing the flat rate to 4.4 percent, but the state’s overall ranking fell from 21st to 27th due to notable improvements in other states, including Mississippi and Wisconsin.

Idaho

In January 2023, Idaho moved to a flat individual income tax structure, consolidating four brackets with a top marginal rate of 6 percent into a single rate of 5.8 percent while also reducing its corporate income tax rate to 5.8 percent. This was enough to improve Idaho’s individual tax component ranking by two places, but Idaho’s overall ranking fell by one due to Arizona improving from 19th to 14th.

Iowa

Iowa witnessed significant changes in its tax landscape this year. Notably, the state reduced its top marginal individual income tax rate from 8.53 to 6.0 percent and simplified its rate schedule by consolidating nine brackets into four. The state is on its way to further reduce individual income tax rates and transition to a flat rate of 3.9 percent by 2026. Additionally, Iowa eliminated the marriage penaltyA marriage penalty is when a household’s overall tax bill increases due to a couple marrying and filing taxes jointly. A marriage penalty typically occurs when two individuals with similar incomes marry; this is true for both high- and low-income couples. in its individual income tax brackets by doubling the bracket widths for married couples filing jointly. On the corporate side, Iowa’s three-bracket corporate income tax was consolidated into a two-bracket tax, with the top rate decreasing from 9.8 to 8.4 percent. Subject to revenue availability, future reforms target a flat corporate income tax rate of 5.5 percent. These reforms signify a concerted effort by Iowa lawmakers to provide tax relief to residents and enhance the overall competitiveness of the tax system. As a result, Iowa’s overall ranking improved from 38th to 33rd.

Louisiana

In June 2023, Louisiana lawmakers passed legislation that would have phased out the state’s franchise tax, which is a capital stock tax that disincentivizes investment in the state. Phasing out this inefficient tax would have been a positive development, but the measure was vetoed by the governor. Nevertheless, S.B. 161, enacted in 2021, reduced the franchise tax rate from 0.3 to 0.275 percent this year, improving the state’s ranking on the property tax component from 22nd to 21st. Other recently enacted reforms, described elsewhere, are not reflected in this year’s Index due to effective dates after July 1, 2023.

Massachusetts

Massachusetts fell further than any other state in the overall rankings this year, sliding 12 places since last year. This decline in tax competitiveness is due to the adoption of Question 1 in November 2022, which amended the state’s constitution to move from a single-rate to a graduated-rate income tax by imposing a 4 percent surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services. on income over $1 million, raising the top marginal individual income tax rate from 5 to 9 percent. While the $1 million threshold at which the surtax kicks in is indexed to inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power. , the surtax imposes a sizeable marriage penalty that the Commonwealth lacked previously. This policy change represents a stark contrast from the recent reforms to reduce rates while consolidating brackets in many other states. Simultaneously, a new payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue. —the implementation of which had previously been postponed—went into effect this year. Massachusetts’s decline in tax competitiveness is evidenced by its 33-place decline in the individual tax component ranking, falling from 11th to 44th in just one year.

Minnesota

Minnesota ranks in the bottom half of states on each component of the Index. The state’s corporate income tax score is, in part, weighed down by the new election to add Global Intangible Low-Taxed Income (GILTI) to the corporate tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates. . Generally, states should avoid taxing GILTI, as state taxation should stop at the water’s edge, and taxing GILTI makes it more expensive for corporations to operate in a state for reasons having nothing to do with their activities in that state. Now, Minnesota ranks 47th on the corporate tax component, a loss of four positions compared to last year, and 44th overall.

Mississippi

Mississippi’s ranking improved from 27th to 20th overall. The state improved from 13th to 8th on the corporate tax component, due to the adoption of permanent full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. for qualified investments in machinery and equipment. This policy change, which thus far has been adopted only in Oklahoma and Mississippi, is the result of H.B. 1733, which was enacted in March 2023 and is retroactively effective as of January 1, 2023. The implementation of a flat individual income tax drove a seven-place improvement on the individual income tax component, from 26th to 19th. The Magnolia State will begin reducing the rate of its individual income tax next year, which will yield further improvements in the Index, and is slowly phasing out its franchise tax.

Missouri

With the enactment of S.B. 3 in October 2022, Missouri reformed its individual income tax structure to provide tax relief to residents, reducing the top marginal rate from 5.3 to 4.95 percent while consolidating nine brackets into seven. As a result, Missouri’s individual tax component ranking improved by one place, from 21st to 20th. If certain conditions regarding the state’s net revenues are satisfied in future years, the rates will be further reduced.

North Dakota

North Dakota reduced its top marginal individual income tax rate from 2.9 to 2.5 percent and established a wide zero-tax bracketA tax bracket is the range of incomes taxed at given rates, which typically differ depending on filing status. In a progressive individual or corporate income tax system, rates rise as income increases. There are seven federal individual income tax brackets; the federal corporate income tax system is flat. . The state now has the lowest top marginal rate among those states that tax wage and salary income. As a result, North Dakota became more competitive on the individual income tax component and improved seven places, from 28th to 21st.

Oklahoma

Oklahoma improved in the rankings again this year, thanks to a continued emphasis on tax reform. Specifically, the state saw gains on the individual tax component by eliminating the marriage penalty. On the property tax front, Oklahoma’s split roll ratio has narrowed, and the state repealed its capital stock tax, causing the property tax component ranking to soar from 30th to 15th. By adopting permanent full expensing in 2022, Oklahoma maintained its 4th-place standing on the corporate tax component while other states became less competitive by remaining conformed to the phaseout of the federal bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. allowance under Section 168(k), with only 80 percent bonus depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment. offered in 2023, down from 100 percent in 2022. Overall, Oklahoma now ranks 19th, a gain of four positions compared to last year. The governor has called for a special session to commence in October 2023. Any changes that may result could be reflected in the next Index.

Pennsylvania

Pennsylvania’s corporate net income tax was reduced by one percentage point, from 9.99 to 8.99 percent, effective January 1, 2023. This change is the result of H.B. 1342, enacted in July 2022, which also prescribes future reductions of 0.5 percentage points each year until the rate reaches 4.99 percent in 2031. This year’s rate reduction helped Pennsylvania improve from 33rd to 31st overall and from 42nd to 41st on the corporate tax component.

Rhode Island

S.B. 928, enacted in June 2023, exempts from taxation the first $50,000 of each taxpayer’s otherwise taxable tangible personal property for calendar year 2023. As a result, Rhode Island’s property tax component ranking improved from 41st to 35th, and the state’s overall ranking improved from 42nd to 41st.

South Dakota

South Dakota, which does not have an individual or corporate income tax, enacted H.B. 1137 in March 2023, trimming its sales tax rate from 4.5 to 4.2 percent, effective July 1, 2023. This change improved South Dakota’s sales tax component ranking by seven places, from 34th to 27th, but this change was not enough to improve the state’s overall ranking, which is already 2nd in the country.

West Virginia

In March 2023, H.B. 2526 was enacted in West Virginia, reducing the state’s individual income tax rates across the board, including reducing the top marginal rate from 6.5 to 5.12 percent, retroactive to January 1, 2023. This law also established triggers to reduce future tax rates, subject to revenue availability. These changes helped improve the state’s ranking on the individual income tax component from 29th to 25th. However, with other states continuing to improve, West Virginia has fallen two places overall, from 20th to 22nd.

