Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readNevada forgoes both individual and corporate income taxes, though it levies a low-rate payroll tax (for purposes other than unemployment insurance) that exclusively taxes wage income, and places a low multi-rate gross receipts tax, the Commerce Tax, on businesses. The Commerce Tax is structurally unsound, as it taxes gross revenue rather than profits, but it is imposed at rates low enough to make the tax’s distortions less damaging.

Nevada’s sales tax is higher than average, as an offset for not levying broad-based income taxes. Its remote seller threshold takes the number of transactions into account, whereas best practice is to adopt a dollar-denominated threshold. The state does not impose a capital stock tax, and, absent income taxes, avoids many of the structural questions faced by other states. However, the state’s unemployment insurance tax regime is relatively uncompetitive.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 20 | -2 | 5.34 |

| Corporate Taxes | 39 | 0 | 4.72 |

| Individual Income Taxes | 8 | -1 | 6.89 |

| Sales Taxes | 41 | 0 | 4.08 |

| Property Taxes | 9 | -1 | 5.90 |

| Unemployment Insurance Taxes | 47 | -2 | 3.76 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

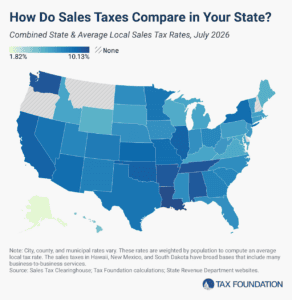

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read