North Carolina‘s tax system ranks 12th overall on the 2025 State Tax Competitiveness Index. Of the states that levy all the major taxes, North Carolina is among the highest performers on the Index, with its flat 4.5 percent individual income tax rate, low 2.5 percent corporate income tax rate (slated for eventual repeal), and relatively competitive property and sales tax systems. These low rates are made possible in part by North Carolina’s decision to forgo many nonneutral and distortive business tax credits, such as jobs, R&D, and investment tax credits, and for its commitment—secured through a series of reforms in the past decade—to broad bases and low rates.

North Carolina does, however, have room for improvement in its treatment of business net operating losses, as the state allows only 15 years of net operating loss (NOL) carryforwards, whereby past losses can be deducted from current or future profits to ensure the tax falls on average long-run profitability and to avoid subjecting cyclical businesses to a penalty. Additionally, North Carolina’s bonus depreciation allowance is only 15 percent, substantially lower than the federal allowance. Moving forward, the state could rectify this adverse treatment of investment by adopting permanent full expensing separate from the federal Section 168(k) provision. Furthermore, North Carolina’s Section 179 expensing limit is only $25,000, significantly lower than the $1 million federal allowance. Finally, the largest barrier to the state’s tax competitiveness remains its capital stock tax, called the franchise tax, which is unusually aggressive and taxes businesses on their worth rather than their profits, harming investment and yielding a tax levied without regard to ability to pay.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).

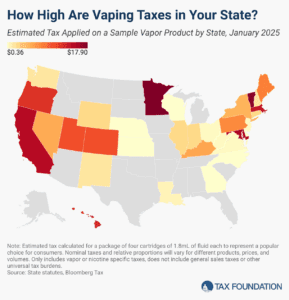

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.

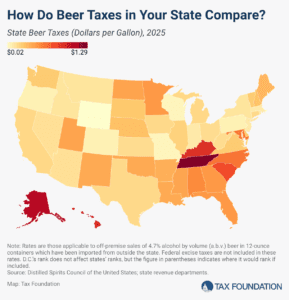

In the United States, taxes are the single most expensive ingredient in beer. The tax burden accounts for more of the final price of beer than labor and materials combined—the many different layers of applicable taxes combining to total as much as 40.8 percent of the retail price.