Table 2. State Business Tax Climate Index (2014–2024)

| State | 2014 Rank | 2015 Rank | 2016 Rank | 2017 Rank | 2018 Rank | 2019 Rank | 2020 Rank | 2021 Rank | 2022 Rank | 2023 Rank | 2023 Score | 2024 Rank | 2024 Score | 2023-2024 Rank Change | 2023-2024 Score Change |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama | 40 | 40 | 41 | 38 | 39 | 41 | 40 | 40 | 39 | 41 | 4.56 | 39 | 4.60 | 2 | 0.04 |

| Alaska | 4 | 4 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 3 | 7.25 | 3 | 7.14 | 0 | -0.11 |

| Arizona | 27 | 26 | 23 | 24 | 24 | 23 | 22 | 23 | 24 | 19 | 5.26 | 14 | 5.45 | 5 | 0.19 |

| Arkansas | 41 | 42 | 45 | 42 | 43 | 46 | 44 | 46 | 43 | 40 | 4.57 | 38 | 4.62 | 2 | 0.05 |

| California | 48 | 48 | 48 | 48 | 49 | 48 | 48 | 48 | 48 | 48 | 3.56 | 48 | 3.64 | 0 | 0.08 |

| Colorado | 23 | 22 | 21 | 21 | 20 | 18 | 20 | 19 | 20 | 21 | 5.17 | 27 | 5.09 | -6 | -0.08 |

| Connecticut | 47 | 47 | 47 | 47 | 47 | 47 | 47 | 47 | 47 | 47 | 4.08 | 47 | 4.09 | 0 | 0.01 |

| Delaware | 18 | 15 | 15 | 22 | 22 | 14 | 15 | 16 | 16 | 16 | 5.31 | 21 | 5.29 | -5 | -0.02 |

| Florida | 5 | 5 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 4 | 6.85 | 4 | 6.84 | 0 | -0.01 |

| Georgia | 28 | 30 | 33 | 31 | 30 | 34 | 31 | 29 | 30 | 32 | 4.99 | 32 | 5.01 | 0 | 0.02 |

| Hawaii | 38 | 38 | 36 | 32 | 33 | 39 | 38 | 38 | 41 | 43 | 4.51 | 42 | 4.50 | 1 | 0.00 |

| Idaho | 15 | 18 | 18 | 18 | 18 | 20 | 19 | 20 | 17 | 15 | 5.33 | 16 | 5.40 | -1 | 0.07 |

| Illinois | 33 | 36 | 28 | 25 | 29 | 35 | 36 | 36 | 36 | 36 | 4.78 | 37 | 4.64 | -1 | -0.14 |

| Indiana | 10 | 10 | 10 | 9 | 9 | 10 | 10 | 9 | 9 | 9 | 5.63 | 10 | 5.60 | -1 | -0.02 |

| Iowa | 45 | 45 | 46 | 46 | 46 | 45 | 45 | 42 | 38 | 38 | 4.66 | 33 | 4.96 | 5 | 0.30 |

| Kansas | 22 | 24 | 26 | 27 | 28 | 31 | 34 | 33 | 23 | 25 | 5.13 | 26 | 5.10 | -1 | -0.03 |

| Kentucky | 35 | 35 | 34 | 37 | 37 | 19 | 18 | 17 | 18 | 18 | 5.27 | 18 | 5.30 | 0 | 0.02 |

| Louisiana | 32 | 33 | 38 | 45 | 45 | 42 | 43 | 41 | 42 | 39 | 4.62 | 40 | 4.59 | -1 | -0.04 |

| Maine | 30 | 34 | 35 | 36 | 35 | 28 | 29 | 32 | 34 | 35 | 4.90 | 34 | 4.94 | 1 | 0.04 |

| Maryland | 39 | 39 | 40 | 41 | 40 | 40 | 42 | 44 | 46 | 46 | 4.28 | 45 | 4.25 | 1 | -0.03 |

| Massachusetts | 26 | 28 | 27 | 28 | 25 | 30 | 35 | 35 | 35 | 34 | 4.92 | 46 | 4.14 | -12 | -0.77 |

| Michigan | 11 | 12 | 13 | 13 | 13 | 13 | 12 | 13 | 12 | 12 | 5.57 | 11 | 5.55 | 1 | -0.02 |

| Minnesota | 46 | 46 | 44 | 44 | 44 | 44 | 46 | 45 | 45 | 45 | 4.35 | 44 | 4.30 | 1 | -0.04 |

| Mississippi | 25 | 27 | 29 | 29 | 27 | 27 | 26 | 26 | 28 | 27 | 5.07 | 20 | 5.30 | 7 | 0.22 |

| Missouri | 14 | 16 | 19 | 15 | 15 | 15 | 14 | 11 | 11 | 11 | 5.59 | 12 | 5.55 | -1 | -0.04 |

| Montana | 6 | 6 | 6 | 6 | 6 | 5 | 5 | 5 | 5 | 5 | 6.07 | 5 | 6.02 | 0 | -0.05 |

| Nebraska | 36 | 29 | 30 | 30 | 34 | 25 | 28 | 30 | 31 | 31 | 5.02 | 30 | 5.01 | 1 | -0.01 |

| Nevada | 3 | 3 | 5 | 5 | 5 | 6 | 7 | 7 | 6 | 7 | 5.93 | 7 | 5.82 | 0 | -0.11 |

| New Hampshire | 8 | 7 | 7 | 7 | 7 | 7 | 6 | 6 | 7 | 6 | 5.95 | 6 | 5.93 | 0 | -0.03 |

| New Jersey | 49 | 49 | 50 | 49 | 50 | 50 | 50 | 50 | 50 | 50 | 3.37 | 50 | 3.43 | 0 | 0.06 |

| New Mexico | 21 | 23 | 24 | 26 | 26 | 24 | 24 | 21 | 26 | 22 | 5.16 | 23 | 5.18 | -1 | 0.02 |

| New York | 50 | 50 | 49 | 50 | 48 | 49 | 49 | 49 | 49 | 49 | 3.45 | 49 | 3.57 | 0 | 0.12 |

| North Carolina | 31 | 11 | 12 | 11 | 10 | 11 | 11 | 10 | 10 | 10 | 5.60 | 9 | 5.62 | 1 | 0.02 |

| North Dakota | 19 | 19 | 17 | 17 | 17 | 16 | 17 | 18 | 19 | 17 | 5.29 | 17 | 5.33 | 0 | 0.04 |

| Ohio | 42 | 41 | 42 | 39 | 41 | 37 | 37 | 37 | 37 | 37 | 4.72 | 36 | 4.74 | 1 | 0.02 |

| Oklahoma | 20 | 21 | 22 | 20 | 21 | 26 | 27 | 25 | 29 | 23 | 5.15 | 19 | 5.30 | 4 | 0.15 |

| Oregon | 9 | 9 | 9 | 10 | 11 | 9 | 8 | 15 | 22 | 24 | 5.14 | 28 | 5.07 | -4 | -0.07 |

| Pennsylvania | 37 | 37 | 37 | 33 | 36 | 36 | 33 | 34 | 32 | 33 | 4.99 | 31 | 5.01 | 2 | 0.02 |

| Rhode Island | 44 | 43 | 39 | 40 | 38 | 38 | 39 | 39 | 40 | 42 | 4.54 | 41 | 4.58 | 1 | 0.04 |

| South Carolina | 29 | 31 | 31 | 34 | 32 | 32 | 32 | 31 | 33 | 30 | 5.02 | 29 | 5.02 | 1 | -0.01 |

| South Dakota | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 2 | 7.43 | 2 | 7.46 | 0 | 0.03 |

| Tennessee | 24 | 25 | 25 | 23 | 23 | 29 | 30 | 27 | 14 | 14 | 5.44 | 15 | 5.43 | -1 | 0.00 |

| Texas | 12 | 13 | 11 | 12 | 12 | 12 | 13 | 12 | 13 | 13 | 5.51 | 13 | 5.48 | 0 | -0.03 |

| Utah | 7 | 8 | 8 | 8 | 8 | 8 | 9 | 8 | 8 | 8 | 5.64 | 8 | 5.62 | 0 | -0.01 |

| Vermont | 43 | 44 | 43 | 43 | 42 | 43 | 41 | 43 | 44 | 44 | 4.44 | 43 | 4.49 | 1 | 0.05 |

| Virginia | 16 | 17 | 20 | 19 | 19 | 21 | 23 | 24 | 25 | 26 | 5.07 | 25 | 5.11 | 1 | 0.03 |

| Washington | 13 | 14 | 14 | 14 | 14 | 17 | 16 | 14 | 15 | 29 | 5.03 | 35 | 4.90 | -6 | -0.13 |

| West Virginia | 17 | 20 | 16 | 16 | 16 | 22 | 21 | 22 | 21 | 20 | 5.21 | 22 | 5.18 | -2 | -0.03 |

| Wisconsin | 34 | 32 | 32 | 35 | 31 | 33 | 25 | 28 | 27 | 28 | 5.07 | 24 | 5.12 | 4 | 0.04 |

| Wyoming | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 7.76 | 1 | 7.72 | 0 | -0.04 |

| District of Columbia | 47 | 48 | 47 | 48 | 48 | 47 | 47 | 48 | 48 | 48 | 3.75 | 48 | 3.83 | 0 | 0.08 |

Source: Tax Foundation.

