Kansas has a fairly standard tax code—with few features that make it either distinctly competitive or uncompetitive—and this is reflected in the state’s ranking near the middle of the pack. Kansas’ individual and corporate income taxes both have graduated-rate structures, with brackets, a standard deduction, and a personal exemption that are not indexed for inflation. Kansas’ top marginal individual and corporate income tax rates, as well as its combined state and average local sales tax rate, are all at or above the national median.

While Kansas exposes an outsized share of business income to its corporate income tax due to its throwback rule, the state does conform to the federal bonus depreciation allowance and federal net operating loss (NOL) provisions. The Sunflower State maintains a single point of sales tax administration for its state and local sales taxes, and its state and local sales tax bases largely match, with a couple of exceptions. Additionally, most of Kansas’ excise tax rates are relatively competitive compared to those in many other states.

Kansas’ property tax split roll ratio is fairly high, with commercial properties bearing a higher share of the property tax burden compared to residential properties, but by forgoing a capital stock tax and estate or inheritance tax, Kansas outperforms many of its peers on this component.

In 2025, lawmakers enacted legislation using tax triggers to provide individual and corporate income tax relief and, in time, to move to single-rate income taxes. These reforms will improve the state’s performance on the Index.

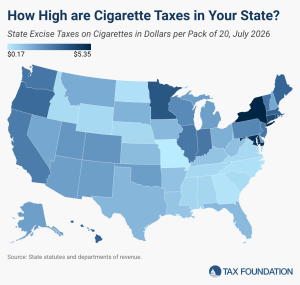

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.