Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readLike other states that forgo one or more major taxes, New Hampshire’s lack of an individual income tax or sales tax yields an extremely competitive overall ranking despite relatively lower rankings on the corporate income tax and property tax components. New Hampshire joined the ranks of the individual income tax-free states when its interest and dividends (I&D) tax was phased out in January 2025, further solidifying the state’s competitive standing.

The Granite State has recently taken steps to improve its corporate income tax structure by decoupling from the federal limitation on the deductibility of business net interest expenses, but New Hampshire has a short net operating loss (NOL) carryforward period of only 10 years, with a $10 million cap. Furthermore, the state does not offer bonus depreciation under Section 168(k), and it limits Section 179 expensing to $500,000. Additionally, New Hampshire has two different business taxes, the business profits tax and the business enterprise tax. The state is also penalized for its lack of conformity to federal schedules for the deductibility of natural resource depletion.

Without an individual income tax or sales tax, New Hampshire relies heavily on property taxes and corporate income taxes, with high rates that affect its scores on those components as a trade-off for its competitiveness compared to states that levy all the major taxes. Moving forward, New Hampshire could improve its competitiveness by adopting permanent full expensing and improving its treatment of NOLs.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 3 | 3 | 7.23 |

| Corporate Taxes | 37 | -5 | 4.83 |

| Individual Income Taxes | 1 | 12 | 10.00 |

| Sales Taxes | 1 | 0 | 8.66 |

| Property Taxes | 44 | -6 | 3.97 |

| Unemployment Insurance Taxes | 23 | 4 | 5.19 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

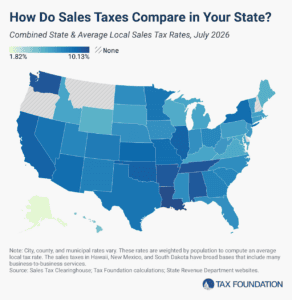

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read