Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readPennsylvania has a low, flat state-level individual income tax rate of 3.07 percent, but local earned income taxes (on a narrower base than the state income tax) dramatically increase overall levels of income taxation in the Commonwealth. Additionally, Pennsylvania maintains an uncompetitive “convenience of the employer rule,” which can lead to double taxation for remote employees working for businesses located in the Commonwealth—ultimately a disincentive for businesses to locate in the state if they want to be able to hire across the country. Pennsylvania also requires individual income tax filing and withholding for nonresidents working even a single day in the state.

Pennsylvania’s corporate income tax rate is unusually high but is slowly phasing down to a competitive 4.99 percent. Pennsylvania is among the very few states to significantly cap net operating loss carryforwards, limiting them to 40 percent of taxable income, but recently enacted legislation will phase this cap up to 80 percent, in 10 percentage point increments, from 2025 through 2029. The Commonwealth does not conform to the Section 168(k) permanent full expensing offered at the federal level, and it also limits Section 179 first-year expensing for pass-through businesses to $25,000 in annual expenses. Pennsylvania also allows localities with existing gross receipts taxes to retain them, though new local gross receipts taxes cannot be created. It is one of five states that still impose an inheritance tax.

Local governments, meanwhile, operate under a patchwork of different state-imposed tax rules, with Philadelphia possessing unique authority given to no other jurisdiction. Consequently, Pennsylvania’s local taxes are among the more complex and burdensome in the country.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 36 | -2 | 4.91 |

| Corporate Taxes | 34 | 4 | 4.90 |

| Individual Income Taxes | 38 | 0 | 4.74 |

| Sales Taxes | 24 | -1 | 4.81 |

| Property Taxes | 13 | -7 | 5.71 |

| Unemployment Insurance Taxes | 34 | 2 | 4.61 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

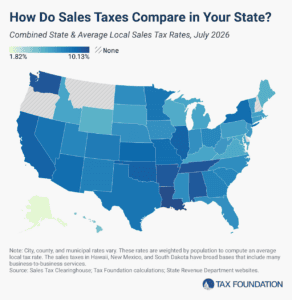

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read