Minnesota‘s tax system ranks 44th overall on the 2025 State Tax Competitiveness Index. Minnesota ranks relatively uncompetitively on the Index and is held back by its graduated state individual income tax with a top rate of 9.85 percent, among the highest in the country. Its taxpayers are also subject to alternative minimum taxes under both the individual and corporate income tax codes, adding complexity to the code. The state also recently created a new surtax on long-term capital gains income, such that the top marginal rate on long-term capital gains income is now higher than the top rate on ordinary income.

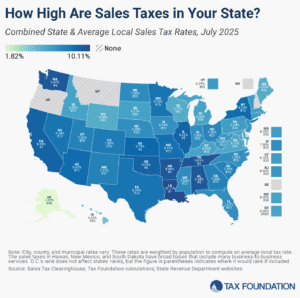

Minnesota also has high sales tax rates, with a 6.875 percent state sales tax rate and an average combined state and local sales tax rate of 8.12 percent. Minnesota’s effective property tax rate on owner-occupied housing value is on the high side, and its split roll system imposes higher taxes on businesses and renters. Minnesota also has a 9.8 percent corporate income tax rate, one of the highest in the country. The state only allows 15 years of net operating loss (NOL) carryforwards, less generous than most states’ rules, which either offer 20-year or unlimited carryforwards. Additionally, Minnesota’s 20 percent first-year expensing allowance is less generous than the federal bonus depreciation allowance under Section 168(k).

Minnesota recently implemented a tax on global intangible low-taxed income (GILTI), which now needs to be added as dividend income by corporations operating within the state. State GILTI taxes are highly uncompetitive, as they have nothing to do with a company’s activities in the state (or even in the US). Minnesota is also in the minority of states to still impose an estate tax on bequeathed property, imposing the tax with a top rate of 16 percent. Among the bright spots in Minnesota’s tax code are its conformity to Section 179 and the fact that the state only partially taxes tangible personal property.

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).