Key Findings

- In 2025, 13 countries made changes to their statutory corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax. rates. Eight countries—Estonia, France, Lithuania, Morocco, the Russian Federation, Slovakia, Tunisia, and Zimbabwe—increased their top corporate taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. rates, while five countries—Equatorial Guinea, Namibia, Iceland, Luxembourg, and Portugal—reduced their corporate tax rates.

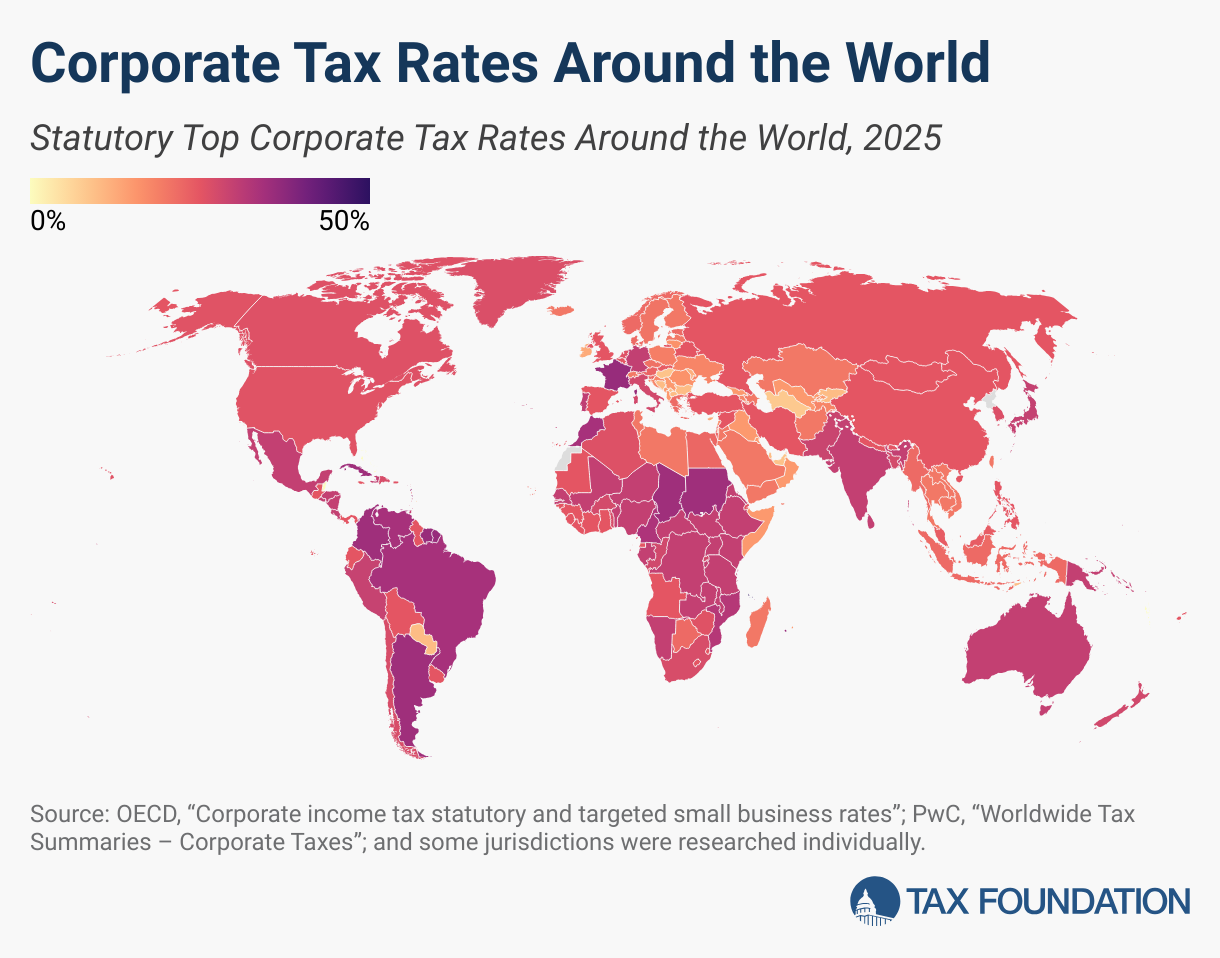

- The countries with the highest corporate tax rates in the world are Comoros (50 percent), Puerto Rico (37.5 percent), France (36.13 percent), and Suriname (36 percent), while the countries with the lowest corporate rates are Turkmenistan (8 percent), Barbados, the United Arab Emirates, and Hungary (all at 9 percent). Fifteen jurisdictions do not impose a corporate tax.

- By 2025, of the 18 countries with statutory corporate tax rates below 15 percent, nine—Barbados, Hungary, United Arab Emirates, Bulgaria, Qatar, North Macedonia, Cyprus, Ireland, and Lichtenstein—have implemented the qualified domestic minimum top-up tax (QDMTT) rules from the Organisation for Co-operation and Economic Development (OECD) Pillar Two agreement, raising their effective corporate tax rate to 15 percent.

- In 2025, of the 15 countries without a corporate income tax, six—Bahrain, Bermuda, Guernsey, Isle of Man, Jersey, and the Bahamas—implemented the QDMTT from the Pillar Two rules, bringing their effective corporate tax rate to 15 percent.

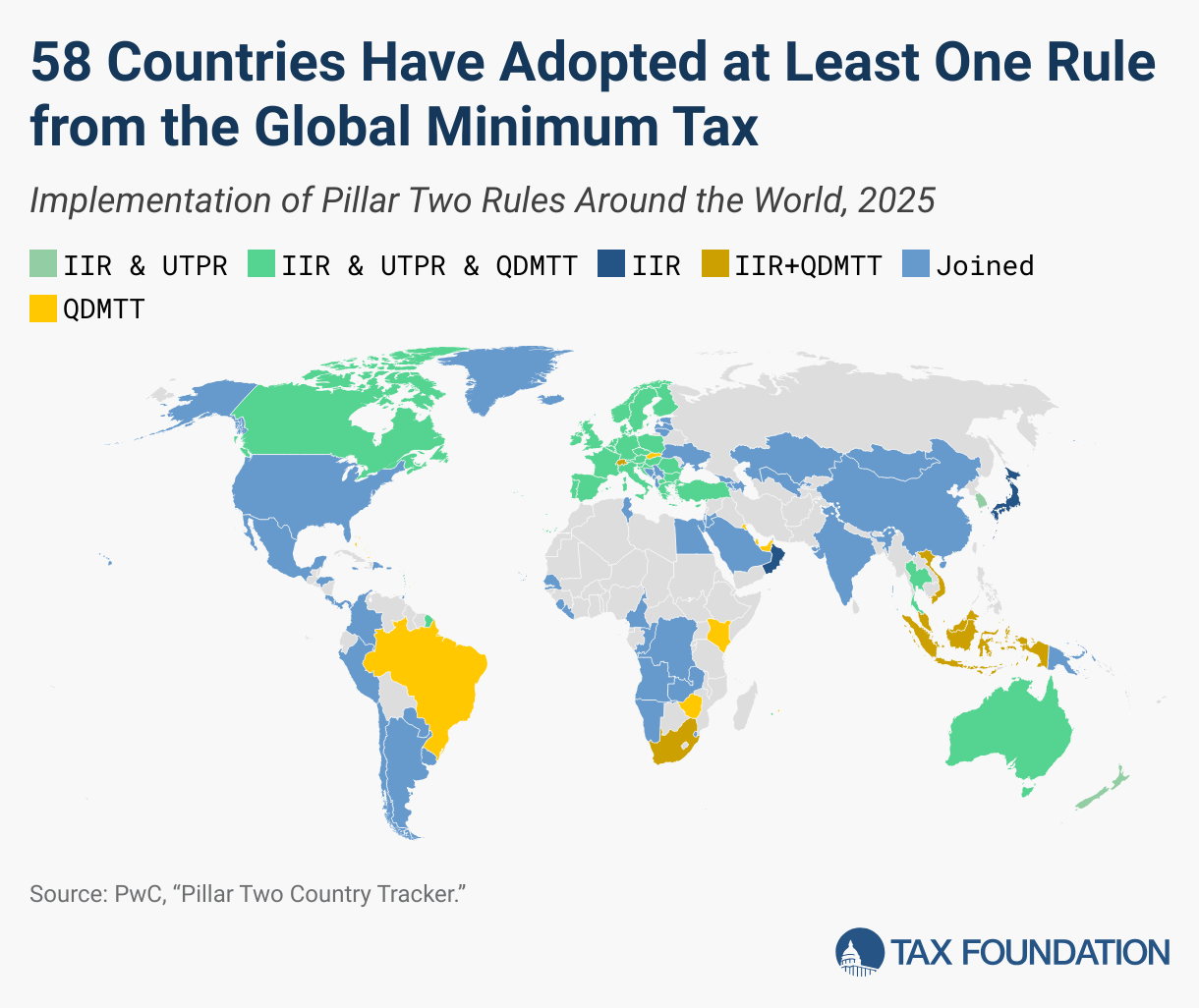

- As of 2025, 29 countries have adopted the income inclusion rule (IIR), the QDMTT, and the undertaxed profits rule (UTPR), while 13 countries have adopted both the IIR and the QDMTT. Two countries—Japan and Oman—have adopted only the IIR, two countries—New Zealand and South Korea—have adopted only the IIR and UTPR, and 12 countries—the United Arab Emirates, Bahamas, Bahrain, Barbados, Bermuda, Brazil, Kenia, Kuwait, Mauritius, Qatar, Slovakia, and Zimbabwe—have only adopted the QDMTT. However, by the end of 2026, Iceland will have implemented both the IIR and QDMT, and the UTPR and QDMTT will have entered into force in Japan. Also, Israel and New Zealand will have adopted the QDMTT, and Indonesia, the UTPR. The worldwide average statutory corporate income tax rate, measured across 181 jurisdictions, is 23.58 percent. When weighted by GDP, the average statutory rate is 26.04 percent.

- Asia has the lowest regional average rate at 19.74 percent, while South America has the highest regional average statutory rate at 28.38 percent. Even when weighted by GDP, Asia still has the lowest regional average rate at 25.10 percent, while South America has the highest at 32.66 percent.

