Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readIdaho’s individual and corporate income taxes are imposed at a single rate, which was reduced from 5.695 percent to 5.3 percent in 2025. However, the state’s throwback rule is inefficient and taxes “nowhere income” in the state from which sales are made because the seller lacks sufficient nexus to be taxed in the destination state, leading to taxation in the wrong state at the wrong rate—making the corporate income tax more of a disincentive to in-state activity. Idaho also fails to conform to federal provisions to provide first-year expensing of business machinery and equipment purchases. Idaho is also among the minority of states that tax net CFC-tested income (NCTI), which replaced global intangible low-taxed income (GILTI), with a 15 percent inclusion.

Idaho has a generous de minimis exemption for tangible personal property, eliminating compliance costs for many smaller and mid-sized businesses. The state’s income tax has a 30-day withholding threshold but a single-day filing threshold, meaning that an individual who works even one day in the state is expected to file and remit taxes, even though the income would not be withheld by their employer.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 9 | 2 | 5.69 |

| Corporate Taxes | 21 | 2 | 5.40 |

| Individual Income Taxes | 14 | -2 | 5.85 |

| Sales Taxes | 8 | 1 | 5.77 |

| Property Taxes | 3 | 6 | 6.51 |

| Unemployment Insurance Taxes | 36 | -1 | 4.59 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

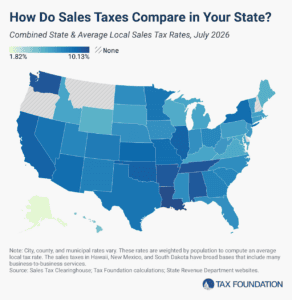

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read