Colorado‘s tax system ranks 32nd overall on the 2025 State Tax Competitiveness Index. Colorado’s individual and corporate income is taxed at a flat rate of 4.25 percent. Individual taxpayers are subject to an alternate minimum tax, requiring some to calculate their liability twice—first under ordinary income tax rules and then under the alternate minimum tax—and pay whichever amount is highest.

While the corporate tax code features a single rate, it also contains some inefficiencies. Colorado imposes a throwback rule and taxes “nowhere income” in the state from which sales are made because the seller lacks sufficient nexus to be taxed in the destination state, leading to taxation in the wrong state at the wrong rate. Colorado is also among the minority of states to tax global intangible low-taxed income (GILTI).

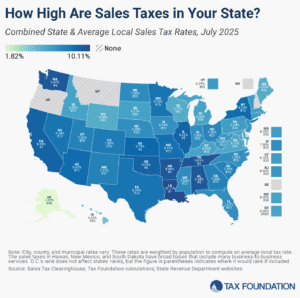

Of the 45 states that levy a sales tax, Colorado’s statewide rate is the lowest (2.77 percent). Local jurisdictions add an average of 4.91 percent in local sales taxes. Highly unusually, the Centennial State also lacks uniform sales tax administration. While this affects sellers in the state, it particularly impacts remote sellers and marketplace facilitators who may be required to collect and remit sales taxes despite having no physical presence in Colorado. Colorado also lacks local base conformity, with bases varying across jurisdictions.

Effective property taxes are low, though state and local property tax collections per capita remain high. Like much of the country, property owners have seen valuations rise significantly, and lawmakers have worked to provide property tax relief. This, however, is nothing new for Colorado. In 1982, voters approved the Gallagher Amendment, which limited the amount of property tax revenue that could be collected from residential property to 45 percent of the state’s total. The remaining 55 percent would come from other property types. In 2022, voters repealed the Gallagher Amendment, paving the way for significantly increased property tax liability for homeowners. Since then, the state has seen several legislative attempts and citizen-led initiatives to provide relief. The state’s Taxpayer’s Bill of Rights (TABOR), though significantly amended over the years, also influences the overall shape of the state’s tax environment.

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).