Maine‘s tax system ranks 29th overall on the 2025 State Tax Competitiveness Index. Maine outperforms many of its Northeastern peers but nevertheless performs below average on the Index, with the property tax and corporate income tax being its least competitive tax types.

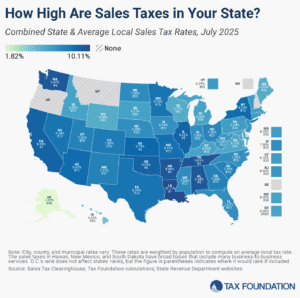

Maine’s property tax structure is among the least competitive in the nation due to high rates, its levying of both an estate tax and a real estate transfer tax, and its taxation of tangible personal property without a de minimis exemption. However, Maine’s high property taxes come as a trade-off for its lack of local sales taxes, which enables the state to maintain one of the lowest combined sales tax rates in the nation, helping it earn a top 10 spot for that component.

On the corporate tax front, Maine includes global intangible low-taxed income (GILTI) in its corporate tax base, and its throwback rule raises the tax burden Maine-based businesses face when they sell tangible property into states with which they do not have nexus. Additionally, Maine’s lack of first-year expensing for C corporations discourages in-state investment, although its conformity to the Section 179 expensing allowance makes its treatment of small business investments more competitive than some of its peers.

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

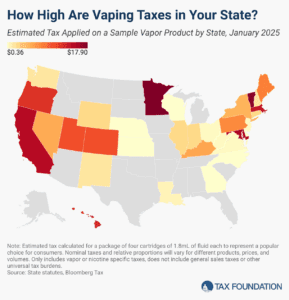

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.