- The average top corporate rate among EU Member States is 21.81 percent, 24.20 percent in OECD countries, and 28.61 percent in the

- When accounting for the global minimum tax, Europe’s average rate raises to 21.19 percent, North America’s average rate raises to 26.46 percent, the OECD’s average rate raises to 24.42 percent, and EU Members States’ average rate raises to 22.40 percent.

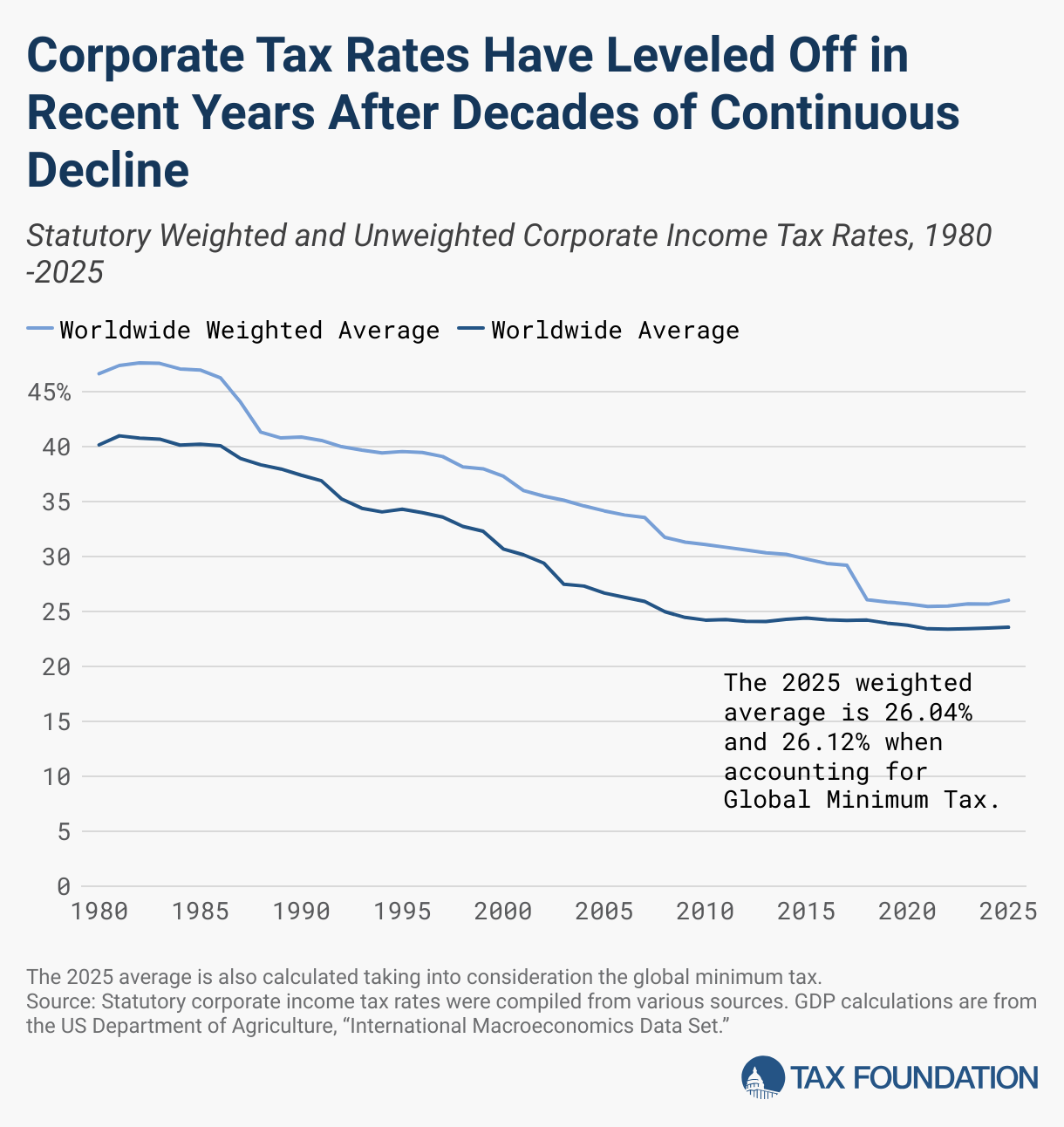

- The worldwide average statutory corporate tax rate has consistently decreased since 1980 but has leveled off in recent years.

- The average statutory corporate tax rate has declined in every region since 1980.

Introduction

In 1980, corporate tax rates around the world averaged 40.18 percent, and 46.66 percent when weighted by GDP.[1] Since then, countries have recognized the impact that high corporate tax rates have on business investment decisions; in 2025, the average is now 23.58 percent, and 26.04 when weighted by GDP, for 181 separate tax jurisdictions. [2] When accounting for the global minimum tax, the 2025 average is 23.95 percent, and 26.12 percent when weighted by GDP.[3]

Declines have been seen in every major region of the world, including in the largest economies. In the United States, the 2017 Tax Cuts and Jobs Act brought the country’s statutory corporate income tax rate from the fourth highest in the world closer to the middle of the distribution.[4]

Asian and European countries tend to have lower corporate income tax rates than countries in other regions, and many developing countries have corporate income tax rates that are above the worldwide average.

Today, most countries have corporate tax rates below 30 percent.

Notable Corporate Tax Rate Changes in 2025

Thirteen countries changed their statutory corporate income tax rates in 2025. Eight countries increased their top corporate rates: Morocco (33 percent to 34 percent), Tunisia (15 percent to 20 percent), Zimbabwe (24.729 percent to 25.75 percent), Estonia (20 percent to 22 percent), France (25.83 percent to 36.13 percent), Lithuania (15 percent to 16 percent), Russian Federation (20 percent to 25 percent) and Slovakia (21 percent to 24 percent).

Five countries across two continents—Equatorial Guinea, Namibia, Iceland, Luxembourg, and Portugal—reduced their corporate tax rates in 2025. The tax rate reductions ranged from just 1 percentage point in Iceland and Portugal to 10 percentage points in Equatorial Guinea.

Additionally, in 2025, 10 countries with no corporate tax or with statutory corporate tax rates below 15 percent—Bahrain, Bermuda, Qatar, United Arab Emirates, Cyprus, Guernsey, Isle of Man, Jersey, North Macedonia, and the Bahamas—implemented the QDMTT from the Pillar Two rules, raising their effective corporate tax rate for large companies to 15 percent. Currently, 15 countries with no corporate tax rate or with statutory corporate tax rates below 15 percent have implemented the QDMTT. Five countries—Bulgaria, Hungary, Ireland, Liechtenstein, and Barbados—implemented the QDMTT in 2024.

Table 1. Notable Corporate Income Tax Rate Changes in 2025

| Country | 2024 Tax Rate | 2025 Tax Rate | 2025 Tax Rate Accounting for Global Minimum Tax | Change from 2024 to 2025 |

|---|---|---|---|---|

| Africa | ||||

| Equatorial Guinea | 35% | 25% | 25% | -10 ppt |

| Morocco | 33% | 34% | 34% | +1 ppt |

| Namibia | 32% | 30% | 30% | -2 ppt |

| Tunisia | 15% | 20% | 20% | +5 ppt |

| Zimbabwe | 24.72% | 25.75% | 25.75% | +1.03ppt |

| Asia | ||||

| Bahrain | 0% | 0% | 15% | +15 ppt |

| Qatar | 10% | 10% | 15% | +5 ppt |

| United Arab Emirates | 9% | 9% | 15% | +6 ppt |

| Europe | ||||

| Cyprus | 13% | 13% | 15% | +2.5 ppt |

| Estonia | 20% | 22% | 22% | +2 ppt |

| France | 25.83% | 36.13% | 36.13% | +10.31 ppt |

| Guernsey | 0% | 0% | 15% | +15 ppt |

| Iceland | 21% | 20% | 20% | -1 ppt |

| Isle of Man | 0% | 0% | 15% | +15 ppt |

| Jersey | 0% | 0% | 15% | +15 ppt |

| Lithuania | 15% | 16% | 16% | +1 ppt |

| Luxembourg | 25% | 24% | 24% | -1.07 ppt |

| Portugal | 32% | 31% | 31% | -1 ppt |

| Russian Federation | 20% | 25% | 25% | +5 ppt |

| Slovakia | 21% | 24% | 24% | +3 ppt |

| North Macedonia | 10% | 10% | 15% | +5 ppt |

| North America | ||||

| Bahamas | 0% | 0% | 15% | +15 ppt |

| Bermuda | 0% | 0% | 15% | +15 ppt |

Scheduled Corporate Tax Rate Changes in the OECD and Selected Jurisdictions

Among OECD countries, Estonia and Lithuania have announced they will implement changes to their statutory corporate income tax rates in 2026. Additionally, Morocco and Slovenia have enacted changes to their statutory corporate income taxes that will continue in 2026, while Germany’s and Portugal’s corporate tax reforms will take place over the coming years.

- In Estonia, the corporate income tax will be increased from 22 percent in 2025 to 24 percent in 2026.[5]

- In Germany, the corporate income tax will decrease by one percentage point per year, starting in 2028 and ending in 2032.[6]

- In Lithuania, the corporate income tax will increase from 16 percent in 2025 to 17 percent in 2026.[7]

- In Morocco, the top corporate income tax was increased from 31 percent to 35 percent for companies with a taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. Taxable income differs from—and is less than—gross income. higher than MAD 100 million (USD 9.9 million). However, this increase was introduced over three years, with a one percentage point increase each year. For the fiscal year of 2026, the corporate income tax rate applicable will be 35 percent.[8]

- In Portugal, the corporate income tax will decrease by one percentage point per year, starting from January 2026 and ending in 2028.[9]

- In Slovenia, the top corporate income tax was increased temporarily, from 19 percent to 22 percent, for five years, until 2028. This five-year tax is set to finance the reconstruction efforts after the major floods that occurred in August 2023.[10]

The Impact of Global Minimum Tax

More than 140 countries have already agreed to a set of rules for a 15 percent global minimum tax, as part of the 2021 global tax agreement coordinated by the OECD. The global minimum tax, also known as Pillar Two, includes three main rules. The first is a qualified domestic minimum top-up tax, which countries could use to claim the first right to tax profits currently being taxed below the minimum effective rate of 15 percent. The second is an income inclusion rule, which determines when the foreign income of a company should be included in the taxable income of the parent company. When a company’s effective tax rate falls below 15 percent, additional taxes would be owed in its home jurisdiction. The third rule in Pillar Two is the undertaxed profits rule, which would allow a country to increase taxes on a company if another related entity in a different jurisdiction was being taxed below the 15 percent effective rate. If multiple countries apply a similar top-up tax, the taxable profit would be divided based on the location of tangible assets and employees.

