Iowa‘s tax system ranks 20th overall on the 2025 State Tax Competitiveness Index. Iowa’s Index ranking has improved substantially in recent years as the result of several rounds of pro-growth and structurally sound tax reform that have greatly improved the state’s competitive standing. Under recent reforms, Iowa has lowered income tax rates, eliminated an unusual and counterproductive policy of federal deductibility, repealed the alternative minimum tax, and begun the phaseout of the state’s inheritance tax.

While Iowa still has a graduated-rate individual income tax as of July 2024, the state will move to a single-rate structure in 2025, which will further improve the state’s overall score. Unusually, Iowa has a graduated-rate corporate income tax structure but has enacted tax triggers to reduce and flatten the rate over time as revenue becomes available. Iowa is also among the states that allow local income taxes.

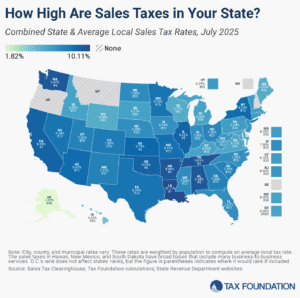

While Iowa’s combined state and average local sales tax rate is slightly below average, the state’s property tax burden is somewhat high, and unlike many of its regional competitors, Iowa not only taxes tangible personal property (machinery and equipment) but does so without providing a de minimis exemption for small businesses. The state also has split roll property taxes, with higher ratios applied to businesses and renters than to homeowners. The state’s inheritance tax will be eliminated in January 2025, which will be reflected in next year’s edition of the Index.

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).