Wyoming‘s tax system ranks 1st overall on the 2025 State Tax Competitiveness Index. Wyoming does not tax individual or corporate income, one of only two states to forgo both taxes (with South Dakota) without imposing a gross receipts tax. However, the state does impose a low-rate capital stock tax on businesses without capping maximum payments. Capital stock taxes are levied on a business’s net worth (or accumulated wealth) and tend to penalize investment. Moreover, businesses are required to pay the capital stock tax regardless of profitability. Wyoming’s tax, notably, is imposed in part to capture revenue from businesses that incorporate in Wyoming for other benefits the state provides.

The four percent statewide sales tax rate is nationally competitive, even after accounting for local sales taxes. The tax base is broad, but includes a disproportionate share of business inputs, which can lead to tax pyramiding and make it more expensive to produce or conduct business in the state. The state’s remote seller threshold takes the number of transactions into account, whereas best practice is to adopt a dollar-denominated threshold. While Wyoming’s overall taxes are quite low, the structure of its tax code results in most taxes being imposed on businesses.

Wyoming is unusual in its ability—at least for now—to rely so heavily on severance taxes and pipeline property taxes, which enables it to forgo taxes imposed in most other states. A state without a corporate or individual income tax definitionally cannot have structural shortcomings in the design of those taxes, hence Wyoming’s performance on the Index. Notably, however, states can also rank well by imposing a wider range of taxes provided they are imposed relatively neutrally, with broad bases and low rates.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).

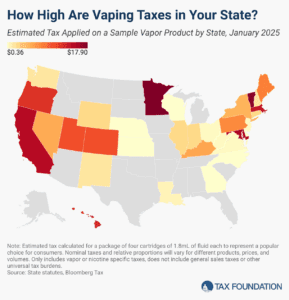

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.

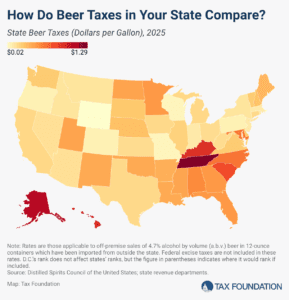

In the United States, taxes are the single most expensive ingredient in beer. The tax burden accounts for more of the final price of beer than labor and materials combined—the many different layers of applicable taxes combining to total as much as 40.8 percent of the retail price.