Recent and Scheduled Changes Not Reflected in the 2024 Index

Arkansas

As a result of H.B. 1045, enacted in April 2023, Arkansas is scheduled to phase out its throwback rule over time, eliminating it entirely by 2030. After Arkansas’s planned repeal of its throwback rule is complete, the state’s corporate tax component score will improve.

Georgia

On January 1, 2024, Georgia will transition from a graduated individual income tax with a top rate of 5.75 percent to a flat tax structure with a rate of 5.49 percent. Per H.B. 1437, enacted in April 2022, the rate could decrease to 4.99 percent by January 1, 2029, if certain revenue conditions are met, paired with substantial increases in personal exemptions. Both the rate reductions and the single-rate tax structure would improve Georgia’s ranking on the Index.

Indiana

House Bill 1001, enacted in May 2023, accelerated Indiana’s previously enacted tax rate reductions, reducing the individual income tax rate from 3.15 to 3.05 percent in 2024. The law also repealed previously enacted tax triggers, instead prescribing rate reductions to bring the rate to 3.0 percent in 2025, 2.95 percent in 2026, and 2.9 percent in 2027 and beyond. These rate reductions will improve Indiana’s score on the individual tax component in future years.

Iowa

Iowa’s recent comprehensive tax reforms will continue phasing in over time, further improving the state’s rankings as Iowa moves toward a flat individual income tax rate of 3.9 percent in 2026 and a flat corporate income tax with a target rate of 5.5 percent, subject to tax triggers.

Kentucky

House Bill 1 was signed into law in February 2023, reducing Kentucky’s flat individual income tax rate from 4.5 percent in 2023 to 4.0 percent starting in 2024, codifying a reduction that was triggered under the conditions established by H.B. 8, enacted in 2022. This scheduled rate reduction will improve Kentucky’s score on the individual tax component in the future.

Louisiana

House Bill 631, enacted in June 2023, repeals Louisiana’s complex and economically harmful throwout rule, effective January 1, 2024, leaving Maine as the only state to keep such a rule on the books. Additionally, with the enactment of H.B. 171 in May 2023, the state also removed the 200 transactions threshold for economic nexus for remote sellers. This means that only those with more than $100,000 in gross revenue in the state will be subject to sales tax collection and remittance obligations. These improvements will show up in the next edition of the Index, as they took effect after the July 1, 2023, snapshot date.

Michigan

Michigan’s flat individual income tax rate has been reduced from 4.25 to 4.05 percent for 2023, the automatic result of a 2015 law that prescribed tax rate reductions for any year, beginning in 2023, in which general fund revenue growth exceeds the rate of inflation growth. In March 2023, Attorney General Dana Nessel issued a legal opinion stipulating that the rate will revert back to 4.25 percent for 2024 and beyond. This opinion has sparked debate among legislators and stakeholders as to the intent and letter of the 2015 law and created uncertainty regarding the possibility of a near-term rate increase. If the rate reverts to 4.25 percent in 2024, Michigan’s score will be negatively affected.

Mississippi

Under HB 531, enacted in April 2022, Mississippi converted its graduated-rate individual income tax to a single-rate tax of 5 percent on taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income. exceeding $10,000, effective January 1, 2023. The flat rate is scheduled to decrease to 4.7 percent in 2024, 4.4 percent in 2025, and 4 percent in 2026. These reductions will further improve Mississippi’s ranking.

Montana

Montana was among the states to enact individual income tax cuts in 2021, reducing the top marginal rate from 6.9 percent in 2021 to 6.75 percent in 2022 and scheduling a future reduction, along with bracket consolidation and other structural reforms, for 2024. Originally, the 2021 law converted Montana’s seven marginal rates into two, with rates of 4.7 and 6.5 percent, effective in 2024. However, in March 2022, S.B. 121 was enacted, reducing the top marginal rate even further—to 5.9 percent—beginning in 2024. Although the lowest rate will rise to 4.7 percent in 2024, conforming to the federal standard deductionThe standard deduction reduces a taxpayer’s taxable income by a set amount determined by the government. It was nearly doubled for all classes of filers by the 2017 Tax Cuts and Jobs Act (TCJA) as an incentive for taxpayers not to itemize deductions when filing their federal income taxes. in 2025 will yield tax savings for lower-income taxpayers. This law also doubles the bracket widths for married filers, thereby removing the marriage penalty that currently exists in the state’s income tax code. These reforms will yield a favorable ranking change.

Nebraska

Nebraska has taken strides to improve its tax competitiveness in recent years and continued that work in 2023 by accelerating previously enacted individual and corporate income tax rate cuts and reducing rates further than originally planned. Legislative Bill 754, enacted in May 2023, will gradually phase down Nebraska’s top marginal individual and corporate income tax rates to 3.99 percent in 2027, with initial reductions of both top marginal rates to 5.84 percent in 2024, reaching that target rate three years earlier than initially anticipated. This new law also converts Nebraska’s graduated-rate corporate income tax into a single-rate tax in 2025 and consolidates Nebraska’s four marginal individual income tax rates into three starting in 2026. Assuming these reforms proceed as scheduled, Nebraska’s corporate and individual tax component scores will continue to improve.

New Hampshire

Senate Bill 189, enacted in July 2023, decouples New Hampshire from the business net interest limitation under IRC Section 163(j), thereby allowing businesses to fully deduct their interest expenses in the year those expenses are incurred, effective January 1, 2024. This change will improve New Hampshire’s score on the corporate tax component. Additionally, the state budget (H.B. 2), enacted in June 2023, accelerates the phaseout of New Hampshire’s tax on interest and dividends income, eliminating the tax by January 2025, rather than 2027. This will improve New Hampshire’s score on the individual tax component.

New Jersey

Assembly Bill 5323, enacted in July 2023, made several changes to New Jersey’s corporate income tax code, including reducing the taxation of GILTI from 50 to 5 percent, effective for privilege periods ending on or after July 31, 2023. This change will help New Jersey’s corporate tax component score in the future. However, that same law will also newly conform New Jersey to the 80 percent federal limitation on NOL carryforwards without adopting a corresponding unlimited recovery period included in federal law. Additionally, New Jersey’s 2.5 percent corporation business tax surcharge is scheduled to expire at the end of 2023, which would result in the reduction of New Jersey’s top marginal corporate income tax rate from 11.5 to 9 percent. If the surcharge is indeed allowed to expire, New Jersey’s corporate tax component score will improve in the future.

Oklahoma

House Bill 1040, enacted in May 2023, removes the marriage penalty from Oklahoma’s individual income tax brackets by adjusting the bracket threshold at which the top marginal rate kicks in to $14,400, making it double the threshold at which the top marginal rate kicks in for single filers. This change, which will improve Oklahoma’s individual component score, is applicable beginning in tax year 2024.

Pennsylvania

Under H.B. 1342, enacted in June 2022, Pennsylvania reduced its corporate net income tax rate from 9.99 to 8.99 percent on January 1, 2023. In 2024 and years thereafter, the rate will decrease by 0.5 percentage points until it reaches 4.99 percent at the beginning of 2031, transforming the nation’s second-highest corporate income tax rate into a much more competitive system of corporate taxation. As such, Pennsylvania’s corporate tax component score will continue to improve.

South Dakota

House Bill 1137, enacted in March 2023, reduced South Dakota’s sales tax rate from 4.5 to 4.2 percent, effective July 1, 2023, improving the state’s sales tax component score. However, this rate reduction is scheduled to expire on July 1, 2027, meaning this improvement in score might be short-lived.

