Montana enacted individual income tax cuts in 2021, reducing the top marginal rate from 6.9 percent to 6.75 percent in 2022 and scheduling further reductions, bracket consolidation, and structural reforms for 2024. Initially, the 2021 law compressed the state’s seven individual income tax brackets into two, with rates of 4.7 and 6.5 percent, to be effective in 2024. However, in 2022, lawmakers further reduced the top marginal rate to 5.9 percent effective 2024. While the bottom bracket features an increased rate, conforming to the federal standard deduction in 2025 will help lower-income taxpayers. The individual income tax reforms also removed the marriage penalty by doubling the bracket widths for married filers. The top marginal rate will be reduced to 5.65 percent in 2026 and 5.4 percent in 2027. Additionally, the number of Montanans eligible for the lower bracket has expanded.

Montana’s corporate taxpayers are subject to a single rate of 6.75 percent. Montana does not conform to federal net operating loss deductions and allows carryforwards for 10 years and carrybacks for 3. Montana is also among the minority of states that taxes net CFC-tested income (NCTI), which replaced global intangible low-taxed income (GILTI), with a 20 percent inclusion. The state applies a different formula to assess distinct property types, known as split roll taxation. This leads to higher property tax costs for businesses and for renters, since rental properties with four or more units are classified as commercial property. Montana has a generous de minimis exemption for tangible personal property, eliminating compliance costs for many smaller and mid-sized businesses.

Montana property owners have faced surging property valuations in recent years. In 2025, Montana lawmakers enacted changes to the property tax code. Property owners now face a tiered tax structure with different rates applying depending on the value of the property, effectively shifting the tax burden to other classes of property. Residential property owners are also eligible for a one-time property tax rebate and are automatically eligible for the future homestead exemption.

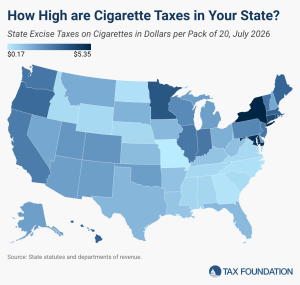

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.