Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readSouth Carolina levies an individual income tax with two brackets, a top marginal rate of 6 percent, and a marriage penalty. By contrast, neighboring North Carolina levies a flat individual income tax and does not impose a marriage penalty, making South Carolina’s levy particularly uncompetitive. Pass-through businesses enjoy a preferential rate on business income, which helps them but creates distortions and drives up the ordinary rate.

The Palmetto State maintains a reasonably competitive corporate tax code, featuring a flat rate of 5 percent. However, the state also relies unusually heavily on tax credits rather than focusing on broad-based rate relief. The state imposes a capital stock tax without capping maximum payments. Capital stock taxes are levied against a business’s net worth (or accumulated wealth) and tend to penalize investment. Moreover, businesses are required to pay capital stock taxes regardless of profitability.

The state also applies a different formula to assess distinct property types, known as split roll taxation, and South Carolina is the only state to apply school property taxes to commercial and industrial property but not to residential property, raising costs for businesses and renters compared to homeowners.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 29 | 0 | 5.08 |

| Corporate Taxes | 8 | 1 | 5.62 |

| Individual Income Taxes | 24 | -1 | 5.43 |

| Sales Taxes | 28 | 1 | 4.63 |

| Property Taxes | 40 | 1 | 4.20 |

| Unemployment Insurance Taxes | 27 | 1 | 5.11 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

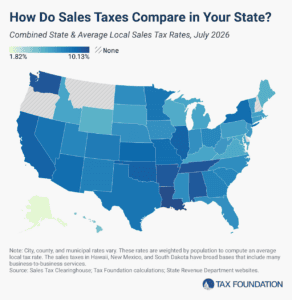

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read