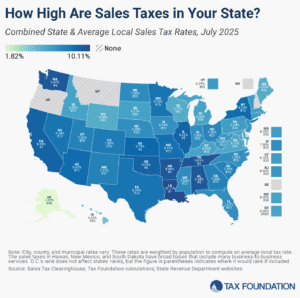

Alaska‘s tax system ranks 3rd overall on the 2025 State Tax Competitiveness Index. Alaska, which forgoes an individual income tax and a state-level sales tax, ranks well on the Index due to the absence of major taxes, but has room to reform the taxes it does impose. Cities and boroughs can impose their own sales taxes, resulting in a lack of base uniformity, though local governments have agreed to adopt a uniform code with central administration for remote sellers, lessening compliance burdens.

The state’s corporate income tax has a 20 percent global intangible low-taxed income (GILTI) inclusion, making it a national outlier. Alaska also imposes a throwback rule, exposing some out-of-state activity of Alaska-based corporations to the state’s corporate taxes, and it only partially conforms to federal depletion allowances. Property taxes are somewhat high, and the state taxes some inventory, but with no individual income tax, state sales tax, capital stock tax, or inheritance or estate tax, Alaska keeps taxes low for most residents and for some businesses, particularly those not subject to production taxes (e.g., oil and natural gas).

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

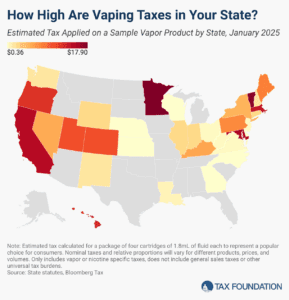

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.