West Virginia

In addition to reducing individual income tax rates across the board, retroactive to January 1, 2023, H.B. 2526, enacted in March 2023, established a set of triggers that could reduce rates further in future years, starting in 2025, subject to revenue availability. If future rates are reduced, West Virginia’s individual tax component score will improve.

Wisconsin

Assembly Bill 245, enacted in June 2023, repeals Wisconsin’s tangible personal property tax beginning with the January 1, 2024, property tax assessment. Since this change does not benefit taxpayers until after the July 1, 2023, snapshot date, this change was not reflected in the current Index but will improve Wisconsin’s property tax component score in the future.

Introduction

Taxation is inevitable, but the specifics of a state’s tax structure matter greatly. The measure of total taxes paid is relevant, but other elements of a state tax system can also enhance or harm the competitiveness of a state’s business environment. The State Business Tax Climate Index distills many complex considerations to an easy-to-understand ranking.

The modern market is characterized by mobile capital and labor, with all types of businesses, small and large, tending to locate where they have the greatest competitive advantage. The evidence shows that states with the best tax systems will be the most competitive at attracting new businesses and most effective at generating economic and employment growth. It is true that taxes are but one factor in business decision-making. Other concerns also matter–such as access to raw materials or infrastructure or a skilled labor pool–but a simple, sensible tax system can positively impact business operations with regard to these resources. Furthermore, unlike changes to a state’s health-care, transportation, or education systems, which can take decades to implement, changes to the tax code can quickly improve a state’s business climate.

It is important to remember that even in our global economy, states’ stiffest competition often comes from other states. The Department of Labor reports that most mass job relocations are from one U.S. state to another rather than to a foreign location.[1] Certainly, job creation is rapid overseas, as previously underdeveloped nations enter the world economy, though in the aftermath of federal tax reform, U.S. businesses no longer face the third-highest corporate tax rate in the world, but rather one in line with averages for industrialized nations.[2] State lawmakers are right to be concerned about how their states rank in the global competition for jobs and capital, but they need to be more concerned with companies moving from Detroit, Michigan, to Dayton, Ohio, than from Detroit to New Delhi, India. This means that state lawmakers must be aware of how their states’ business climates match up against their immediate neighbors and to other regional competitor states.

Anecdotes about the impact of state tax systems on business investment are plentiful. In Illinois early last decade, hundreds of millions of dollars of capital investments were delayed when then-Governor Rod Blagojevich (D) proposed a hefty gross receipts taxA gross receipts tax, also known as a turnover tax, is applied to a company’s gross sales, without deductions for a firm’s business expenses, like costs of goods sold and compensation. Unlike a sales tax, a gross receipts tax is assessed on businesses and apply to business-to-business transactions in addition to final consumer purchases, leading to tax pyramiding. .[3] Only when the legislature resoundingly defeated the bill did the investment resume. In 2005, California-based Intel decided to build a multibillion-dollar chip-making facility in Arizona due to its favorable corporate income tax system.[4] In 2010, Northrup Grumman chose to move its headquarters to Virginia over Maryland, citing the better business tax climate.[5] In 2015, General Electric and Aetna threatened to decamp from Connecticut if the governor signed a budget that would increase corporate tax burdens, and General Electric actually did so.[6] Anecdotes such as these reinforce what we know from economic theory: taxes matter to businesses, and those places with the most competitive tax systems will reap the benefits of business-friendly tax climates.

Tax competition is an unpleasant reality for state revenue and budget officials, but it is an effective restraint on state and local taxes. When a state imposes higher taxes than a neighboring state, businesses will cross the border to some extent. Therefore, states with more competitive tax systems score well in the Index because they are best suited to generate economic growth.

State lawmakers are mindful of their states’ business tax climates, but they are sometimes tempted to lure business with lucrative tax incentives and subsidies instead of broad-based tax reform. This can be a dangerous proposition, as the example of Dell Computers and North Carolina illustrates. North Carolina agreed to $240 million worth of incentives to lure Dell to the state. Many of the incentives came in the form of tax credits from the state and local governments. Unfortunately, Dell announced in 2009 that it would be closing the plant after only four years of operations.[7] A 2007 USA TODAY article chronicled similar problems other states have had with companies that receive generous tax incentives.[8]

Lawmakers make these deals under the banner of job creation and economic development, but the truth is that if a state needs to offer such packages, it is most likely covering for an undesirable business tax climate. A far more effective approach is the systematic improvement of the state’s business tax climate for the long term to improve the state’s competitiveness. When assessing which changes to make, lawmakers need to remember two rules:

- Taxes matter to business. Business taxes affect business decisions, job creation and retention, plant location, competitiveness, the transparency of the tax system, and the long-term health of a state’s economy. Most importantly, taxes diminish profits. If taxes take a larger portion of profits, that cost is passed along to either consumers (through higher prices), employees (through lower wages or fewer jobs), shareholders (through lower dividends or share value), or some combination of the above. Thus, a state with lower tax costs will be more attractive to business investment and more likely to experience economic growth.

- States do not enact tax changes (increases or cuts) in a vacuum. Every tax law will in some way change a state’s competitive position relative to its immediate neighbors, its region, and even globally. Ultimately, it will affect the state’s national standing as a place to live and to do business. Entrepreneurial states can take advantage of the tax increases of their neighbors to lure businesses out of high-tax states.

To some extent, tax-induced economic distortions are a fact of life, but policymakers should strive to maximize the occasions when businesses and individuals are guided by business principles and minimize those cases where economic decisions are influenced, micromanaged, or even dictated by a tax system. The more riddled a tax system is with politically motivated preferences, the less likely it is that business decisions will be made in response to market forces. The Index rewards those states that minimize tax-induced economic distortions.

Ranking the competitiveness of 50 very different tax systems presents many challenges, especially when a state dispenses with a major tax entirely. Should Indiana’s tax system, which includes three relatively neutral taxes on sales, individual income, and corporate income, be considered more or less competitive than Alaska’s tax system, which includes a particularly burdensome corporate income tax but no statewide tax on individual income or sales?

The Index deals with such questions by comparing the states on more than 120 variables in the five major areas of taxation (corporate taxes, individual income taxes, sales taxes, unemployment insurance taxes, and property taxes) and then adding the results to yield a final, overall ranking. This approach rewards states on particularly strong aspects of their tax systems (or penalizes them on particularly weak aspects), while measuring the general competitiveness of their overall tax systems. The result is a score that can be compared to other states’ scores. Ultimately, both Alaska and Indiana score well.

Literature Review

Economists have not always agreed on how individuals and businesses react to taxes. As early as 1956, Charles Tiebout postulated that if citizens were faced with an array of communities that offered different types or levels of public goods and services at different costs or tax levels, then all citizens would choose the community that best satisfied their particular demands, revealing their preferences by “voting with their feet.” Tiebout’s article is the seminal work on the topic of how taxes affect the location decisions of taxpayers.

Tiebout suggested that citizens with high demands for public goods would concentrate in communities with high levels of public services and high taxes while those with low demands would choose communities with low levels of public services and low taxes. Competition among jurisdictions results in a variety of communities, each with residents who all value public services similarly.

However, businesses sort out the costs and benefits of taxes differently from individuals. For businesses, which can be more mobile and must earn profits to justify their existence, taxes reduce profitability. Theoretically, businesses could be expected to be more responsive than individuals to the lure of low-tax jurisdictions. Research suggests that corporations engage in “yardstick competition,” comparing the costs of government services across jurisdictions. Shleifer (1985) first proposed comparing regulated franchises in order to determine efficiency. Salmon (1987) extended Shleifer’s work to look at subnational governments. Besley and Case (1995) showed that “yardstick competition” affects voting behavior, and Bosch and Sole-Olle (2006) further confirmed the results found by Besley and Case. Tax changes that are out of sync with neighboring jurisdictions will impact voting behavior.

The economic literature over the past 50 years has slowly cohered around this hypothesis. Ladd (1998) summarizes the post-World War II empirical tax research literature in an excellent survey article, breaking it down into three distinct periods of differing ideas about taxation: (1) taxes do not change behavior; (2) taxes may or may not change business behavior depending on the circumstances; and (3) taxes definitely change behavior.

