Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readFlorida boasts no individual income tax and a competitive 5.5 percent corporate income tax. Unlike many of its regional competitors, Florida does not tax capital stock, and its corporate income tax largely adheres to national norms, yielding a highly competitive overall tax code. However, the state falls short on its treatment of capital investment, only allowing corporate taxpayers to claim 15 percent of the first-year expensing of machinery and equipment offered under the federal tax code. With full expensing now permanent at the federal level, Florida should consider conforming to this provision of the federal tax code.

Florida’s sales tax rate—despite the lack of an individual income tax—is lower than those levied in many other southern states. Florida’s sales tax base contains a fair amount of exemptions, and in 2025, Florida narrowed its sales tax base even further with new exemptions as well as additional sales tax holidays.

Florida offers a de minimis exemption for tangible personal property, but at $25,000, it is relatively low and offers a possible avenue for improvement. As of the July 1, 2025, snapshot date of this Index, Florida was also the only state to impose a separate commercial lease tax, though the tax was repealed as of October 1. Despite a few outlier provisions, in most regards, the state is among the more competitive in the country.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 5 | -1 | 6.84 |

| Corporate Taxes | 17 | -1 | 5.47 |

| Individual Income Taxes | 1 | 0 | 10.00 |

| Sales Taxes | 16 | 0 | 5.19 |

| Property Taxes | 20 | -5 | 5.22 |

| Unemployment Insurance Taxes | 8 | 2 | 5.72 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

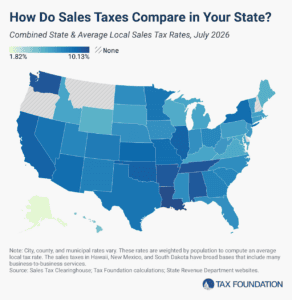

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read