Oregon forgoes a sales tax but doubles down on other forms of taxation. The state has a complex and progressive individual income tax system with four tax brackets, a top marginal rate of 9.9 percent, and a personal exemption structured as a tax credit. Additionally, the tax brackets are not adjusted for inflation. Portland has the highest combined local income tax rate in the nation (4 percent), adding an extra layer of tax burden for residents of the state’s largest city.

The absence of a sales tax in Oregon is offset by an overly complex corporate tax system, which includes a 7.6 percent corporate income tax, a 0.57 percent gross receipts tax (the Corporate Activity Tax), and additional corporate taxes at the local level, particularly in the Portland area. Although gross receipts taxes typically do not allow any deductions from gross sales, the CAT provides a 35 percent deduction for either labor costs or the cost of goods sold. However, this does not significantly improve Oregon’s competitiveness in attracting businesses, as the state’s corporate tax system ranks among the worst in the nation, comparable to Delaware, the only other state to combine corporate income and gross receipts taxes.

Oregon’s property tax system is moderately competitive, though the property tax burden relative to personal income is higher than in California and Washington. Additionally, the state imposes an estate tax with a maximum rate of 16 percent and the lowest estate tax exemption among states that levy the tax ($1 million), which further reduces the state’s competitiveness for high-net-worth individuals.

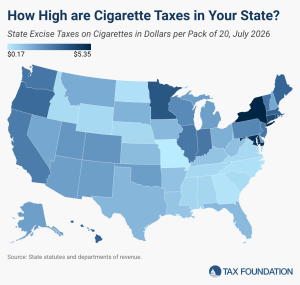

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.