These model rules are incentivizing countries around the world to implement a corporate income tax for the first time.

The United Arab Emirates, which introduced a 9 percent federal corporate income tax in 2023, now imposes a minimum top-up tax of 15 percent on large multinational companies operating in the country since January 1, 2025.

Bermuda has also introduced a minimum 15 percent corporate income tax. In recent years, the Bermuda government extended a tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax. granted to Bermuda companies until March 2035. This exemption is supposed to protect companies from any newly enacted taxes on income or capital gains until March 2035. However, in December 2023, Bermuda introduced a 15 percent corporate income tax on multinational companies with annual revenue of EUR 750 million or more, effective from 2025. Bermuda’s corporate income tax aligns with the Pillar Two rules and qualifies as a covered tax. However, Bermuda currently has no proposals to introduce the income inclusion rule (IIR) or the undertaxed profits rule (UTPR).[11]

Additionally, in 2025, five other countries that did not impose a general corporate income tax—Bahrain, Guernsey, Isle of Man, Jersey, and the Bahamas—have implemented the QDMTT from the Pillar Two rules, bringing their statutory corporate tax rate to 15 percent.[12]

At the end of 2022, the EU also adopted its own Pillar Two directive. The EU obliges Member States with more than 12 in-scope multinational groups to implement the IIR starting December 31, 2023, and the UTPR starting December 31, 2024. Member States with no more than 12 in-scope multinational groups can elect to defer implementing both rules for six years under Article 50 of the Directive.[13]

As of 2025, 29 countries have adopted the three rules, 13 adopted both the IIR and the QDMTT, two countries—Japan and Oman—have adopted only the IIR, two countries—New Zealand and South Korea—have adopted only the IIR and UTPR, and 12 countries—the United Arab Emirates, the Bahamas, Bahrain, Barbados, Bermuda, Brazil, Kenia, Kuwait, Mauritius, Qatar, Slovakia, and Zimbabwe—have only adopted the QDMTT. However, by the end of 2026, Iceland will have implemented both the IIR and QDMT, and the UTPR and QDMTT will have entered into force in Japan. Also, Israel and New Zealand will have adopted the QDMTT, and Indonesia, the UTPR.[14]

However, while countries implement the global minimum tax, they are also considering new qualified refundable tax creditA refundable tax credit can be used to generate a federal tax refund larger than the amount of tax paid throughout the year. In other words, a refundable tax credit creates the possibility of a negative federal tax liability. An example of a refundable tax credit is the Earned Income Tax Credit (EITC). incentives for multinational companies allowed under the framework to continue competing for investment.[15]

The Highest and Lowest Corporate Tax Rates in the World

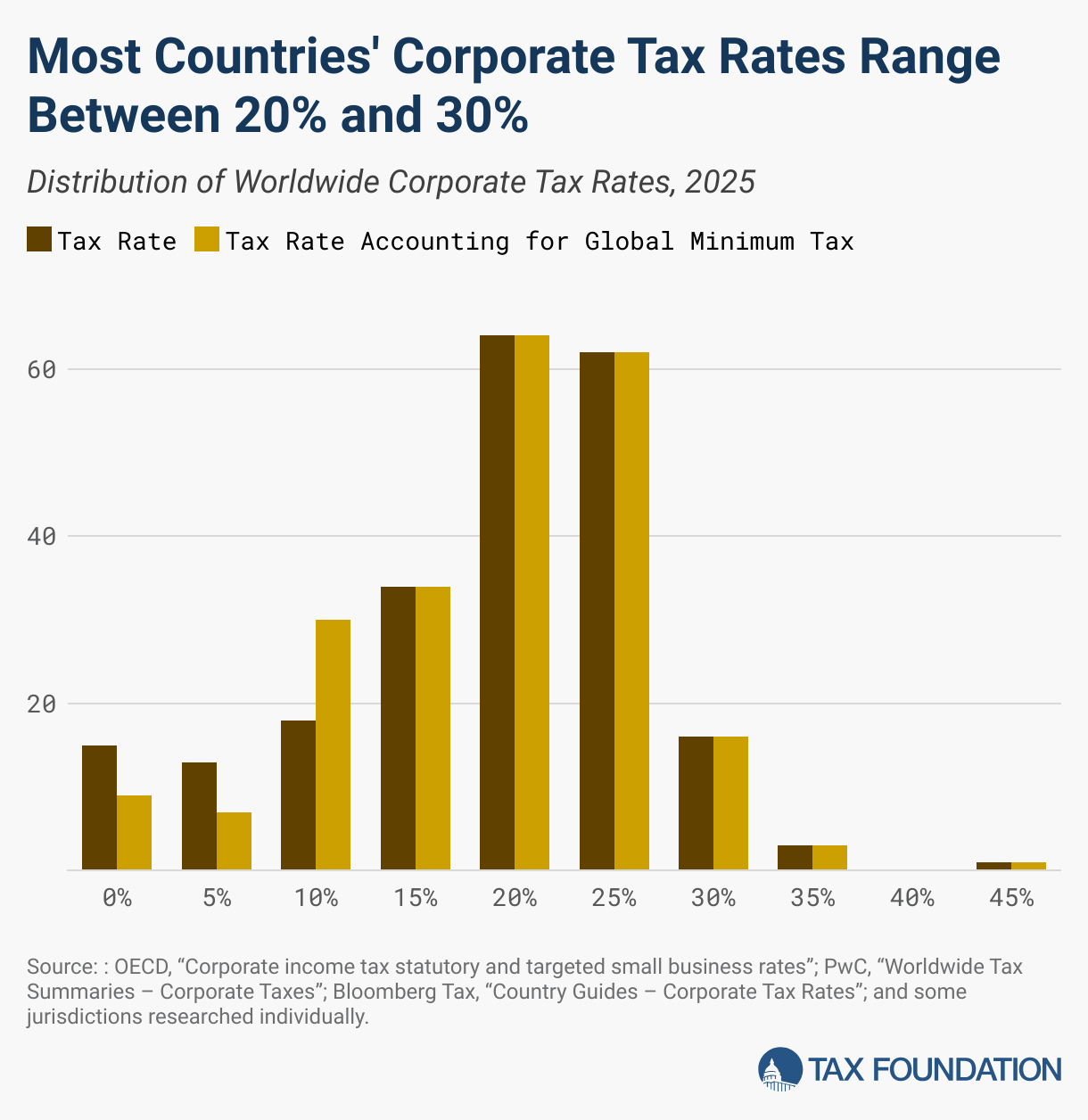

One hundred and forty-three of the 226 separate jurisdictions surveyed in 2025 have corporate tax rates at or below 25 percent.[16] One hundred and twenty-six have rates above 20 percent but below or at 30 percent. The average rate among the 226 jurisdictions is 22.35 percent.[17] The United States has the 82nd-highest corporate tax rate with a combined federal and state statutory rate of 25.57 percent.[18]

The 20 countries with the highest statutory corporate income tax rates span almost every region, albeit unequally. While six of the top 20 countries are in Africa, Oceania appears only once. Of the remaining jurisdictions, four are in North America, another four are in Europe, and five are in South America.

Table 2. 20 Highest Statutory Corporate Income Tax Rates in the World, 2025

| Country | Continent | Tax Rate |

|---|---|---|

| Comoros* | Africa | 50% |

| Puerto Rico | North America | 37.5% |

| France | Europe | 36.13% |

| Suriname | South America | 36% |

| Argentina | South America | 35% |

| Chad | Africa | 35% |

| Colombia | South America | 35% |

| Cuba | North America | 35% |

| Malta | Europe | 35% |

| Sudan | Africa | 35% |

| Sint Maarten (Dutch part) | North America | 34.5% |

| American Samoa | Oceania | 34% |

| Brazil | South America | 34% |

| Morocco | Africa | 34% |

| Bolivarian Republic of Venezuela | South America | 34% |

| Cameroon | Africa | 33% |

| Saint Kitts and Nevis | North America | 33% |

| Mozambique | Africa | 32% |

| Portugal | Europe | 30.50% |

| Germany | Europe | 30.06% |

Source: OECD, “Corporate income tax statutory and targeted small business rates,” updated April 2025; PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2025, https://taxsummaries.pwc.com/; Bloomberg Tax, “Country Guides – Corporate Tax Rates,” accessed November 2025, https://www.bloomberglaw.com/product/tax/toc_view_menu/3380; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates,” GitHub, https://github.com/TaxFoundation/worldwide-corporate-tax-rates.

On the other end of the spectrum, of the 20 countries with the lowest non-zero statutory corporate tax rates, 18 charge rates at or below 15 percent. Nine countries have statutory rates of 10 percent, five being small European nations (Andorra, Bosnia and Herzegovina, Bulgaria, Kosovo, and Macedonia). The only two OECD members represented among the bottom 20 countries are Hungary and Ireland. Hungary reduced its corporate income tax rate from 19 to 9 percent in 2017. Ireland has had its 12.5 percent rate in place since 2003. By 2025, of the 18 countries with corporate tax rates below 15 percent, nine—Barbados, Hungary, United Arab Emirates, Bulgaria, Qatar, North Macedonia, Cyprus, Ireland, and Lichtenstein—have implemented the QDMTT from the Pillar Two rules, raising their effective corporate tax rate to 15 percent.

