Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readIndiana’s tax code includes all major tax types, but the state has ranked well on the Index since reforms inaugurated in the early 2010s. Indiana has low, single-rate state income taxes and has one of the most efficient property tax systems in the nation, using levy limits to constrain the unlegislated growth of property taxes. However, despite the state’s low, flat 3 percent individual income tax (down from 3.05 percent last year), Indiana allows its counties to impose nonuniform local income tax rates, which range from 0.5 to 3 percent, a factor that negatively impacts the state’s competitiveness.

Indiana’s flat corporate tax rate of 4.9 percent is one of the lowest in the Midwest. Unlike nearby Ohio, Indiana does not impose a harmful gross receipts tax. The state also does not have a throwback rule, offers generous carryforwards for net operating losses, and does not impose a capital stock tax. Implementing permanent full expensing is one element of the corporate income tax code that could further enhance Indiana’s competitiveness.

Indiana is one of the few states that does not allow local governments to impose local option sales taxes. While the state’s sales tax rate of 7 percent is one of the highest in the country, the overall consumption tax burden is only moderately above average given the absence of a local-level tax. The sales tax base in the state is relatively narrow, as most personal consumption services are excluded from the base, while some business inputs are included. Modernizing the sales tax base is a potentially valuable reform for Indiana.

In 2025, Indiana passed legislation tripling the state’s tobacco tax of $0.995 per pack of cigarettes to $2.995 per pack of cigarettes, joining Illinois in imposing the highest tobacco tax in the region.

The state taxes tangible personal property but offers a de minimis exemption of $80,000 to reduce compliance costs for small and medium-sized businesses. Additionally, Indiana does not impose inheritance, estate, or gift taxes.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 10 | -1 | 5.66 |

| Corporate Taxes | 7 | 0 | 5.71 |

| Individual Income Taxes | 20 | -5 | 5.67 |

| Sales Taxes | 14 | 0 | 5.30 |

| Property Taxes | 4 | 0 | 6.25 |

| Unemployment Insurance Taxes | 15 | 0 | 5.47 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

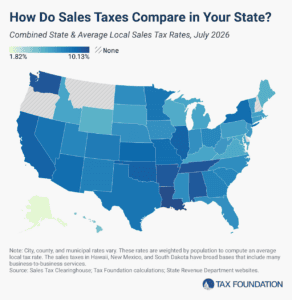

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read