Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readWest Virginia ranks near the middle of the pack on the Index, with some competitive elements and others that could use improvement. The Mountain State recently reduced its individual income tax rates, with a current top rate of 4.82 percent. The legislature has adopted revenue triggers that will continue to phase in rate reductions subject to revenue availability. However, West Virginia has a 6.5 percent corporate income tax rate, which is higher than the national average. In the future, if the state chooses to forgo distortive tax credits for jobs, R&D, and investments, a lower tax rate on all corporate income could be achieved. West Virginia does benefit, however, by conforming to the federal bonus depreciation allowance under Section 168(k) and the federal treatment of net operating losses (NOLs).

West Virginia has a relatively competitive sales tax rate and a low effective property tax rate on owner-occupied housing. However, West Virginia’s taxes on tangible personal property create distortions, especially its harmful taxes on business inventory. Furthermore, West Virginia recently implemented split roll treatment of property, introducing non-neutrality into the tax code by encouraging investment in certain classes of property over others. Under a split roll system, classes of property can be pitted against each other, changing incentives to own or invest in different kinds of property, and allowing local policymakers to ratchet up tax burdens without being seen as raising taxes on homeowners. Some West Virginia localities also impose gross receipts taxes, called Business & Occupation taxes.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 32 | -2 | 5.06 |

| Corporate Taxes | 29 | -2 | 5.15 |

| Individual Income Taxes | 27 | 0 | 5.28 |

| Sales Taxes | 33 | -1 | 4.45 |

| Property Taxes | 19 | 3 | 5.23 |

| Unemployment Insurance Taxes | 24 | -1 | 5.18 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

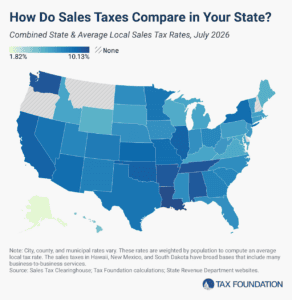

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read