Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readNew Jersey levies all major categories of tax, typically at high rates and significant levels of complexity.

In 1976, the Garden State enacted an individual income tax, in part to provide relief from rising property taxes. Now, individual taxpayers are subject to seven individual income tax brackets, a top marginal rate of 10.75 percent, and among the highest per capita property tax collections in the nation. Moreover, individual taxpayers are subject to a marriage penalty. New Jersey property taxpayers also pay the third-highest effective rate in the country. The state repealed its estate tax but continues to levy an inheritance tax.

Corporations face a top marginal tax rate of 11.5 percent, taking into account a surtax on large businesses known as the Corporate Transit Fee. Recently, however, New Jersey has largely removed global intangible low-taxed income (GILTI) from its tax base, and tangible personal property is exempt from property taxation. Additionally, the state allows up to 20 years of net operating loss carryforwards without placing a cap on the dollar amount allowed.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 49 | 0 | 3.71 |

| Corporate Taxes | 44 | 0 | 4.30 |

| Individual Income Taxes | 48 | 0 | 2.64 |

| Sales Taxes | 34 | 0 | 4.38 |

| Property Taxes | 42 | 1 | 4.13 |

| Unemployment Insurance Taxes | 46 | 4 | 3.84 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

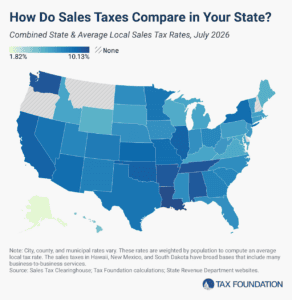

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read