New Mexico‘s tax system ranks 31st overall on the 2025 State Tax Competitiveness Index. New Mexico has a graduated state individual income tax with a top rate of 5.9 percent. Unusually, New Mexico’s corporate tax rate is also graduated, with rates ranging from 4.8 percent to 5.9 percent, and not indexed for inflation.

New Mexico also has a 4.875 percent tax on sales, with an average combined state and local rate of 7.62 percent. As a hybrid between an ordinary sales tax and a gross receipts tax, this tax does not apply to all intermediate transactions like a pure gross receipts tax but does apply to many more business inputs than are included in a typical sales tax, including manufacturing machinery and research and development (R&D) equipment. When this gross receipts-like tax applies to business-to-business transactions, it causes tax pyramiding throughout the supply chain, hampers investment, and negatively affects low-margin businesses.

The state’s corporate income tax also features a throwback rule, which exposes in-state businesses to additional tax when they sell into other states with which they do not have nexus, discouraging some businesses from locating operations in New Mexico. The state conforms to the federal treatment of capital investment under its corporate income tax, but with federal full expensing provisions currently phasing out, New Mexico has an opportunity to make its first-year expensing provisions permanent to avoid the erosion of this pro-investment provision.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).

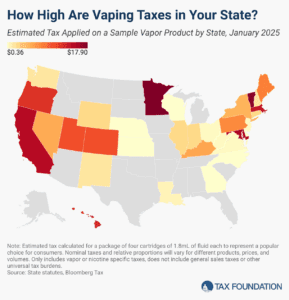

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.

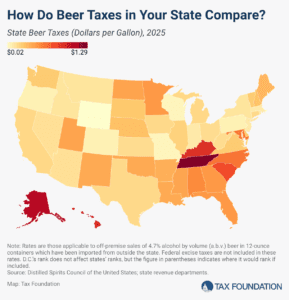

In the United States, taxes are the single most expensive ingredient in beer. The tax burden accounts for more of the final price of beer than labor and materials combined—the many different layers of applicable taxes combining to total as much as 40.8 percent of the retail price.