Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readLouisiana’s tax code was a national outlier until the state conducted major tax reform through a special session in November 2024. Previously, the state had multiple individual and corporate income tax brackets that were not indexed for inflation. Now, individual and corporate income is taxed through flat rates of 3 percent and 5.5 percent, respectively. Additionally, the individual standard deduction has been raised to $12,500.

In 2026, the state will eliminate the franchise tax. While not immediate relief, the reform is a positive one as the franchise tax (capital stock tax) is imposed on business net worth (or accumulated wealth), which penalizes investment and is imposed regardless of profitability. The 2024 reforms also ushered in permanent full expensing, making Louisiana the third state to fully decouple from federal phasedowns that existed prior to the One Big Beautiful Bill Act. While the federal provision has been made permanent, only those states that permanently decoupled can guarantee corporate taxpayers stability should the full expensing be restructured or eliminated in the future.

Unlike other states with an individual income tax, Louisiana failed to recognize S corporation status, requiring these entities to file taxes as C corporations rather than the pass-through status accorded to them in other states. This, too, was addressed in the 2024 reform effort and will go into effect in 2026.

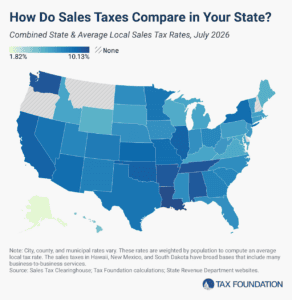

While the reforms of 2024 were a step in the right direction, there is still work to be done. Louisiana maintains one of the most complicated sales tax regimes with the highest combined statewide and average local sales tax rate (10.1 percent) and a lack of centralized sales tax administration. The sales tax code also continues to exempt several services, leaving the base unnecessarily narrow, hindering efforts to lower the rate. The state currently taxes business inventory, which, like the capital stock tax, is imposed regardless of business profitability. These taxes are nonneutral, disproportionately affecting those businesses with larger inventories and causing taxpayers to make inefficient timing and location decisions with their inventory. Voters have the opportunity to repeal this uncompetitive policy in 2026.

Like the state’s individual tax code, the corporate tax rates are not indexed for inflation. However, Louisiana repealed the inefficient throwout rule, which taxes “nowhere income” in the state from which sales are made because the seller lacks sufficient nexus to be taxed in the destination state, leading to taxation in the wrong state at the wrong rate.

Perhaps most notably, Louisiana is highly unusual in lacking central collections and administration of its sales tax. The state has made progress with an alternative remote sellers regime, but parishes’ and other jurisdictions’ ability to define their own tax bases and to administer the taxes separately from the state imposes high compliance costs.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 31 | 6 | 5.06 |

| Corporate Taxes | 10 | 19 | 5.58 |

| Individual Income Taxes | 15 | 17 | 5.84 |

| Sales Taxes | 50 | -2 | 2.93 |

| Property Taxes | 22 | -3 | 5.20 |

| Unemployment Insurance Taxes | 9 | 0 | 5.70 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read