Washington‘s tax system ranks 45th overall on the 2025 State Tax Competitiveness Index. Washington forgoes an individual income tax on wage income due to constitutional constraints, though the state recently imposed a tax on high earners’ capital gains income, a policy that raised constitutional questions but ultimately secured the assent of the state supreme court. The constitution has been similarly interpreted as blocking a corporate income tax, but Washington instead imposes a high multiple-rate gross receipts tax, called the Business & Occupation Tax. Because it is based on gross revenues rather than net income (profits), it yields very high rates of taxation on low-margin businesses and leads to tax pyramiding, where goods and services have the tax embedded several times over, imposed on each transaction within the production process.

The state’s sales tax, imposed atop the gross receipts tax, is not just a high rate but is also imposed on a base that includes an unusual share of business inputs, particularly in the digital products space. Washington also levies a progressive real estate transfer tax and the nation’s highest-rate estate tax. High UI taxes and an uncompetitive UI tax structure also contribute to the state’s poor Index ranking despite the state forgoing an individual income tax, which might otherwise be expected to yield a much more competitive tax environment.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).

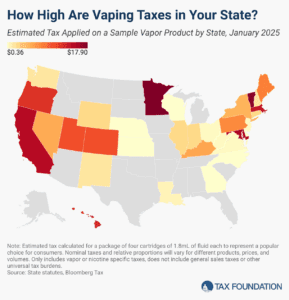

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.

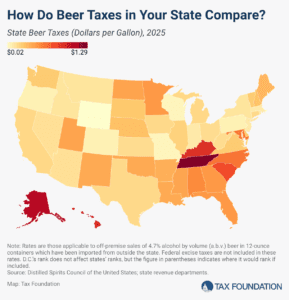

In the United States, taxes are the single most expensive ingredient in beer. The tax burden accounts for more of the final price of beer than labor and materials combined—the many different layers of applicable taxes combining to total as much as 40.8 percent of the retail price.