Tale 3. 20 Lowest Statutory Corporate Income Tax Rates in the World, 2025

| Country | Continent | Tax Rate | Tax Rate Accounting for Global Minimum Tax |

|---|---|---|---|

| Turkmenistan | Asia | 8% | 8% |

| Barbados | North America | 9% | 15% |

| Hungary | Europe | 9% | 15% |

| United Arab Emirates | Asia | 9% | 15% |

| Andorra | Europe | 10% | 10% |

| Bosnia and Herzegovina | Europe | 10% | 10% |

| Bulgaria | Europe | 10% | 15% |

| Republic of Kosovo | Europe | 10% | 10% |

| Kyrgyzstan | Asia | 10% | 10% |

| Paraguay | South America | 10% | 10% |

| Qatar | Asia | 10% | 15% |

| North Macedonia | Europe | 10% | 15% |

| Timor-Leste | Oceania | 10% | 10% |

| China, Macao Special Administrative Region | Asia | 12% | 12% |

| Republic of Moldova | Europe | 12% | 12% |

| Cyprus | Europe | 12.5% | 15% |

| Ireland | Europe | 12.5% | 15% |

| Liechtenstein | Europe | 12.5% | 15% |

| Albania* | Europe | 15% | 15% |

| Georgia* | Asia | 15% | 15% |

*Apart from Albania and Georgia, there are 11 other countries with a corporate tax rate of 15 percent that are not shown in this table.

Source: OECD, “Corporate income tax statutory and targeted small business rates”; PwC, “Worldwide Tax Summaries – Corporate Taxes”; Bloomberg Tax, “Country Guides – Corporate Tax Rates”; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates.”

Of the 226 jurisdictions surveyed, 15 currently do not impose a general corporate income tax. All these jurisdictions are small, island nations. A handful, such as the Cayman Islands and Bermuda, are well known for their lack of corporate taxes. In 2025, of the 15 countries without a corporate income tax, five—Bahrain, Guernsey, Isle of Man, Jersey, and the Bahamas—have implemented the QDMTT from the Pillar Two rules, bringing their effective corporate tax rate to 15 percent. Bermuda also introduced a 15 percent corporate income tax on multinational companies with annual revenue of EUR 750 million or more, effective from 2025, which qualifies as a covered tax under the Pillar Two rules.

Table 4. Countries without General Corporate Income Tax, 2025

| Country | Continent | Tax Rate Accounting for Global Minimum Tax |

|---|---|---|

| Anguilla | North America | 0% |

| Bahamas | North America | 15% |

| Bahrain* | Asia | 15% |

| Belize* | North America | 0% |

| Bermuda* | North America | 15% |

| British Virgin Islands | North America | 0% |

| Cayman Islands | North America | 0% |

| Guernsey | Europe | 15% |

| Isle of Man | Europe | 15% |

| Jersey | Europe | 15% |

| Saint Barthelemy | North America | 0% |

| Tokelau | Oceania | 0% |

| Turks and Caicos Islands | North America | 0% |

| Vanuatu | Oceania | 0% |

| Wallis and Futuna Islands | Oceania | 0% |

Source: OECD, “Corporate income tax statutory and targeted small business rates”; PwC, “Worldwide Tax Summaries – Corporate Taxes”; Bloomberg Tax, “Country Guides – Corporate Tax Rates.”

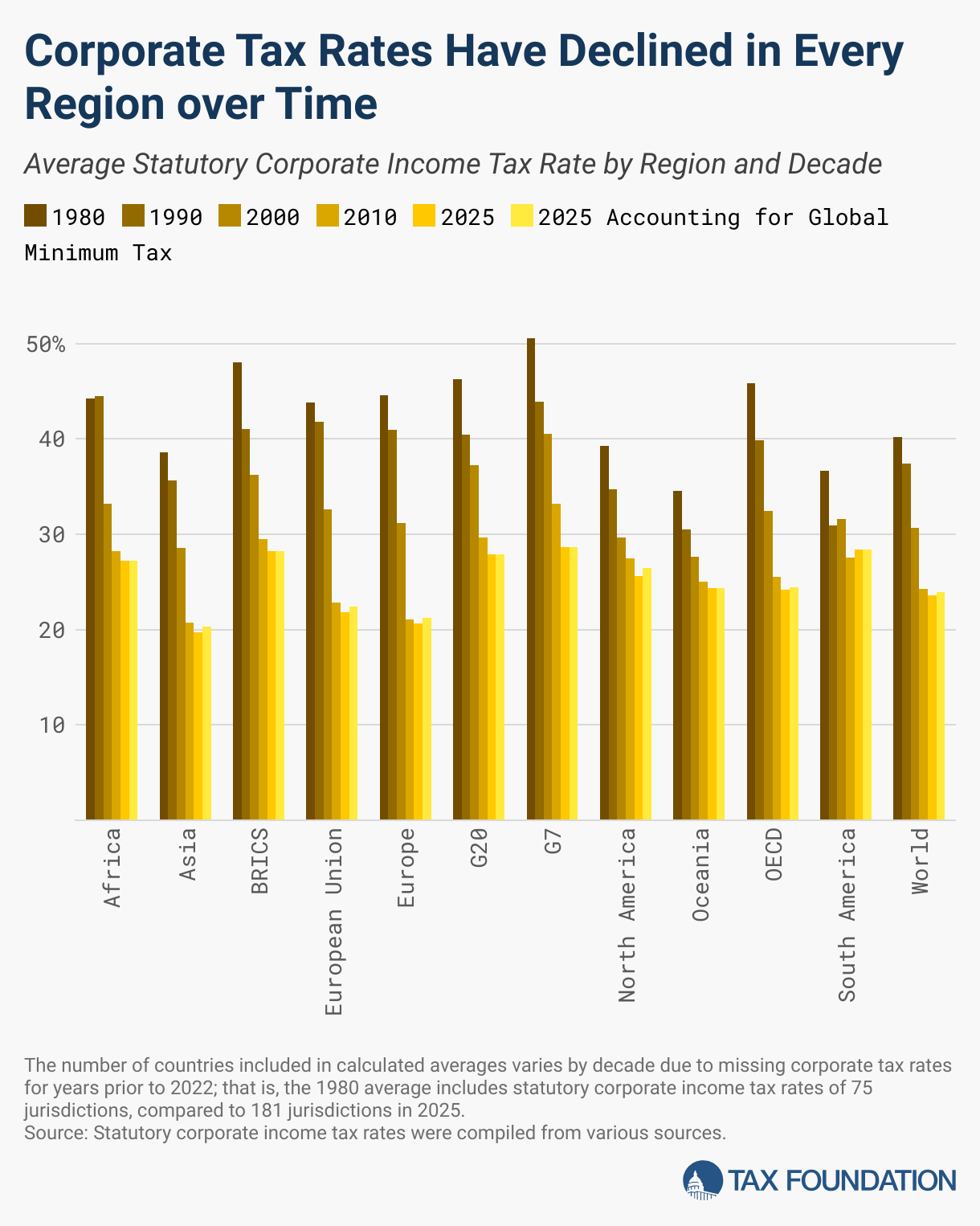

Regional Variation in Corporate Tax Rates

Corporate tax rates can vary significantly by region. South America has the highest average statutory corporate tax rate among all regions at 28.38 percent. Asia has the lowest average statutory corporate tax rate among all regions at 19.74 percent.

When weighted by GDP, South America has the highest average statutory corporate tax rate at 32.66 percent, while Asia has the lowest at 25.10 percent.

In general, larger and more industrialized nations tend to have higher corporate income tax rates than smaller nations. The G7, which is comprised of the seven wealthiest nations in the world, has an average statutory corporate income tax rate of 28.61 percent and a weighted average rate of 27.28 percent. OECD member states have an average statutory corporate tax rate of 24.20 percent and a rate of 26.59 percent when weighted by GDP. The BRICS[19] have an average statutory rate of 28.20 percent and a weighted average statutory corporate income tax rate of 26.56 percent.

When accounting for the global minimum tax, there are no significant changes in the weighted averages of the regions analyzed. However, when comparing the unweighted averages, Asia (20.29 percent), Europe (21.19 percent), and North America (26.46 percent) have slightly higher average rates when accounting for the global minimum than without the global minimum tax (19.74 percent, 20.65 percent, and 25.59 percent, respectively). Additionally, when accounting for the global minimum tax, the OECD average rate rises from 24.20 percent to 24.42 percent, while the European Union average rises from 21.81 percent to 22.40 percent.

Table 5. Average Corporate Tax Rate by Region or Group, 2025

| Region | Average Rate | Average Rate Accounting for Global Minimum Tax | Average Rate Weighted by GDP | Average Rate Accounting for Global Minimum Tax Weighted by GDP | Number of Countries Covered |

|---|---|---|---|---|---|

| Africa | 27.18% | 27.18% | 27.69% | 27.69% | 51 |

| Asia | 19.74% | 20.29% | 25.10% | 25.20% | 47 |

| Europe | 20.65% | 21.19% | 26.06% | 26.19% | 39 |

| North America | 25.59% | 26.46% | 25.90% | 25.91% | 24 |

| Oceania | 24.38% | 24.38% | 29.72% | 29.72% | 8 |

| South America | 28.38% | 28.38% | 32.66% | 32.66% | 12 |

| G7 | 28.61% | 28.61% | 27.28% | 27.28% | 7 |

| OECD | 24.20% | 24.42% | 26.59% | 26.63% | 38 |

| BRICS | 28.20% | 28.20% | 26.56% | 26.56% | 5 |

| European Union | 21.81% | 22.40% | 26.96% | 27.13% | 27 |

| G20 | 27.88% | 27.88% | 26.97% | 26.97% | 19 |

| World | 23.58% | 23.96% | 26.04% | 26.12% | 181 |

Source: OECD, “Corporate income tax statutory and targeted small business rates”; PwC, “Worldwide Tax Summaries – Corporate Taxes”; Bloomberg Tax, “Country Guides – Corporate Tax Rates”; and some jurisdictions researched individually, see Tax Foundation, “worldwide-corporate-tax-rates.”

The following map illustrates the current state of corporate tax rates around the world. Countries in Africa and South America tend to have higher corporate tax rates than Asian and European jurisdictions. Oceania’s and North America’s corporate tax rates tend to be close to the world average.

