Tennessee forgoes an individual income tax, having phased out a narrow tax on interest and dividend income, known as the Hall Tax, in 2021. However, Tennessee is among the minority of states that still have a capital stock tax on the books, despite making structural improvements to it during the 2024 legislative session. Tennessee businesses also face an additional layer of tax on their gross receipts, and not just their net income (profits).

Tennessee excludes most, but not all, net CFC-tested income (NCTI), formerly global intangible low-taxed income (GILTI), from its tax base, and caps net operating loss carryforwards at 15 years, whereas most states have 20-year or unlimited carryforwards. The state recently conformed to the Tax Cuts and Jobs Act’s treatment of first-year expensing under Section 168(k), but did so in such a way that maintains the phasedown that was reversed under the One Big Beautiful Bill Act (OBBBA).

Tennessee has among the highest combined state and average local sales tax rates in the nation. The largest portion of the sales tax burden comes from the 7 percent state-level sales tax rate, which is second only to California’s 7.25 percent rate (and tied with the state sales tax rates in Indiana, Mississippi, and Rhode Island). Because income taxes have a greater impact on economic growth than sales taxes, however, Tennessee’s decision to rely on high sales taxes in lieu of income taxes is an economically advantageous one.

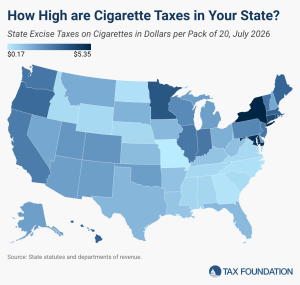

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.