Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readTexas boasts a regionally and nationally competitive tax code. The state does not impose an individual income tax. However, unlike most others without an individual income tax, Texas (like Washington) applies the corporate gross receipts tax (also known as the “margin tax”) to S corporation and LLC income when others accord them pass-through status.

The margin tax is complex and burdensome. As a modified gross receipts tax, it applies to a firm’s total sales with limited deductions, rather than being imposed on profits.

In 2023, Texas voted to increase the homestead exemption on residential property from $40,000 to $100,000 ($110,000 for the elderly, disabled, and disabled veterans). This exemption is limited to school district property taxes alone, and the state replaces lost education funding with general fund revenue. Instead of shifting the tax burden directly to commercial property and renters like most homestead exemptions, this policy redirects the burden to the state’s general revenue sources, and thus to all taxpayers regardless of home ownership.

Texas treats remote sellers and marketplace facilitators competitively. Unlike most other states that require such sellers to collect and remit sales taxes if either a transaction or dollar threshold is surpassed, Texas only imposes a dollar threshold. Additionally, the dollar threshold is $500,000, greater than most other states, which better aligns the threshold with the size of the state’s economy.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 7 | 0 | 6.10 |

| Corporate Taxes | 46 | 0 | 3.95 |

| Individual Income Taxes | 1 | 0 | 10.00 |

| Sales Taxes | 36 | 1 | 4.26 |

| Property Taxes | 38 | 1 | 4.38 |

| Unemployment Insurance Taxes | 31 | 0 | 4.83 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

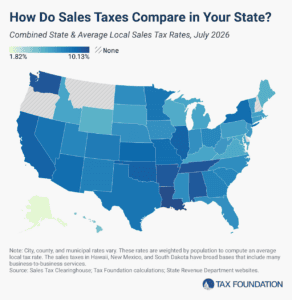

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read