Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readVirginia’s tax code includes all major tax types. The state’s individual income tax has remained stable over the past three decades. However, this stability is not necessarily a positive factor, as many states have implemented significant income tax reforms in recent years, leaving Virginia behind. With four tax brackets that are not adjusted for inflation, the state’s progressive income tax has a top marginal rate higher than several of its neighbors, including Kentucky, North Carolina, Tennessee, and West Virginia. Additionally, Virginia requires individual income tax filing and withholding for nonresidents working even a single day in the state.

While Virginia’s flat corporate income tax rate of 6 percent is around the national average, it is lower than most of Virginia’s neighbors (except North Carolina). The state conforms to the federal treatment of net operating losses, does not have a throwback rule, and does not impose statewide gross receipts or capital stock taxes. However, Virginia allows municipalities to establish local gross receipts taxes and does not permit businesses to claim bonus depreciation, which negatively impacts the state’s tax competitiveness. Implementing permanent full expensing could improve Virginia’s business tax climate.

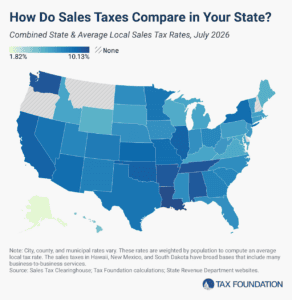

Virginia’s sales tax rate is relatively competitive, though the state could improve by broadening its base to include more consumer services (but not business inputs). In recent years, local and regional sales tax authority has been expanded.

Virginia does not impose estate or inheritance taxes, making it more appealing to wealthy households and retirees. Most of Virginia’s shortcomings are at the local level, with a trio of taxes on business personal property (with no de minimis exemption), business inventory, and business gross receipts. Counties and independent cities are entitled to impose their choice of two of these three taxes.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 30 | -2 | 5.07 |

| Corporate Taxes | 18 | 7 | 5.46 |

| Individual Income Taxes | 36 | 1 | 4.77 |

| Sales Taxes | 13 | 0 | 5.36 |

| Property Taxes | 24 | 0 | 5.15 |

| Unemployment Insurance Taxes | 37 | 1 | 4.57 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read