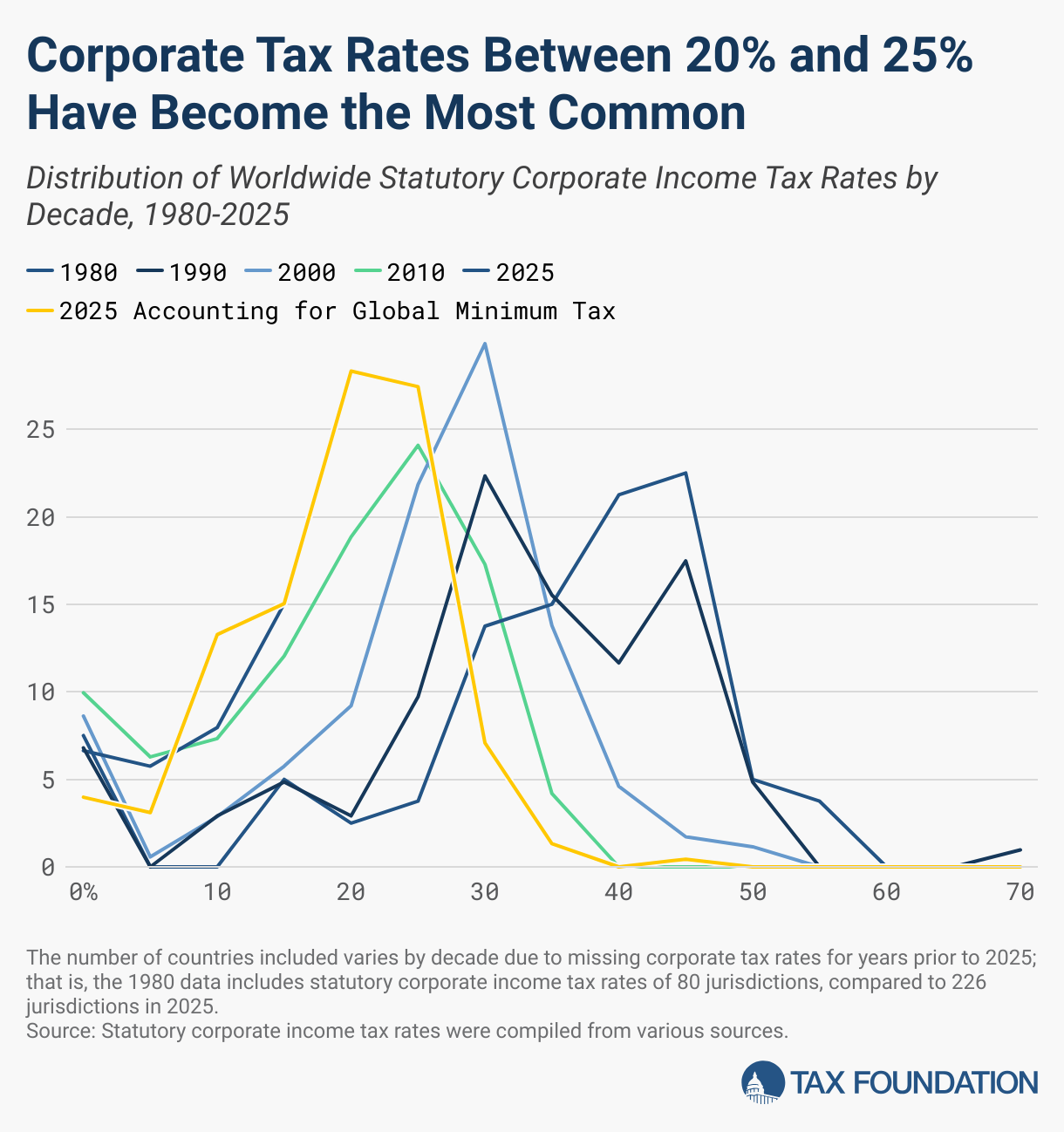

Distribution of Corporate Tax Rates

Only four tax jurisdictions impose a corporate income tax at statutory rates greater than 35 percent. [20] The following chart shows a distribution of corporate income tax rates among 226 jurisdictions in 2025. A plurality of countries (126 total) impose a rate above 20 percent and below or at 30 percent. Sixteen jurisdictions have a statutory corporate tax rate above 30 percent and below or at 35 percent. Eighty jurisdictions have a statutory corporate tax rate below or at 20 percent, and 206 jurisdictions have a corporate tax rate below or at 30 percent.

The Decline of Corporate Tax Rates since 1980 Leveled Off in Recent Years

Over the past 45 years, corporate tax rates have consistently declined on a global basis. In 1980, the unweighted average worldwide statutory tax rate was 40.18 percent. Today, the average statutory rate stands at 23.58 percent—a 41.3 percent reduction—and 23.96 percent when accounting for the global minimum tax.[21]

Despite a general decline in corporate tax rates around the world, OECD and non-OECD countries have also become more reliant on revenue from corporate income taxes.[22] One cause for this change has been a shift in the jurisdictions included.[23] Secondly, the negative revenue impact of the decline in corporate tax rates was generally offset by reducing or abolishing tax relief policies.[24]

The weighted average statutory rate has remained higher than the simple average over this period. Prior to US tax reform in 2017, the United States was largely responsible for keeping the weighted average higher, given its relatively high tax rate, as well as its significant contribution to global GDP. Figure 4 shows the significant impact the change in the US corporate rate had on the worldwide weighted average. The weighted average statutory corporate income tax rate has declined from 46.66 percent in 1980 to 26.04 percent (26.12 percent when accounting for the global minimum tax) in 2025, representing a 44 percent reduction over the 45 years surveyed.

Over time, more countries have shifted to taxing corporations at rates of 30 percent or lower, with the United States following this trend with its tax changes at the end of 2017. The largest shift occurred between 1990 and 2000, with 49 percent of countries imposing a statutory rate below 30 percent in 2000 and only 27 percent of countries in the dataset imposing a statutory rate below 30 percent in 1990. This trend continued between 2000 and 2010, with 79 percent of countries imposing a statutory rate below 30 percent in 2010. Currently, 91 percent of countries impose a statutory rate below 30 percent.[25]

All regions saw a net decline in average statutory rates between 1980 and 2025. The average declined the most in Europe, with the 1980 average of 44.6 percent dropping to 20.65 percent (21.19 percent when accounting for the global minimum tax)—a 54 percent decline. South America has seen the smallest decline, with the average only decreasing by 23 percent, from 36.66 percent in 1980 to 28.38 percent in 2025.

South America saw two periods, 1990-2000 and 2010-2025, during which the average statutory rate increased slightly by less than 0.5 percentage points, although the average rate decreased over the full 45-year period.

Conclusion

Worldwide and regional average top statutory corporate tax rates have declined over the past four decades due to countries turning to more efficient tax types.[26] However, they have leveled off in recent years. Of the 226 jurisdictions around the world, eight have increased their top corporate income tax rates in 2025, while four low-tax jurisdictions and five jurisdictions without a corporate tax raised their effective corporate tax rates by implementing the global minimum tax, a trend that might continue in the coming years as more countries will be implementing the global minimum tax.

Table 6. Statutory Top Corporate Tax Rates and Pillar Two Implementation Around the World, 2025

| ISO 3 | Continent | Country | Corporate Tax Rate | Tax Rate Accounting for Global Minimum Tax | Joined the Pillar Two Statement | Income Inclusion Rule (IIR) | Undertaxed Profits Rule (UTPR) | Qualified Domestic Minimum Top-up Tax (QDMTT) |

|---|---|---|---|---|---|---|---|---|

| ABW | NO | Aruba | 22.00% | 22.00% | No | No | No | No |

| AFG | AS | Afghanistan | 20.00% | 20.00% | No | No | No | No |

| AGO | AF | Angola | 25.00% | 25.00% | Yes | No | No | No |

| AIA | NO | Anguilla | 0.00% | 0.00% | No | No | No | No |

| ALA | EU | Aland Islands | 20.00% | 20.00% | No | No | No | No |

| ALB | EU | Albania | 15.00% | 15.00% | Yes | No | No | No |

| AND | EU | Andorra | 10.00% | 10.00% | No | No | No | No |

| ARE | AS | United Arab Emirates | 9.00% | 15.00% | Yes | No | No | Yes |

| ARG | SA | Argentina | 35.00% | 35.00% | Yes | No | No | No |

| ARM | AS | Armenia | 18.00% | 18.00% | Yes | No | No | No |

| ASM | OC | American Samoa | 34.00% | 34.00% | No | No | No | No |

| ATG | NO | Antigua and Barbuda | 25.00% | 25.00% | Yes | No | No | No |

| AUS | OC | Australia | 30.00% | 30.00% | Yes | Yes | Yes | Yes |

| AUT | EU | Austria | 23.00% | 23.00% | Yes | Yes | Yes | Yes |

| AZE | AS | Azerbaijan | 20.00% | 20.00% | Yes | No | No | No |

| BDI | AF | Burundi | 30.00% | 30.00% | No | No | No | No |

| BEL | EU | Belgium | 25.00% | 25.00% | Yes | Yes | Yes | Yes |

| BEN | AF | Benin | 30.00% | 30.00% | No | No | No | No |

| BES | NO | Bonaire, Sint Eustatius and Saba | 25.80% | 25.80% | No | No | No | No |

| BFA | AF | Burkina Faso | 27.50% | 27.50% | No | No | No | No |

| BGD | AS | Bangladesh | 27.50% | 27.50% | No | No | No | No |

| BGR | EU | Bulgaria | 10.00% | 15.00% | Yes | Yes | Yes | Yes |

| BHR | AS | Bahrain | 0.00% | 15.00% | Yes | No | No | Yes |

| BHS | NO | Bahamas | 0.00% | 15.00% | Yes | No | No | Yes |

| BIH | EU | Bosnia and Herzegovina | 10.00% | 10.00% | Yes | No | No | No |

| BLM | NO | Saint Barthelemy | 0.00% | 0.00% | No | No | No | No |

| BLR | EU | Belarus | 25.00% | 25.00% | No | No | No | No |

| BLZ | NO | Belize | 0.00% | 0.00% | No | No | No | No |

| BMU | NO | Bermuda | 0.00% | 15.00% | Yes | No | No | Yes |

| BOL | SA | Plurinational State of Bolivia | 25.00% | 25.00% | No | No | No | No |