Period one, with the exception of Tiebout, included the 1950s, 1960s, and 1970s and is summarized succinctly in three survey articles: Due (1961), Oakland (1978), and Wasylenko (1981). Due’s was a polemic against tax giveaways to businesses, and his analytical techniques consisted of basic correlations, interview studies, and the examination of taxes relative to other costs. He found no evidence to support the notion that taxes influence business location. Oakland was skeptical of the assertion that tax differentials at the local level had no influence at all. However, because econometric analysis was relatively unsophisticated at the time, he found no significant articles to support his intuition. Wasylenko’s survey of the literature found some of the first evidence indicating that taxes do influence business location decisions. However, the statistical significance was lower than that of other factors such as labor supply and agglomeration economies. Therefore, he dismissed taxes as a secondary factor at most.

Period two was a brief transition during the early- to mid-1980s. This was a time of great ferment in tax policy as Congress passed major tax bills, including the so-called Reagan tax cut in 1981 and a dramatic reform of the federal tax code in 1986. Articles revealing the economic significance of tax policy proliferated and became more sophisticated. For example, Wasylenko and McGuire (1985) extended the traditional business location literature to nonmanufacturing sectors and found, “Higher wages, utility prices, personal income tax rates, and an increase in the overall level of taxation discourage employment growth in several industries.” However, Newman and Sullivan (1988) still found a mixed bag in “their observation that significant tax effects [only] emerged when models were carefully specified.”

Ladd was writing in 1998, so her “period three” started in the late 1980s and continued up to 1998, when the quantity and quality of articles increased significantly. Articles that fit into period three begin to surface as early as 1985, as Helms (1985) and Bartik (1985) put forth forceful arguments based on empirical research that taxes guide business decisions. Helms concluded that a state’s ability to attract, retain, and encourage business activity is significantly affected by its pattern of taxation. Furthermore, tax increases significantly retard economic growth when the revenue is used to fund transfer payments. Bartik concluded that the conventional view that state and local taxes have little effect on business is false.

Papke and Papke (1986) found that tax differentials among locations may be an important business location factor, concluding that consistently high business taxes can represent a hindrance to the location of industry. Interestingly, they use the same type of after-tax model used by Tannenwald (1996), who reaches a different conclusion.

Bartik (1989) provides strong evidence that taxes have a negative impact on business start-ups. He finds specifically that property taxes, because they are paid regardless of profit, have the strongest negative effect on business. Bartik’s econometric model also predicts tax elasticities of -0.1 to -0.5 that imply a 10 percent cut in tax rates will increase business activity by 1 to 5 percent. Bartik’s findings, as well as those of Mark, McGuire, and Papke (2000), and ample anecdotal evidence of the importance of property taxes, buttress the argument for inclusion of a property index devoted to property-type taxes in the Index.

By the early 1990s, the literature had expanded sufficiently for Bartik (1991) to identify 57 studies on which to base his literature survey. Ladd succinctly summarizes Bartik’s findings:

The large number of studies permitted Bartik to take a different approach from the other authors. Instead of dwelling on the results and limitations of each individual study, he looked at them in the aggregate and in groups. Although he acknowledged potential criticisms of individual studies, he convincingly argued that some systematic flaw would have to cut across all studies for the consensus results to be invalid. In striking contrast to previous reviewers, he concluded that taxes have quite large and significant effects on business activity.

Ladd’s “period three” surely continues to this day. Agostini and Tulayasathien (2001) examined the effects of corporate income taxes on the location of foreign direct investment in U.S. states. They determined that for “foreign investors, the corporate tax rate is the most relevant tax in their investment decision.” Therefore, they found that foreign direct investment was quite sensitive to states’ corporate tax rates.

Mark, McGuire, and Papke (2000) found that taxes are a statistically significant factor in private-sector job growth. Specifically, they found that personal property taxes and sales taxes have economically large negative effects on the annual growth of private employment.

Harden and Hoyt (2003) point to Phillips and Gross (1995) as another study contending that taxes impact state economic growth, and they assert that the consensus among recent literature is that state and local taxes negatively affect employment levels. Harden and Hoyt conclude that the corporate income tax has the most significant negative impact on the rate of growth in employment.

Gupta and Hofmann (2003) regressed capital expenditures against a variety of factors, including weights of apportionmentApportionment is the determination of the percentage of a business’ profits subject to a given jurisdiction’s corporate income or other business taxes. U.S. states apportion business profits based on some combination of the percentage of company property, payroll, and sales located within their borders. formulas, the number of tax incentives, and burden figures. Their model covered 14 years of data and determined that firms tend to locate property in states where they are subject to lower income tax burdens. Furthermore, Gupta and Hofmann suggest that throwback requirements are the most influential on the location of capital investment, followed by apportionment weights and tax rates, and that investment-related incentives have the least impact.

Other economists have found that taxes on specific products can produce behavioral results similar to those that were found in these general studies. For example, Fleenor (1998) looked at the effect of excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections. differentials between states on cross-border shopping and the smuggling of cigarettes. Moody and Warcholik (2004) examined the cross-border effects of beer excises. Their results, supported by the literature in both cases, showed significant cross-border shopping and smuggling between low-tax states and high-tax states.

Fleenor found that shopping areas sprouted in counties of low-tax states that shared a border with a high-tax state, and that approximately 13.3 percent of the cigarettes consumed in the United States during FY 1997 were procured via some type of cross-border activity. Similarly, Moody and Warcholik found that in 2000, 19.9 million cases of beer, on net, moved from low- to high-tax states. This amounted to some $40 million in sales and excise tax revenue lost in high-tax states.

Although the literature has largely congealed around a general consensus that taxes are a substantial factor in the decision-making process for businesses, disputes remain, and some scholars are unconvinced.

Based on a substantial review of the literature on business climates and taxes, Wasylenko (1997) concludes that taxes do not appear to have a substantial effect on economic activity among states. However, his conclusion is premised on there being few significant differences in state tax systems. He concedes that high-tax states will lose economic activity to average or low-tax states “as long as the elasticity is negative and significantly different from zero.” Indeed, he approvingly cites a State Policy Reports article that finds that the highest-tax states, such as Minnesota, Wisconsin, and New York, have acknowledged that high taxes may be responsible for the low rates of job creation in those states.[9]

Wasylenko’s rejoinder is that policymakers routinely overestimate the degree to which tax policy affects business location decisions and that as a result of this misperception, they respond readily to public pressure for jobs and economic growth by proposing lower taxes. According to Wasylenko, other legislative actions are likely to accomplish more positive economic results because in reality, taxes do not drive economic growth.

However, there is ample evidence that states compete for businesses using their tax systems. A recent example comes from Illinois, where in early 2011 lawmakers passed two major tax increases. The individual income tax rate increased from 3 percent to 5 percent, and the corporate income tax rate rose from 7.3 percent to 9.5 percent.[10] The result was that many businesses threatened to leave the state, including some very high-profile Illinois companies such as Sears and the Chicago Mercantile Exchange. By the end of the year, lawmakers had cut deals with both firms, totaling $235 million over the next decade, to keep them from leaving the state.[11]

A new literature review, Kleven et al. (2019), summarizes recent evidence for tax-driven migration. Meanwhile, Giroud and Rauh (2019) use microdata on multistate firms to estimate the impact of state taxes on business activity, and find that C corporation employment and establishments have short-run corporate tax elasticities of -0.4 to -0.5, while pass-through entities show elasticities of -0.2 to -0.4, meaning that, for each percentage-point increase in the rate, employment decreases by 0.4 to 0.5 percent for C corporations subject to the corporate income tax, and by 0.2 to 0.4 percent within pass-through businesses subject to the individual income tax.

Measuring the Impact of Tax Differentials

Some recent contributions to the literature on state taxation criticize business and tax climate studies in general.[12] Authors of such studies contend that comparative reports like the State Business Tax Climate Index do not take into account those factors which directly impact a state’s business climate. However, a careful examination of these criticisms reveals that the authors believe taxes are unimportant to businesses and therefore dismiss the studies as merely being designed to advocate low taxes.

