Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readRhode Island ranks relatively poorly overall due to below-average rankings on all five components. Hurting Rhode Island’s individual income tax component ranking is the sizeable marriage penalty in its individual income tax brackets, with bracket thresholds that are not adjusted for married couples. On the corporate component, Rhode Island taxes net CFC-tested income (NCTI), making it more expensive for corporations to do business in the Ocean State. Furthermore, Rhode Island does not offer bonus depreciation even though it conforms to the federal limitation on business net interest deductibility. However, Rhode Island recently made strides to improve its treatment of business net operating losses (NOLs) by increasing the NOL carryforward period from 5 to 20 years, bringing it more in line with other states.

On the property tax component, Rhode Island benefits from forgoing a capital stock tax and only partially taxing tangible personal property, but the state continues to levy an estate tax, taxes commercial property more heavily than residential property, and collects relatively high property taxes per capita and as a share of owner-occupied housing value.

While Rhode Island’s state sales tax rate is among the highest in the country, its lack of local sales taxes places the combined state and average local sales tax rate near the middle of the pack. Notably, however, Rhode Island has one of the highest tobacco tax rates in the country. Furthermore, despite recent reforms, Rhode Island’s UI tax continues to rank among the least competitive in the country due to high minimum and maximum rates, a wage base that exceeds the federal wage base, a long experience rating qualifying period, and a surtax.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 40 | 0 | 4.69 |

| Corporate Taxes | 32 | 3 | 4.98 |

| Individual Income Taxes | 30 | 0 | 5.12 |

| Sales Taxes | 27 | -1 | 4.65 |

| Property Taxes | 43 | 2 | 4.12 |

| Unemployment Insurance Taxes | 48 | -1 | 3.74 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

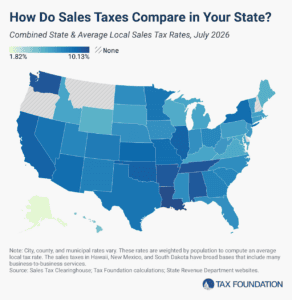

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read