Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readColorado’s individual and corporate income is taxed at a flat rate of 4.4 percent, with the possibility of a reduction to a rate as low as 4.25 percent retroactively, subject to revenues hitting certain targets that are not expected to be hit in 2025. Individual taxpayers are subject to an alternate minimum tax, requiring some to calculate their liability twice—first under ordinary income tax rules and then under the alternate minimum tax—and pay whichever amount is highest.

While the corporate tax code features a single rate, it also contains some inefficiencies. Colorado imposes a throwback rule and taxes “nowhere income” in the state from which sales are made because the seller lacks sufficient nexus to be taxed in the destination state, leading to taxation in the wrong state at the wrong rate. Colorado is also among the minority of states to tax net CFC-tested income (NCTI), formerly global intangible low-taxed income (GILTI).

Of the 45 states that levy a sales tax, Colorado’s statewide rate is the lowest (2.9 percent). Local jurisdictions add an average of 4.96 percent in local sales taxes. Highly unusually, the Centennial State also lacks uniform sales tax administration. While this affects sellers in the state, it particularly impacts remote sellers and marketplace facilitators who may be required to collect and remit sales taxes despite having no physical presence in Colorado. Colorado also lacks local base conformity, with bases varying across jurisdictions.

Effective property taxes are low, though state and local property tax collections per capita remain high. Like much of the country, property owners have seen valuations rise significantly, and lawmakers have worked to provide property tax relief. This, however, is nothing new for Colorado. In 1982, voters approved the Gallagher Amendment, which limited the amount of property tax revenue that could be collected from residential property, shifting ever larger burdens to commercial and industrial property. The remaining 55 percent would come from other property types. In 2020, voters repealed the Gallagher Amendment, eliminating further distortions but reducing future relief for homeowners. Since then, the state has seen several legislative attempts and citizen-led initiatives to provide additional relief. The state’s Taxpayer Bill of Rights (TABOR), though significantly amended over the years, also influences the overall shape of the state’s tax environment.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 33 | -1 | 5.00 |

| Corporate Taxes | 20 | -10 | 5.42 |

| Individual Income Taxes | 21 | -4 | 5.58 |

| Sales Taxes | 39 | -1 | 4.11 |

| Property Taxes | 34 | 1 | 4.75 |

| Unemployment Insurance Taxes | 40 | -1 | 4.31 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

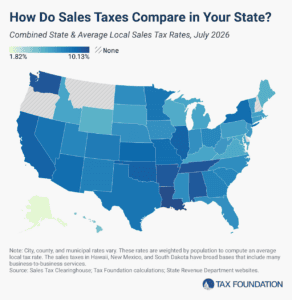

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read