Peter Fisher’s Grading Places: What Do the Business Climate Rankings Really Tell Us? now published by Good Jobs First, criticizes four indices: The U.S. Business Policy Index published by the Small Business and Entrepreneurship Council, Beacon Hill’s Competitiveness Report, the American Legislative Exchange Council’s Rich States, Poor States, and this study. The first edition also critiqued the Cato Institute’s Fiscal Policy Report Card and the Economic Freedom Index by the Pacific Research Institute. In the report’s first edition, published before Fisher summarized his objections: “The underlying problem with the … indexes, of course, is twofold: none of them actually do a very good job of measuring what it is they claim to measure, and they do not, for the most part, set out to measure the right things to begin with” (Fisher 2005). In the second edition, he identified three overarching questions: (1) whether the indices included relevant variables, and only relevant variables; (2) whether these variables measured what they purport to measure; and (3) how the index combines these measures into a single index number (Fisher 2013). Fisher’s primary argument is that if the indexes did what they purported to do, then all five would rank the states similarly.

Fisher’s conclusion holds little weight because the five indices serve such dissimilar purposes, and each group has a different area of expertise. There is no reason to believe that the Tax Foundation’s Index, which depends entirely on state tax laws, would rank the states in the same or similar order as an index that includes crime rates, electricity costs, and health care (the Small Business and Entrepreneurship Council’s Small Business Survival Index), or infant mortality rates and the percentage of adults in the workforce (Beacon Hill’s State Competitiveness Report), or charter schools, tort reform, and minimum wage laws (the Pacific Research Institute’s Economic Freedom Index).

The Tax Foundation’s State Business Tax Climate Index is an indicator of which states’ tax systems are the most hospitable to business and economic growth. The Index does not purport to measure economic opportunity or freedom, or even the broad business climate, but rather the narrower business tax climate, and its variables reflect this focus. We do so not only because the Tax Foundation’s expertise is in taxes, but because every component of the Index is subject to immediate change by state lawmakers. It is by no means clear what the best course of action is for state lawmakers who want to thwart crime, for example, either in the short or long term, but they can change their tax codes now. Contrary to Fisher’s 1970s view that the effects of taxes are “small or non-existent,” our study reflects strong evidence that business decisions are significantly impacted by tax considerations.

Although Fisher does not feel tax climates are important to states’ economic growth, other authors contend the opposite. Bittlingmayer, Eathington, Hall, and Orazem (2005) find in their analysis of several business climate studies that a state’s tax climate does affect its economic growth rate and that several indices are able to predict growth. Specifically, they concluded, “The State Business Tax Climate Index explains growth consistently.” This finding was confirmed by Anderson (2006) in a study for the Michigan House of Representatives, and more recently by Kolko, Neumark, and Mejia (2013), who, in an analysis of the ability of 10 business climate indices to predict economic growth, concluded that the State Business Tax Climate Index yields “positive, sizable, and statistically significant estimates for every specification” they measured, and specifically cited the Index as one of two business climate indices (out of 10) with particularly strong and robust evidence of predictive power.

Bittlingmayer et al. also found that relative tax competitiveness matters, especially at the borders, and therefore, indices that place a high premium on tax policies do a better job of explaining growth. They also observed that studies focused on a single topic do better at explaining economic growth at borders. Lastly, the article concludes that the most important elements of the business climate are tax and regulatory burdens on business (Bittlingmayer et al. 2005). These findings support the argument that taxes impact business decisions and economic growth, and they support the validity of the Index.

Fisher and Bittlingmayer et al. hold opposing views about the impact of taxes on economic growth. Fisher finds support from Robert Tannenwald, formerly of the Boston Federal Reserve, who argues that taxes are not as important to businesses as public expenditures. Tannenwald compares 22 states by measuring the after-tax rate of return to cash flow of a new facility built by a representative firm in each state. This very different approach attempts to compute the marginal effective tax rate of a hypothetical firm and yields results that make taxes appear trivial.

The taxes paid by businesses should be a concern to everyone because they are ultimately borne by individuals through lower wages, increased prices, and decreased shareholder value. States do not institute tax policy in a vacuum. Every change to a state’s tax system makes its business tax climate more or less competitive compared to other states and makes the state more or less attractive to business. Ultimately, anecdotal and empirical evidence, along with the cohesion of recent literature around the conclusion that taxes matter a great deal to business, show that the Index is an important and useful tool for policymakers who want to make their states’ tax systems welcoming to business.

Methodology

The Tax Foundation’s State Business Tax Climate Index is a hierarchical structure built from five components:

- Individual Income Tax

- Sales Tax

- Corporate Income Tax

- Property Tax

- Unemployment Insurance Tax

Using the economic literature as our guide, we designed these five components to score each state’s business tax climate on a scale of 0 (worst) to 10 (best). Each component is devoted to a major area of state taxation and includes numerous variables. Overall, there are 125 variables measured in this report.

The five components are not weighted equally, as they are in some indices. Rather, each component is weighted based on the variability of the 50 states’ scores from the mean. The standard deviation of each component is calculated and a weight for each component is created from that measure. The result is a heavier weighting of those components with greater variability. The weighting of each of the five major components is:

29.8% — Individual Income Tax

23.3% — Sales Tax

20.9% — Corporate Tax

14.9% — Property Tax

11.1% — Unemployment Insurance Tax

This improves the explanatory power of the State Business Tax Climate Index as a whole because components with higher standard deviations are those areas of tax law where some states have significant competitive advantages. Businesses that are comparing states for new or expanded locations must give greater emphasis to tax climates when the differences are large. On the other hand, components in which the 50 state scores are clustered together, closely distributed around the mean, are those areas of tax law where businesses are more likely to de-emphasize tax factors in their location decisions. For example, Delaware is known to have a significant advantage in sales tax competition, because its tax rate of zero attracts businesses and shoppers from all over the Mid-Atlantic region. That advantage and its drawing power increase every time another state raises its sales tax.

In contrast with this variability in state sales tax rates, unemployment insurance tax systems are similar around the nation, so a small change in one state’s law could change its component ranking dramatically.

Within each component are two equally weighted subindices devoted to measuring the impact of the tax rates and the tax bases. Each subindex is composed of one or more variables. There are two types of variables: scalar variables and dummy variables. A scalar variable is one that can have any value between 0 and 10. If a subindex is composed only of scalar variables, then they are weighted equally. A dummy variable is one that has only a value of 0 or 1. For example, a state either indexes its brackets for inflation or does not. Mixing scalar and dummy variables within a subindex is problematic because the extreme valuation of a dummy can overly influence the results of the subindex. To counter this effect, the Index generally weights scalar variables at 80 percent and dummy variables at 20 percent.

Relative versus Absolute Indexing

The State Business Tax Climate Index is designed as a relative index rather than an absolute or ideal index. In other words, each variable is ranked relative to the variable’s range in other states. The relative scoring scale is from 0 to 10, with zero meaning not “worst possible” but rather worst among the 50 states.

Many states’ tax rates are so close to each other that an absolute index would not provide enough information about the differences among the states’ tax systems, especially for pragmatic business owners who want to know which states have the best tax system in each region.

Comparing States without a Tax. One problem associated with a relative scale is that it is mathematically impossible to compare states with a given tax to states that do not have the tax. As a zero rate is the lowest possible rate and the most neutral base, since it creates the most favorable tax climate for economic growth, those states with a zero rate on individual income, corporate income, or sales gain an immense competitive advantage. Therefore, states without a given tax generally receive a 10, and the Index measures all the other states against each other.

Three notable exceptions to this rule exist. The first is in Washington, Tennessee, and Texas, which do not have taxes on wage income but do apply their gross receipts taxes to S corporations. (Washington and Texas also apply these to limited liability corporations.) Because these entities are generally taxed through the individual code, these three states do not score perfectly in the individual income tax component. The second exception is found in Nevada, where a payroll tax (for purposes other than unemployment insurance) is also included in the individual income tax component. The final exception is in zero sales tax states–Alaska, Montana, New Hampshire, Oregon, and Delaware–which do not have general sales taxes but still do not score a perfect 10 in that component section because of excise taxes on gasoline, beer, spirits, and cigarettes, which are included in that section. Alaska, moreover, forgoes a state sales tax, but does permit local option sales taxes.

