Of the states that levy all the major taxes, North Carolina is among the highest performers on the Index, with its flat 4.25 percent individual income tax rate, low 2.25 percent corporate income tax rate (slated for eventual repeal), and relatively competitive property and sales tax systems. These low rates are made possible in part by North Carolina’s decision to forgo many nonneutral and distortive business tax credits, such as jobs, R&D, and investment tax credits, and for its commitment—secured through a series of reforms in the past decade—to broad bases and low rates.

North Carolina does, however, have room for improvement in its treatment of business net operating losses, as the state allows only 15 years of net operating loss (NOL) carryforwards, whereby past losses can be deducted from current or future profits to ensure the tax falls on average long-run profitability and to avoid subjecting cyclical businesses to a penalty. Additionally, North Carolina’s bonus depreciation allowance is only 15 percent, substantially lower than the federal allowance.

Moving forward, the state could rectify this adverse treatment of investment by adopting permanent full expensing separate from the federal Section 168(k) provision. Furthermore, North Carolina’s Section 179 expensing limit is only $25,000, significantly lower than the $1 million federal allowance. Finally, the largest barrier to the state’s tax competitiveness remains its capital stock tax, called the franchise tax, which is unusually aggressive and taxes businesses on their worth rather than their profits, harming investment and yielding a tax levied without regard to ability to pay.

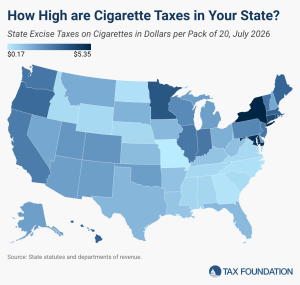

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.