Wyoming does not tax individual or corporate income, one of only two states to forgo both taxes (with South Dakota) without imposing a gross receipts tax. However, the state does impose a low-rate capital stock tax on businesses without capping maximum payments. Capital stock taxes are levied on a business’s net worth (or accumulated wealth) and tend to penalize investment. Moreover, businesses are required to pay the capital stock tax regardless of profitability. Wyoming’s tax, notably, is imposed in part to capture revenue from businesses that incorporate in Wyoming for other benefits the state provides.

The four percent statewide sales tax rate is nationally competitive, even after accounting for local sales taxes. The tax base is broad, but includes a disproportionate share of business inputs, which can lead to tax pyramiding and make it more expensive to produce or conduct business in the state. While Wyoming’s overall taxes are quite low, the structure of its tax code results in most taxes being imposed on businesses.

Wyoming is unusual in its ability—at least for now—to rely so heavily on severance taxes and pipeline property taxes, which enables it to forgo taxes imposed in most other states. A state without a corporate or individual income tax definitionally cannot have structural shortcomings in the design of those taxes, hence Wyoming’s performance on the Index. Notably, however, states can also rank well by imposing a wider range of taxes, provided they are imposed relatively neutrally, with broad bases and low rates.

Wyoming property owners have faced surging property valuations in recent years. In 2024, voters authorized the legislature to create a specific residential property tax class, further splitting the roll. In 2025, the legislature enacted a 25 percent exemption on the first $1 million of the value of a single-family residential home and its improved land. This only applies to primary residences inhabited for at least eight months of the year, with exceptions for active-duty military personnel. Similarly, seniors have separate property tax exemptions.

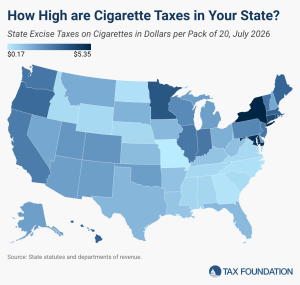

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.