North Dakota performs above average across all tax categories, ranking just outside of the top 10 states overall, as well as on the property tax and corporate tax components. While North Dakota’s corporate and individual income taxes have a graduated-rate structure, both rates are low, with North Dakota’s top marginal individual income tax rate tied with Arizona’s as the lowest in the country (2.5 percent). In May 2025, North Dakota lawmakers limited the growth in local property tax collections by placing a 3 percent cap on annual property tax revenue increases. The same law also raised the homestead property tax credit from $500 to $1,600 and increased the property tax credit for disabled veterans and surviving spouses from $8,100 to $9,000. These property tax changes were made retroactive and are effective for the 2025 tax year.

One shortcoming in North Dakota’s tax code is its throwback rule, which increases tax liability for in-state businesses making sales of tangible personal property in states with which they lack nexus.

However, North Dakota conforms to federal expensing provisions under Sections 168(k) and 179, conforms to the federal treatment of NOLs, and does not levy a capital stock tax, real estate transfer tax, or estate or inheritance tax.

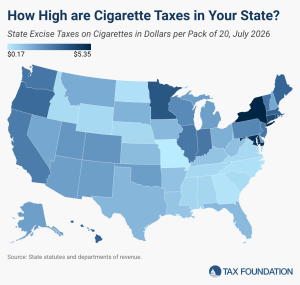

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.