| BRA | SA | Brazil | 34.00% | 34.00% | Yes | No | No | Yes |

| BRB | NO | Barbados | 9.00% | 15.00% | Yes | No | No | Yes |

| BRN | AS | Brunei Darussalam | 18.50% | 18.50% | No | No | No | No |

| BTN | AS | Bhutan | 25.00% | 25.00% | No | No | No | No |

| BWA | AF | Botswana | 22.00% | 22.00% | No | No | No | No |

| CAF | AF | Central African Republic | 30.00% | 30.00% | No | No | No | No |

| CAN | NO | Canada | 25.98% | 25.98% | Yes | Yes | Yes | Yes |

| CHE | EU | Switzerland | 19.61% | 19.61% | Yes | Yes | No | Yes |

| CHL | SA | Chile | 27.00% | 27.00% | Yes | No | No | No |

| CHN | AS | China | 25.00% | 25.00% | Yes | No | No | No |

| CIV | AF | Cote d'Ivoire | 25.00% | 25.00% | No | No | No | No |

| CMR | AF | Cameroon | 33.00% | 33.00% | Yes | No | No | No |

| COD | AF | Democratic Republic of the Congo | 30.00% | 30.00% | Yes | No | No | No |

| COG | AF | Congo | 28.00% | 28.00% | Yes | No | No | No |

| COK | OC | Cook Islands | 20.00% | 20.00% | No | No | No | No |

| COL | SA | Colombia | 35.00% | 35.00% | Yes | No | No | No |

| COM | AF | Comoros | 50.00% | 50.00% | No | No | No | No |

| CPV | AF | Cabo Verde | 21.42% | 21.42% | Yes | No | No | No |

| CRI | NO | Costa Rica | 30.00% | 30.00% | Yes | No | No | No |

| CUB | NO | Cuba | 35.00% | 35.00% | No | No | No | No |

| CUW | NO | Curacao | 22.00% | 22.00% | Yes | Yes | No | Yes |

| CYM | NO | Cayman Islands | 0.00% | 0.00% | Yes | No | No | No |

| CYP | EU | Cyprus | 12.50% | 15.00% | No | Yes | Yes | Yes |

| CZE | EU | Czechia | 21.00% | 21.00% | Yes | Yes | Yes | Yes |

| DEU | EU | Germany | 30.06% | 30.06% | Yes | Yes | Yes | Yes |

| DJI | AF | Djibouti | 25.00% | 25.00% | No | No | No | No |

| DMA | NO | Dominica | 25.00% | 25.00% | Yes | No | No | No |

| DNK | EU | Denmark | 22.00% | 22.00% | Yes | Yes | Yes | Yes |

| DOM | NO | Dominican Republic | 27.00% | 27.00% | Yes | No | No | No |

| DZA | AF | Algeria | 26.00% | 26.00% | No | No | No | No |

| ECU | SA | Ecuador | 25.00% | 25.00% | No | No | No | No |

| EGY | AF | Egypt | 22.50% | 22.50% | Yes | No | No | No |

| ERI | AF | Eritrea | 30.00% | 30.00% | No | No | No | No |

| ESP | EU | Spain | 25.00% | 25.00% | Yes | Yes | Yes | Yes |

| EST | EU | Estonia | 22.00% | 22.00% | Yes | No | No | No |

| ETH | AF | Ethiopia | 30.00% | 30.00% | No | No | No | No |

| FIN | EU | Finland | 20.00% | 20.00% | Yes | Yes | Yes | Yes |

| FJI | OC | Fiji | 25.00% | 25.00% | No | No | No | No |

| FLK | SA | Falkland Islands (Malvinas) | 26.00% | 26.00% | No | No | No | No |

| FRA | EU | France | 36.13% | 36.13% | Yes | Yes | Yes | Yes |

| FRO | EU | Faroe Islands | 18.00% | 18.00% | No | No | No | No |

| FSM | OC | Federated States of Micronesia | 30.00% | 30.00% | No | No | No | No |

| GAB | AF | Gabon | 30.00% | 30.00% | No | No | No | No |

| GBR | EU | United Kingdom of Great Britain and Northern Ireland | 25.00% | 25.00% | Yes | Yes | Yes | Yes |

| GEO | AS | Georgia | 15.00% | 15.00% | Yes | No | No | No |

| GGY | EU | Guernsey | 0.00% | 15.00% | Yes | Yes | No | Yes |

| GHA | AF | Ghana | 25.00% | 25.00% | No | No | No | No |

| GIB | EU | Gibraltar | 15.00% | 15.00% | Yes | Yes | No | Yes |

| GIN | AF | Guinea | 25.00% | 25.00% | No | No | No | No |

| GMB | AF | Gambia | 27.00% | 27.00% | No | No | No | No |

| GNB | AF | Guinea-Bissau | 25.00% | 25.00% | No | No | No | No |

| GNQ | AF | Equatorial Guinea | 25.00% | 25.00% | No | No | No | No |

| GRC | EU | Greece | 22.00% | 22.00% | Yes | Yes | Yes | Yes |

| GRD | NO | Grenada | 28.00% | 28.00% | No | No | No | No |

| GRL | NO | Greenland | 26.50% | 26.50% | Yes | No | No | No |

| GTM | NO | Guatemala | 25.00% | 25.00% | No | No | No | No |

| GUM | OC | Guam | 21.00% | 21.00% | No | No | No | No |

| GUY | SA | Guyana | 25.00% | 25.00% | No | No | No | No |

| HKG | AS | China, Hong Kong Special Administrative Region | 16.50% | 16.50% | Yes | Yes | No | Yes |

| HND | NO | Honduras | 30.00% | 30.00% | Yes | No | No | No |

| HRV | EU | Croatia | 18.00% | 18.00% | Yes | Yes | Yes | Yes |

| HTI | NO | Haiti | 30.00% | 30.00% | No | No | No | No |

| HUN | EU | Hungary | 9.00% | 15.00% | Yes | Yes | Yes | Yes |

| IDN | AS | Indonesia | 22.00% | 22.00% | Yes | Yes | No | Yes |

| IMN | EU | Isle of Man | 0.00% | 15.00% | Yes | Yes | No | Yes |

| IND | AS | India | 30.00% | 30.00% | Yes | No | No | No |

| IRL | EU | Ireland | 12.50% | 15.00% | Yes | Yes | Yes | Yes |

| IRN | AS | Islamic Republic of Iran | 25.00% | 25.00% | No | No | No | No |

| IRQ | AS | Iraq | 15.00% | 15.00% | No | No | No | No |

| ISL | EU | Iceland | 20.00% | 20.00% | Yes | No | No | No |

| ISR | AS | Israel | 23.00% | 23.00% | Yes | No | No | No |

| ITA | EU | Italy | 27.81% | 27.81% | Yes | Yes | Yes | Yes |

| JAM | NO | Jamaica | 25.00% | 25.00% | Yes | No | No | No |

| JEY | EU | Jersey | 0.00% | 15.00% | Yes | Yes | No | Yes |

| JOR | AS | Jordan | 20.00% | 20.00% | Yes | No | No | No |

| JPN | AS | Japan | 29.74% | 29.74% | Yes | Yes | No | No |

| KAZ | AS | Kazakhstan | 20.00% | 20.00% | Yes | No | No | No |

| KEN | AF | Kenya | 30.00% | 30.00% | No | No | No | Yes |

| KGZ | AS | Kyrgyzstan | 10.00% | 10.00% | No | No | No | No |

| KHM | AS | Cambodia | 20.00% | 20.00% | No | No | No | No |

| KIR | OC | Kiribati | 30.00% | 30.00% | No | No | No | No |

| KNA | NO | Saint Kitts and Nevis | 33.00% | 33.00% | Yes | No | No | No |

| KOR | AS | Republic of Korea | 26.40% | 26.40% | Yes | Yes | Yes | No |

| KWT | AS | Kuwait | 15.00% | 15.00% | No | No | No | Yes |

| LAO | AS | Lao People's Democratic Republic | 20.00% | 20.00% | No | No | No | No |

| LBN | AS | Lebanon | 17.00% | 17.00% | No | No | No | No |

| LBR | AF | Liberia | 25.00% | 25.00% | Yes | No | No | No |

| LBY | AF | Libya | 20.00% | 20.00% | No | No | No | No |

| LCA | NO | Saint Lucia | 30.00% | 30.00% | Yes | No | No | No |

| LIE | EU | Liechtenstein | 12.50% | 15.00% | Yes | Yes | No | Yes |

| LKA | AS | Sri Lanka | 30.00% | 30.00% | No | No | No | No |

| LSO | AF | Lesotho | 25.00% | 25.00% | No | No | No | No |

| LTU | EU | Lithuania | 16.00% | 16.00% | Yes | No | No | No |

| LUX | EU | Luxembourg | 23.87% | 23.87% | Yes | Yes | Yes | Yes |

| LVA | EU | Latvia | 20.00% | 20.00% | Yes | No | No | No |

| MAC | AS | China, Macao Special Administrative Region | 12.00% | 12.00% | No | No | No | No |