Normalizing Final Scores. Another problem with using a relative scale within the components is that the average scores across the five components vary. This alters the value of not having a given tax across major indices. For example, the unadjusted average score of the corporate income tax component is 6.71 while the average score of the sales tax component is 5.39.

In order to solve this problem, scores on the five major components are “normalized,” which brings the average score for all of them to 5.00, excluding states that do not have the given tax. This is accomplished by multiplying each state’s score by a constant value.

Once the scores are normalized, it is possible to compare states across indices. For example, because of normalization, it is possible to say that Connecticut’s score of 4.94 on corporate income taxes is better than its score of 3.53 on the individual income tax.

Time Frame Measured by the Index (Snapshot Date)

Starting with the 2006 edition, the Index has measured each state’s business tax climate as it stands at the beginning of the standard state fiscal year, July 1. Therefore, this edition is the 2024 Index and represents the tax climate of each state as of July 1, 2023, the first day of fiscal year 2024 for most states.

District of Columbia

The District of Columbia (D.C.) is only included as an exhibit and its scores and “phantom ranks” offered do not affect the scores or ranks of other states.

Past Rankings and Scores

This report includes 2014-2023 Index rankings that can be used for comparison with the 2024 rankings and scores. These can differ from previously published Index rankings and scores due to the enactment of retroactive statutes, backcasting of the above methodological changes, and corrections to variables brought to our attention since the last report was published. The scores and rankings in this report are definitive.

Corporate Tax

This component measures the impact of each state’s principal tax on business activities and accounts for 20.9 percent of each state’s total score. It is well established that the extent of business taxation can affect a business’s level of economic activity within a state. For example, Newman (1982) found that differentials in state corporate income taxes were a major factor influencing the movement of industry to Southern states. Two decades later, with global investment greatly expanded, Agostini and Tulayasathien (2001) determined that a state’s corporate tax rate is the most relevant tax in the investment decisions of foreign investors.

Most states levy standard corporate income taxes on profit (gross receipts minus expenses). Some states, however, problematically impose taxes on the gross receipts of businesses with few or no deductions for expenses. Between 2005 and 2010, for example, Ohio phased in the Commercial Activities Tax (CAT), which has a rate of 0.26 percent. Washington has the Business and Occupation (B&O) Tax, which is a multi-rate tax (depending on industry) on the gross receipts of Washington businesses. Delaware has a similar Manufacturers’ and Merchants’ License Tax, as does Tennessee with its Business Tax, Virginia with its locally-levied Business/Professional/Occupational License (BPOL) tax, and West Virginia with its local Business & Occupation (B&O) tax. Texas also added the Margin Tax, a complicated gross receipts tax, in 2007, Nevada adopted the gross receipts-based multi-rate Commerce Tax in 2015, and Oregon implemented a new modified gross receipts tax in 2020. However, in 2011, Michigan passed a significant corporate tax reform that eliminated the state’s modified gross receipts tax and replaced it with a 6 percent corporate income tax, effective January 1, 2012.[13] The previous tax had been in place since 2007, and Michigan’s repeal followed others in Kentucky (2006) and New Jersey (2006). Several states contemplated gross receipts taxes in 2017, but none were adopted.

Since gross receipts taxes and corporate income taxes are levied on different bases, we separately compare gross receipts taxes to each other, and corporate income taxes to each other, in the Index.

For states with corporate income taxes, the corporate tax rate subindex is calculated by assessing three key areas: the top tax rate, the level of taxable income at which the top rate kicks in, and the number of brackets. States that levy neither a corporate income tax nor a gross receipts tax achieve a perfectly neutral system in regard to business income and thus receive a perfect score.

States that do impose a corporate tax generally will score well if they have a low rate. States with a high rate or a complex and multiple-rate system score poorly.

To calculate the parallel subindex for the corporate tax base, three broad areas are assessed: tax credits, treatment of net operating losses, and an “other” category that includes variables such as conformity to the Internal Revenue Code, protections against double taxationDouble taxation is when taxes are paid twice on the same dollar of income, regardless of whether that’s corporate or individual income. , and the taxation of “throwback” income, among others. States that score well on the corporate tax base subindex generally will have few business tax credits, generous carryback and carryforward provisions, deductions for net operating losses, conformity to the Internal Revenue Code, and provisions that alleviate double taxation.

Table 3. Corporate Tax Component of the State Business Tax Climate Index (2014–2024)

| State | 2014 Rank | 2015 Rank | 2016 Rank | 2017 Rank | 2018 Rank | 2019 Rank | 2020 Rank | 2021 Rank | 2022 Rank | 2023 Rank | 2023 Score | 2024 Rank | 2024 Score | 2023-2024 Rank Change | 2023-2024 Score Change |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Alabama | 23 | 24 | 22 | 14 | 21 | 22 | 24 | 24 | 17 | 18 | 5.51 | 19 | 5.46 | -1 | -0.05 |

| Alaska | 25 | 26 | 26 | 25 | 26 | 27 | 22 | 23 | 24 | 24 | 5.22 | 26 | 5.16 | -2 | -0.06 |

| Arizona | 22 | 22 | 20 | 19 | 14 | 16 | 21 | 22 | 23 | 23 | 5.29 | 22 | 5.30 | 1 | 0.01 |

| Arkansas | 36 | 36 | 38 | 38 | 38 | 39 | 33 | 33 | 29 | 29 | 4.96 | 28 | 5.12 | 1 | 0.16 |

| California | 29 | 31 | 33 | 32 | 31 | 37 | 27 | 27 | 46 | 46 | 4.05 | 45 | 4.06 | 1 | 0.01 |

| Colorado | 19 | 13 | 15 | 18 | 18 | 6 | 7 | 9 | 6 | 7 | 6.00 | 7 | 5.98 | 0 | -0.02 |

| Connecticut | 27 | 29 | 31 | 31 | 30 | 33 | 26 | 26 | 27 | 28 | 5.09 | 30 | 4.94 | -2 | -0.15 |

| Delaware | 50 | 50 | 50 | 50 | 50 | 50 | 50 | 50 | 50 | 50 | 2.40 | 50 | 2.35 | 0 | -0.06 |

| Florida | 13 | 14 | 16 | 19 | 19 | 11 | 9 | 6 | 7 | 10 | 5.77 | 11 | 5.81 | -1 | 0.04 |

| Georgia | 9 | 10 | 10 | 11 | 10 | 8 | 6 | 7 | 8 | 8 | 5.90 | 9 | 5.91 | -1 | 0.01 |

| Hawaii | 5 | 5 | 4 | 6 | 11 | 12 | 17 | 19 | 19 | 19 | 5.46 | 18 | 5.47 | 1 | 0.01 |

| Idaho | 17 | 21 | 21 | 23 | 23 | 26 | 28 | 28 | 28 | 27 | 5.10 | 27 | 5.14 | 0 | 0.05 |

| Illinois | 43 | 44 | 32 | 24 | 35 | 36 | 35 | 35 | 38 | 38 | 4.46 | 43 | 4.16 | -5 | -0.30 |

| Indiana | 28 | 27 | 23 | 22 | 22 | 19 | 11 | 12 | 11 | 11 | 5.73 | 12 | 5.74 | -1 | 0.01 |

| Iowa | 48 | 48 | 48 | 48 | 48 | 46 | 48 | 46 | 33 | 34 | 4.84 | 29 | 5.09 | 5 | 0.24 |

| Kansas | 35 | 35 | 37 | 37 | 37 | 31 | 34 | 30 | 21 | 21 | 5.37 | 21 | 5.32 | 0 | -0.05 |

| Kentucky | 24 | 25 | 25 | 26 | 24 | 15 | 13 | 15 | 15 | 15 | 5.60 | 15 | 5.61 | 0 | 0.01 |

| Louisiana | 16 | 20 | 35 | 39 | 39 | 34 | 36 | 34 | 34 | 32 | 4.87 | 34 | 4.81 | -2 | -0.06 |

