Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readMichigan’s tax code includes all major tax types and has traditionally ranked well on the Index. The state’s individual income tax is flat with a relatively low rate of 4.25 percent, along with a modest personal exemption. However, Michigan faces significant regional competition, as Indiana, Ohio, and Pennsylvania all have lower state individual income tax rates, although all four states authorize localities to impose local income taxes.

Michigan has a flat 6 percent corporate income tax, which is close to the national average. The state has no throwback rule or capital stock tax, and, unlike Ohio, it does not impose a gross receipts tax. However, the state does not offer full expensing, which could be an important element of future pro-growth reforms aimed at attracting capital-intensive businesses.

The state’s sales tax rate is 6 percent, lower than in all other Midwestern states except Wisconsin. Michigan does not authorize cities and counties to impose local option sales taxes, simplifying the consumption tax system compared to most other states.

Michigan’s property tax system is reasonably competitive with an average property tax burden. The state taxes tangible personal property but offers a generous de minimis exemption of $180,000, reducing compliance costs for small businesses. Michigan also does not impose estate, inheritance, or gift taxes, making it more attractive for high-net-worth individuals.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 16 | -2 | 5.44 |

| Corporate Taxes | 22 | -14 | 5.39 |

| Individual Income Taxes | 19 | -5 | 5.70 |

| Sales Taxes | 10 | 0 | 5.56 |

| Property Taxes | 29 | 0 | 5.00 |

| Unemployment Insurance Taxes | 28 | -2 | 5.11 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

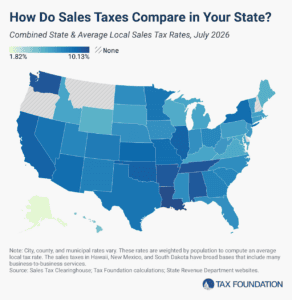

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read