| MAF | NO | Saint Martin (French Part) | 20.00% | 20.00% | No | No | No | No |

| MAR | AF | Morocco | 34.00% | 34.00% | No | No | No | No |

| MCO | EU | Monaco | 25.00% | 25.00% | No | No | No | No |

| MDA | EU | Republic of Moldova | 12.00% | 12.00% | No | No | No | No |

| MDG | AF | Madagascar | 20.00% | 20.00% | No | No | No | No |

| MDV | AS | Maldives | 15.00% | 15.00% | No | No | No | No |

| MEX | NO | Mexico | 30.00% | 30.00% | Yes | No | No | No |

| MKD | EU | North Macedonia | 10.00% | 15.00% | Yes | Yes | Yes | Yes |

| MLI | AF | Mali | 30.00% | 30.00% | No | No | No | No |

| MLT | EU | Malta | 35.00% | 35.00% | Yes | No | No | No |

| MMR | AS | Myanmar | 22.00% | 22.00% | No | No | No | No |

| MNE | EU | Montenegro | 15.00% | 15.00% | Yes | No | No | No |

| MNG | AS | Mongolia | 25.00% | 25.00% | Yes | No | No | No |

| MNP | OC | Northern Mariana Islands | 21.00% | 21.00% | No | No | No | No |

| MOZ | AF | Mozambique | 32.00% | 32.00% | No | No | No | No |

| MRT | AF | Mauritania | 25.00% | 25.00% | No | No | No | No |

| MSR | NO | Montserrat | 30.00% | 30.00% | No | No | No | No |

| MUS | AF | Mauritius | 15.00% | 15.00% | Yes | No | No | Yes |

| MWI | AF | Malawi | 30.00% | 30.00% | No | No | No | No |

| MYS | AS | Malaysia | 24.00% | 24.00% | Yes | Yes | No | Yes |

| NAM | AF | Namibia | 30.00% | 30.00% | Yes | No | No | No |

| NCL | OC | New Caledonia | 30.00% | 30.00% | No | No | No | No |

| NER | AF | Niger | 30.00% | 30.00% | No | No | No | No |

| NGA | AF | Nigeria | 30.00% | 30.00% | No | No | No | No |

| NIC | NO | Nicaragua | 30.00% | 30.00% | No | No | No | No |

| NIU | OC | Niue | 30.00% | 30.00% | No | No | No | No |

| NLD | EU | Netherlands | 25.80% | 25.80% | Yes | Yes | Yes | Yes |

| NOR | EU | Norway | 22.00% | 22.00% | Yes | Yes | Yes | Yes |

| NPL | AS | Nepal | 25.00% | 25.00% | No | No | No | No |

| NRU | OC | Nauru | 25.00% | 25.00% | No | No | No | No |

| NZL | OC | New Zealand | 28.00% | 28.00% | Yes | Yes | Yes | No |

| OMN | AS | Oman | 15.00% | 15.00% | Yes | Yes | No | No |

| PAK | AS | Pakistan | 29.00% | 29.00% | No | No | No | No |

| PAN | NO | Panama | 25.00% | 25.00% | Yes | No | No | No |

| PER | SA | Peru | 29.50% | 29.50% | Yes | No | No | No |

| PHL | AS | Philippines | 25.00% | 25.00% | No | No | No | No |

| PNG | OC | Papua New Guinea | 30.00% | 30.00% | Yes | No | No | No |

| POL | EU | Poland | 19.00% | 19.00% | Yes | Yes | Yes | Yes |

| PRI | NO | Puerto Rico | 37.50% | 37.50% | No | No | No | No |

| PRT | EU | Portugal | 30.50% | 30.50% | Yes | Yes | Yes | Yes |

| PRY | SA | Paraguay | 10.00% | 10.00% | Yes | No | No | No |

| PSE | AS | State of Palestine | 15.00% | 15.00% | No | No | No | No |

| PYF | OC | French Polynesia | 25.00% | 25.00% | No | No | No | No |

| QAT | AS | Qatar | 10.00% | 15.00% | Yes | No | No | Yes |

| ROU | EU | Romania | 16.00% | 16.00% | Yes | Yes | Yes | Yes |

| RUS | EU | Russian Federation | 25.00% | 25.00% | No | No | No | No |

| RWA | AF | Rwanda | 28.00% | 28.00% | No | No | No | No |

| SAU | AS | Saudi Arabia | 20.00% | 20.00% | Yes | No | No | No |

| SDN | AF | Sudan | 35.00% | 35.00% | No | No | No | No |

| SEN | AF | Senegal | 30.00% | 30.00% | Yes | No | No | No |

| SGP | AS | Singapore | 17.00% | 17.00% | Yes | Yes | No | Yes |

| SHN | AF | Saint Helena | 25.00% | 25.00% | No | No | No | No |

| SLB | OC | Solomon Islands | 30.00% | 30.00% | No | No | No | No |

| SLE | AF | Sierra Leone | 25.00% | 25.00% | Yes | No | No | No |

| SLV | NO | El Salvador | 30.00% | 30.00% | No | No | No | No |

| SMR | EU | San Marino | 17.00% | 17.00% | No | No | No | No |

| SOM | AF | Somalia | 15.00% | 15.00% | No | No | No | No |

| SRB | EU | Serbia | 15.00% | 15.00% | Yes | No | No | No |

| SSD | AF | South Sudan | 30.00% | 30.00% | No | No | No | No |

| STP | AF | Sao Tome and Principe | 25.00% | 25.00% | No | No | No | No |

| SUR | SA | Suriname | 36.00% | 36.00% | No | No | No | No |

| SVK | EU | Slovakia | 24.00% | 24.00% | Yes | No | No | Yes |

| SVN | EU | Slovenia | 22.00% | 22.00% | Yes | Yes | Yes | Yes |

| SWE | EU | Sweden | 20.60% | 20.60% | Yes | Yes | Yes | Yes |

| SWZ | AF | Swaziland | 25.00% | 25.00% | Yes | No | No | No |

| SXM | NO | Sint Maarten (Dutch part) | 34.50% | 34.50% | No | No | No | No |

| SYC | AF | Seychelles | 25.00% | 25.00% | Yes | No | No | No |

| SYR | AS | Syrian Arab Republic | 25.00% | 25.00% | No | No | No | No |

| TCA | NO | Turks and Caicos Islands | 0.00% | 0.00% | No | No | No | No |

| TCD | AF | Chad | 35.00% | 35.00% | No | No | No | No |

| TGO | AF | Togo | 27.00% | 27.00% | No | No | No | No |

| THA | AS | Thailand | 20.00% | 20.00% | Yes | Yes | Yes | Yes |

| TJK | AS | Tajikistan | 18.00% | 18.00% | No | No | No | No |

| TKL | OC | Tokelau | 0.00% | 0.00% | No | No | No | No |

| TKM | AS | Turkmenistan | 8.00% | 8.00% | No | No | No | No |

| TLS | OC | Timor-Leste | 10.00% | 10.00% | No | No | No | No |

| TON | OC | Tonga | 25.00% | 25.00% | No | No | No | No |

| TTO | NO | Trinidad and Tobago | 30.00% | 30.00% | Yes | No | No | No |

| TUN | AF | Tunisia | 20.00% | 20.00% | Yes | No | No | No |

| TUR | AS | Turkey | 25.00% | 25.00% | Yes | Yes | Yes | Yes |

| TWN | AS | Taiwan | 20.00% | 20.00% | No | No | No | No |

| TZA | AF | United Republic of Tanzania | 30.00% | 30.00% | No | No | No | No |

| UGA | AF | Uganda | 30.00% | 30.00% | No | No | No | No |

| UKR | EU | Ukraine | 18.00% | 18.00% | Yes | No | No | No |

| URY | SA | Uruguay | 25.00% | 25.00% | Yes | No | No | No |

| USA | NO | United States of America | 25.57% | 25.57% | Yes | No | No | No |

| UZB | AS | Uzbekistan | 15.00% | 15.00% | Yes | No | No | No |

| VCT | NO | Saint Vincent and the Grenadines | 28.00% | 28.00% | Yes | No | No | No |

| VEN | SA | Bolivarian Republic of Venezuela | 34.00% | 34.00% | No | No | No | No |

| VGB | NO | British Virgin Islands | 0.00% | 0.00% | Yes | No | No | No |

| VIR | NO | United States Virgin Islands | 23.10% | 23.10% | No | No | No | No |

| VNM | AS | Viet Nam | 20.00% | 20.00% | Yes | Yes | No | Yes |

| VUT | OC | Vanuatu | 0.00% | 0.00% | No | No | No | No |

| WLF | OC | Wallis and Futuna Islands | 0.00% | 0.00% | No | No | No | No |

| WSM | OC | Samoa | 27.00% | 27.00% | No | No | No | No |

| XKX | EU | Republic of Kosovo | 10.00% | 10.00% | No | No | No | No |

| YEM | AS | Yemen | 20.00% | 20.00% | No | No | No | No |

| ZAF | AF | South Africa | 27.00% | 27.00% | Yes | Yes | No | Yes |

| ZMB | AF | Zambia | 30.00% | 30.00% | Yes | No | No | No |

| ZWE | AF | Zimbabwe | 25.75% | 25.75% | No | No | No | Yes |

Source: Statutory corporate income tax rates are from OECD, “Corporate income tax statutory and targeted small business rates”; PwC, “Worldwide Tax Summaries – Corporate Taxes”; Bloomberg Tax, “Country Guides – Corporate Tax Rates”; and some jurisdictions researched individually, see Tax Foundation, “worldwide-corporate-tax-rates.” Tax Rate Accounting for Global Minimum Tax was calculated based on PwC, “Pillar Two Country Tracker,” accessed Dec. 2, 2025. https://pwc.com/gx/en/services/tax/pillar-two-readiness/country-tracker.html.

Subscribe to our free newsletter to get the latest tax data, news and analysis.Stay informed on the tax policies impacting you.

Appendix

The Dataset

Scope

The dataset compiled for this publication includes the 2025 statutory corporate income tax rates of 226 sovereign states and dependent territories around the world. Tax rates were researched only for jurisdictions that are among the around 250 sovereign states and dependent territories that have been assigned a country code by the International Organization for Standardization (ISO). As a result, zones or territories that are independent taxing jurisdictions but do not have their own country code are generally not included in the dataset.

In addition, the dataset includes historic statutory corporate income tax rates from 1980 to 2024. However, these years cover tax rates of fewer than 226 jurisdictions due to missing data points. Please let Tax Foundation know if you are aware of any sources for historic corporate tax rates that are not mentioned in this report, as we constantly strive to improve our datasets.

To be able to calculate average statutory corporate income tax rates weighted by GDP, the dataset includes GDP data for 181 jurisdictions. When used to calculate average statutory corporate income tax rates, either weighted by GDP or unweighted, only these 181 jurisdictions are included (to ensure the comparability of the unweighted and weighted averages).

