Mississippi, which ranks near the middle of the pack on the Index, benefits from a low, flat individual income tax rate and a relatively low corporate income tax rate. However, Mississippi’s throwback rule exposes in-state firms to higher Mississippi tax liability when they sell tangible property into states with which they do not have nexus. Additionally, Mississippi maintains a graduated-rate corporate income tax despite moving to a single-rate individual income tax in 2023, a rate that has been reduced to 4.4 percent as of 2025, with the aim to reduce it further to 4 percent by 2026.

While Mississippi’s statewide sales tax rate is among the highest in the country, low reliance on local sales taxes yields a combined state and average local rate that sits near the middle of the pack.

Notably, as part of a series of recent pro-growth reforms, in 2023, Mississippi joined Oklahoma to become the second state in the country to enact permanent full expensing for machinery and equipment investments, thereby increasing the marginal attractiveness of Mississippi for firms that invest in large amounts of capital. Additionally, Mississippi’s capital stock tax is scheduled to phase out by 2028, which will further improve the state’s ability to attract business investment.

While Mississippi’s property taxes are relatively low, its taxation of tangible personal property, including business inventory, as well as intangible property, penalizes in-state investment and hurts the state’s property tax component score.

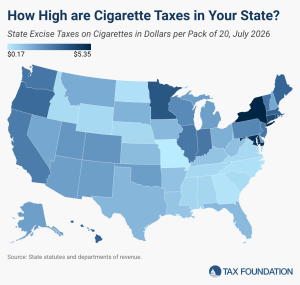

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.