Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readHawaii’s tax code is complex and includes all major tax types, placing the state among the bottom 10 on the Index. Hawaii has one of the most complex, least neutral, and most progressive individual income tax systems in the nation, with 12 tax brackets, a top marginal rate of 11 percent, a very low standard deduction, and, until recently, no adjustment for inflation. It does, however, provide favorable treatment of capital gains income. Conversely, Hawaii caps small business expensing under Section 179 at $25,000, whereas most states allow $1 million.

Hawaii’s corporate income tax is also progressive (which is unusual), with a top rate of 6.4 percent. The state does not index tax brackets for inflation, does not allow full expensing, and has a throwback rule, which exposes Hawaii-based businesses to tax on certain income earned in other states.

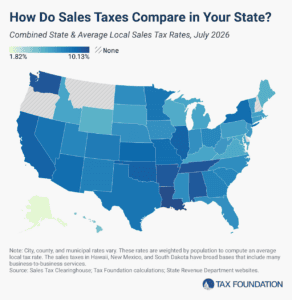

The state’s sales tax, known as the general excise tax (GET), has a relatively low rate of 4 percent but an extremely broad base that includes virtually all business inputs, both goods and services, leading to significant tax pyramiding. Hawaii also allows counties to impose local option sales taxes, generally capped at 0.5 percent.

Hawaii has the highest estate tax rate in the nation at 20 percent, with an exemption of $5.49 million. The state’s property tax system is generally competitive, and particularly features low rates on owner-occupied property, though some counties have split roll property taxes, where commercial properties are taxed more heavily than residential ones. Some counties also impose assessment caps on homestead properties, which are less efficient than levy limits.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 41 | 0 | 4.55 |

| Corporate Taxes | 27 | -1 | 5.29 |

| Individual Income Taxes | 45 | 0 | 3.79 |

| Sales Taxes | 29 | -1 | 4.56 |

| Property Taxes | 15 | 6 | 5.47 |

| Unemployment Insurance Taxes | 43 | 6 | 4.16 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read