Definition of Selected Corporate Income Tax Rate

The dataset captures standard top statutory corporate income tax rates levied on domestic businesses. This means:

- The dataset does not reflect special tax regimes, including but not limited to patent boxes, offshore regimes, or special rates for specific industries.

- A number of countries levy lower rates for businesses below a certain revenue threshold. The dataset does not capture these lower rates.

- A few countries levy gross revenue taxes on businesses instead of corporate income taxes. Since the tax rates of a corporate income tax and a gross revenue tax are not comparable, these countries are excluded from the dataset.

- Some countries have a separate tax rate for nonresident companies. This dataset does not consider nonresident tax rates that differ from the general corporate rate.

Sources

Tax Rates for the Year 2025

For OECD and non-OECD countries, the statutory corporate income tax rates used are the combined corporate income tax rates provided by the OECD; see OECD, “Corporate income tax statutory and targeted small business rates,” updated April 2025. Another source used for non-OECD jurisdictions is the statutory rates provided by PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2025, https://taxsummaries.pwc.com/. The study also relies on Bloomberg Tax, “Country Guides – Corporate Tax Rates,” accessed in November 2025, https://www.bloomberglaw.com/product/tax/toc_view_menu/3380. Jurisdictions that are not part of these sources were researched individually. The source for each of these jurisdictions is listed in a GitHub repository; see Tax Foundation, “worldwide-corporate-tax-rates,” GitHub, https://github.com/TaxFoundation/worldwide-corporate-tax-rates.

To calculate the 2025 tax rates accounting for the global minimum tax, the Pillar Two country tracker was used; see PwC, “Pillar Two Country Tracker,” accessed Dec. 2, 2025, https://pwc.com/gx/en/services/tax/pillar-two-readiness/country-tracker.html.

Tax Rates for the Years 1980-2024

Tax rates for the time frame between 1980 and 2024 are taken from a dataset compiled by the Tax Foundation over the last few years. These historic rates come from multiple sources: PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2010-2024; KPMG, “Corporate Tax Rate Survey,” 1998- 2003; KPMG, “Corporate tax rates table,” 2003-2019; EY, “Worldwide Corporate Tax Guide,” 2004-2019; OECD, “Historical Table II.1 – Statutory corporate income tax rate,” 1999, https://data-explorer.oecd.org/vis?tenant=archive&df[ds]=DisseminateArchiveDMZ&df[id]=DF_TABLE_II1&df[ag]=OECD&dq=.&lom=LASTNPERIODS&lo=5&to[TIME_PERIOD]=false; the University of Michigan – Ross School of Business, “World Tax Database,” https://www.bus.umich.edu/otpr/otpr/default.asp; and numerous government websites.

Gross Domestic Product (GDP) for the Years 1980-2025

GDP calculations are from the US Department of Agriculture, “International Macroeconomics Data Set- Historical and projected real gross domestic product (GDP) and growth rates of GDP for baseline countries/regions (in billions of 2017 dollars) 1970-2034,” Nov. 15 , 2024, https://www.ers.usda.gov/data-products/international-macroeconomic-data-set/.

References

[1] Unless otherwise noted, calculated averages of statutory corporate income tax rates only include jurisdictions for which GDP data is available for all years between 1980 and 2025. For 2025, the dataset includes statutory corporate income tax rates of 226 jurisdictions, but GDP data is available for only 181 of these jurisdictions, reducing the number of jurisdictions included in calculated averages to 181. For years prior to 2025, the number of countries included in calculated averages varies by year due to missing corporate tax rates; that is, the 1980 average includes statutory corporate income tax rates of 75 jurisdictions, compared to 181 jurisdictions in 2025.

[2] Statutory rates are from OECD, “Corporate income tax statutory and targeted small business rates,” updated April 2025; PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2025, https://taxsummaries.pwc.com/; Bloomberg Tax, “Country Guides – Corporate Tax Rates,” accessed November 2023, https://www.bloomberglaw.com/product/tax/toc_view_menu/3380; and researched individually, see Tax Foundation, “worldwide-corporate-tax-rates,” GitHub, https://github.com/TaxFoundation/worldwide-corporate-tax-rates. Tax rates accounting for global minimum tax were calculated based on PwC, “Pillar Two Country Tracker,” accessed Dec. 2, 2025, https://pwc.com/gx/en/services/tax/pillar-two-readiness/country-tracker.html. GDP calculations are from the US Department of Agriculture, “International Macroeconomics Data Set,” Nov. 15, 2024, https://www.ers.usda.gov/data-products/international-macroeconomic-data-set/.

[3] By 2025, nine jurisdictions with statutory corporate tax rates below 15 percent and five jurisdictions without a corporate income tax implemented the qualified domestic minimum top-up tax from the Pillar Two rules, raising their effective corporate tax rate to 15 percent. See PwC, “Pillar Two Country Tracker,” accessed Dec. 2, 2025, https://pwc.com/gx/en/services/tax/pillar-two-readiness/country-tracker.html.

[4] Kari Jahnsen and Kyle Pomerleau, “Corporate Income Tax Rates around the World, 2017,” Tax Foundation, Sep. 7, 2017, https://taxfoundation.org/corporate-income-tax-rates-around-the-world-2017/.

[5] PwC, “Worldwide Tax Summaries – Estonia,” 2025, https://taxsummaries.pwc.com/estonia/corporate/significant-developments.

[6] PwC, “Worldwide Tax Summaries – Germany,” 2025, https://taxsummaries.pwc.com/germany/corporate/significant-developments.

[7] KPMG, “Lithuania: Amendments to corporate income taxation effective January 1, 2026,” 2025, https://kpmg.com/us/en/taxnewsflash/news/2025/10/tnf-lithuania-amendments-to-corporate-income-taxation-effective-january-1-2026.html.

[8] PwC, “Worldwide Tax Summaries – Morocco,” 2025, https://taxsummaries.pwc.com/morocco/corporate/significant-developments.

[9] PwC, “Worldwide Tax Summaries – Portugal,” 2025, https://taxsummaries.pwc.com/portugal/corporate/significant-developments.

[10] PwC, “Worldwide Tax Summaries – Slovenia,” 2025, https://taxsummaries.pwc.com/slovenia/corporate/taxes-on-corporate-income.

[11] PwC, “Worldwide Tax Summaries – Bermuda,” 2025, https://taxsummaries.pwc.com/bermuda/corporate/significant-developments.

[12]PwC, “Pillar Two Country Tracker,” accessed Dec. 2, 20254, https://pwc.com/gx/en/services/tax/pillar-two-readiness/country-tracker.html.

[13]Alex Mengden, “Pillar Two Implementation in Europe, 2025,” Tax Foundation, Oct. 30, 2025, https://taxfoundation.org/data/all/eu/pillar-two-implementation-europe/.

[14] PwC, “Pillar Two Country Tracker,” accessed Dec. 2, 2025, https://pwc.com/gx/en/services/tax/pillar-two-readiness/country-tracker.html.

[15] Bloomberg Tax, “Tax Havens Race to Lure Companies as 15% Global Levy Looms,” Dec. 6. 2023, https://news.bloombergtax.com/daily-tax-report-international/tax-havens-race-to-lure-companies-as-15-global-levy-looms.

[16] As no averages are presented in this section, it covers all 226 jurisdictions for which corporate income tax rates were found in 2025 (thus including jurisdictions for which GDP data was not available).

[17] This average is lower than the average of the 181 jurisdictions because many of the jurisdictions for which no GDP data is available are small economies with low corporate income tax rates.

[18] Where applicable, similar combinations of national and subnational rates are included in this dataset. For example, the combined German corporate tax rate is 30.06 percent, which includes both the federal rate of 15 percent and municipal trade taxes ranging from 8.75 to 20.3 percent.

[19] BRICS is a group of countries with major emerging economies. The members of this group are Brazil, Russia, India, China, and South Africa.

[20] As no averages are presented in this chapter, it covers all 226 jurisdictions for which 2025 corporate income tax rates were found (thus including jurisdictions for which GDP data was not available).

[21] Historical data comes from multiple sources: PwC, “Worldwide Tax Summaries – Corporate Taxes,” 2010-2019; KPMG, “Corporate Tax Rate Survey,” 1998- 2003; KPMG, “Corporate tax rates table,” 2003-2019; EY, “Worldwide Corporate Tax Guide,” 2004-2019; OECD, “Historical Table II.1 – Statutory corporate income tax rate,” 1999, https://data-explorer.oecd.org/vis?tenant=archive&df[ds]=DisseminateArchiveDMZ&df[id]=DF_TABLE_II1&df[ag]=OECD&dq=.&lom=LASTNPERIODS&lo=5&to[TIME_PERIOD]=falsehttp://www.oecd.org/tax/tax-policy/tax-database.htm; University of Michigan – Ross School of Business, “World Tax Database,” https://www.bus.umich.edu/otpr/otpr/default.asp; and numerous government websites.

[22] The average of the corporate income tax revenues as a share of total tax revenues increased from 10 percent in 1990 to 17.4 percent in 2023, and the average of the corporate income tax revenues as a percentage of GDP increased from 2.3 percent in 1990 to 3.5 percent in 2023. See OECD, “Global Revenue Statistics – Comparative tax revenues.”

[23] Cristina Enache, “Sources of Government Revenue in the OECD,” Tax Foundation, 2025, https://taxfoundation.org/data/all/global/oecd-tax-revenue-by-country/.

[24] OECD, “Revenue Statistics 2024: Health Taxes in OECD Countries,” OECD Publishing, 2024, https://doi.org/10.1787/c87a3da5-en.

[25] This section of the report covers all 226 jurisdictions for which 2025 corporate income tax rates were found (thus including jurisdictions for which GDP data was not available).

[26] Asa Johansson, Christopher Heady, Jens Arnold, Bert Brys, and Laura Vartia, “Tax and Economic Growth,” OECD, Jul. 11, 2008, https://www.oecd.org/tax/tax-policy/41000592.pdf; see also, Alex Durante, “Reviewing Recent Evidence of the Effect of Taxes on Economic Growth,” Tax Foundation, May 21, 2021, https://taxfoundation.org/reviewing-recent-evidence-effect-taxes-economic-growth/.

Share this article