| Maine | 41 | 42 | 41 | 40 | 40 | 32 | 37 | 36 | 35 | 35 | 4.58 | 35 | 4.58 | 0 | 0.01 |

| Maryland | 14 | 15 | 17 | 21 | 20 | 25 | 31 | 32 | 32 | 33 | 4.85 | 33 | 4.86 | 0 | 0.01 |

| Massachusetts | 32 | 34 | 36 | 35 | 34 | 38 | 38 | 37 | 36 | 36 | 4.55 | 36 | 4.55 | 0 | 0.01 |

| Michigan | 8 | 8 | 8 | 9 | 8 | 13 | 18 | 20 | 20 | 20 | 5.42 | 20 | 5.43 | 0 | 0.01 |

| Minnesota | 40 | 40 | 42 | 42 | 41 | 43 | 45 | 43 | 43 | 43 | 4.13 | 47 | 3.83 | -4 | -0.31 |

| Mississippi | 10 | 11 | 12 | 12 | 12 | 14 | 10 | 13 | 13 | 13 | 5.64 | 8 | 5.95 | 5 | 0.32 |

| Missouri | 4 | 4 | 3 | 5 | 5 | 4 | 3 | 3 | 3 | 3 | 6.76 | 3 | 6.55 | 0 | -0.21 |

| Montana | 15 | 16 | 18 | 13 | 13 | 9 | 20 | 21 | 22 | 22 | 5.34 | 23 | 5.28 | -1 | -0.05 |

| Nebraska | 34 | 28 | 27 | 27 | 27 | 28 | 30 | 31 | 31 | 30 | 4.92 | 31 | 4.91 | -1 | -0.01 |

| Nevada | 1 | 1 | 24 | 33 | 32 | 21 | 25 | 25 | 26 | 26 | 5.18 | 25 | 5.18 | 1 | 0.01 |

| New Hampshire | 47 | 47 | 47 | 47 | 43 | 45 | 42 | 44 | 44 | 44 | 4.10 | 44 | 4.11 | 0 | 0.01 |

| New Jersey | 37 | 37 | 39 | 41 | 44 | 49 | 49 | 48 | 48 | 48 | 3.50 | 48 | 3.50 | 0 | 0.00 |

| New Mexico | 33 | 33 | 30 | 29 | 25 | 23 | 23 | 11 | 12 | 12 | 5.72 | 13 | 5.66 | -1 | -0.05 |

| New York | 21 | 19 | 11 | 8 | 7 | 18 | 14 | 16 | 25 | 25 | 5.19 | 24 | 5.20 | 1 | 0.01 |

| North Carolina | 26 | 23 | 7 | 4 | 3 | 3 | 4 | 4 | 4 | 5 | 6.15 | 5 | 6.16 | 0 | 0.01 |

| North Dakota | 20 | 18 | 14 | 16 | 16 | 17 | 19 | 8 | 9 | 9 | 5.89 | 10 | 5.84 | -1 | -0.05 |

| Ohio | 45 | 43 | 46 | 46 | 47 | 42 | 41 | 40 | 39 | 39 | 4.43 | 39 | 4.44 | 0 | 0.01 |

| Oklahoma | 11 | 9 | 9 | 10 | 9 | 20 | 8 | 10 | 10 | 4 | 6.20 | 4 | 6.21 | 0 | 0.01 |

| Oregon | 30 | 32 | 34 | 34 | 33 | 29 | 32 | 49 | 49 | 49 | 2.79 | 49 | 2.73 | 0 | -0.06 |

| Pennsylvania | 42 | 41 | 43 | 43 | 42 | 44 | 44 | 42 | 42 | 42 | 4.15 | 41 | 4.35 | 1 | 0.20 |

| Rhode Island | 38 | 38 | 29 | 30 | 29 | 35 | 40 | 39 | 40 | 40 | 4.39 | 40 | 4.40 | 0 | 0.01 |

| South Carolina | 12 | 12 | 13 | 15 | 15 | 5 | 5 | 5 | 5 | 6 | 6.04 | 6 | 6.05 | 0 | 0.01 |

| South Dakota | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 10.00 | 1 | 10.00 | 0 | 0.00 |

| Tennessee | 44 | 45 | 44 | 44 | 45 | 48 | 47 | 45 | 45 | 45 | 4.06 | 42 | 4.32 | 3 | 0.25 |

| Texas | 49 | 49 | 49 | 49 | 49 | 47 | 46 | 47 | 47 | 47 | 3.98 | 46 | 3.99 | 1 | 0.01 |

| Utah | 6 | 6 | 5 | 3 | 4 | 7 | 12 | 14 | 14 | 14 | 5.63 | 14 | 5.62 | 0 | -0.02 |

| Vermont | 39 | 39 | 40 | 36 | 36 | 40 | 43 | 41 | 41 | 41 | 4.31 | 38 | 4.45 | 3 | 0.14 |

| Virginia | 7 | 7 | 6 | 7 | 6 | 10 | 15 | 17 | 16 | 17 | 5.54 | 16 | 5.55 | 1 | 0.01 |

| Washington | 46 | 46 | 45 | 45 | 46 | 41 | 39 | 38 | 37 | 37 | 4.47 | 37 | 4.48 | 0 | 0.01 |

| West Virginia | 18 | 17 | 19 | 17 | 17 | 24 | 16 | 18 | 18 | 16 | 5.60 | 17 | 5.54 | -1 | -0.05 |

| Wisconsin | 31 | 30 | 28 | 28 | 28 | 30 | 29 | 29 | 30 | 31 | 4.88 | 32 | 4.88 | -1 | 0.01 |

| Wyoming | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 10.00 | 1 | 10.00 | 0 | 0.00 |

| District of Columbia | 37 | 37 | 37 | 26 | 26 | 24 | 27 | 27 | 28 | 29 | 5.03 | 30 | 5.04 | -1 | 0.01 |

Source: Tax Foundation.

Corporate Tax Rate

The corporate tax rate subindex is designed to gauge how a state’s corporate income tax top marginal rate, bracket structure, and gross receipts rate affect its competitiveness compared to other states, as the extent of taxation can affect a business’s level of economic activity within a state (Newman 1982).

A state’s corporate tax is levied in addition to the federal corporate income tax of 21 percent, substantially reduced by the Tax Cuts and Jobs Act of 2017 from a graduated-rate tax with a top rate of 35 percent, the highest rate among industrialized nations. Two states levy neither a corporate income tax nor a gross receipts tax: South Dakota and Wyoming. These states automatically score a perfect 10 on this subindex. Therefore, this section ranks the remaining 48 states relative to each other.

Top Tax Rate. New Jersey’s 11.5 percent rate (including a temporary and retroactive surcharge from 2020 to 2023) qualifies for the worst ranking among states that levy one, followed by Minnesota’s 9.8 percent rate. Other states with comparatively high corporate income tax rates are Alaska (9.4 percent), Pennsylvania (8.99 percent), Maine (8.93 percent), and California (8.84 percent). By contrast, North Carolina’s rate of 2.5 percent is the lowest nationally, followed by Missouri’s and Oklahoma’s (both at 4 percent), North Dakota’s at 4.31 percent, and Colorado’s at 4.4 percent. Other states with comparatively low top corporate tax rates are Utah (4.65 percent), Arizona and Indiana (both at 4.9 percent), and Kentucky, Mississippi, and South Carolina, all at 5 percent.

Graduated Rate Structure. Two variables are used to assess the economic drag created by multiple-rate corporate income tax systems: the income level at which the highest tax rate starts to apply and the number of tax brackets. Twenty-nine states and the District of Columbia have single-rate systems, and they score best. Single-rate systems are consistent with the sound tax principles of simplicity and neutrality. In contrast to the individual income tax, there is no meaningful “ability to pay” concept in corporate taxation. Jeffery Kwall, the Kathleen and Bernard Beazley Professor of Law at Loyola University Chicago School of Law, notes that

graduated corporate rates are inequitable—that is, the size of a corporation bears no necessary relation to the income levels of the owners. Indeed, low-income corporations may be owned by individuals with high incomes, and high-income corporations may be owned by individuals with low incomes.[14]