Massachusetts ranks among the bottom 10 states on the Index due to its overly burdensome individual income taxes, property taxes, and UI taxes. In 2022, Massachusetts voters amended the state constitution to impose an additional 4 percent surtax on income greater than $1 million, dismantling the state’s formerly competitive flat income tax and making Massachusetts less attractive for productive households and businesses. The Commonwealth is also an outlier in imposing a separate payroll tax for non-UI purposes.

Additionally, Massachusetts’ so-called corporate excise tax, which has a capital stock base component, imposes high burdens on businesses with large amounts of capital in Massachusetts and includes a throwback rule that exposes Massachusetts’ businesses to high tax burdens when they sell tangible property into states with which they do not have nexus. Furthermore, the state does not offer first-year expensing, discouraging in-state investment. Massachusetts also has an overly burdensome UI tax, with high rates, a solvency tax and surtax, and a lengthy experience rating qualifying period.

In addition to its hefty income tax burdens, especially for businesses, Massachusetts’ property taxes are among the highest in the nation, and the base includes some business inventory, though a levy limit, conventionally called Proposition 2 ½, does help reduce the further growth of property taxes. The state taxes commercial property more heavily than residential property, adding to businesses’ tax burdens. Additionally, Massachusetts levies both an estate tax and a real estate transfer tax.

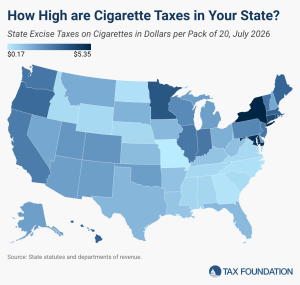

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.