Massachusetts‘s tax system ranks 41st overall on the 2025 State Tax Competitiveness Index. Massachusetts ranks among the bottom 10 states on the Index due to its overly burdensome individual income taxes, property taxes, and UI taxes. In 2022, Massachusetts voters amended the state constitution to impose an additional 4 percent surtax on income greater than $1 million, dismantling the state’s formerly competitive flat income tax and making Massachusetts less attractive for productive households and businesses. The Commonwealth is also an outlier in imposing a separate payroll tax for non-UI purposes.

Additionally, Massachusetts’ so-called corporate excise tax, which has a capital stock base component, imposes high burdens on businesses with large amounts of capital in Massachusetts and includes a throwback rule that exposes Massachusetts’ businesses to high tax burdens when they sell tangible property into states with which they do not have nexus. Furthermore, the state does not offer first-year expensing, discouraging in-state investment. Massachusetts also has an overly burdensome UI tax, with high rates, a solvency tax and surtax, and a lengthy experience rating qualifying period.

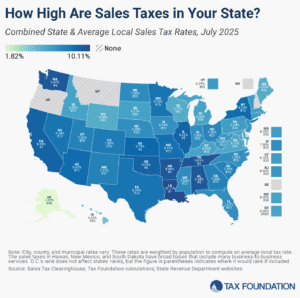

In addition to its hefty income tax burdens, especially for businesses, Massachusetts’ property taxes are among the highest in the nation, and the base includes some business inventory, though a levy limit, conventionally called Proposition 2 ½, does help reduce the further growth of property taxes. Additionally, Massachusetts levies both an estate tax and a real estate transfer tax. One notable bright spot, however, is Massachusetts’ neutral treatment of different classes of property, avoiding the split roll systems common in states that impose excessive burdens on commercial properties compared to residential properties.

The One Big Beautiful Bill’s changes to the taxation of international income have surprising implications for state codes, yielding tax increases and a revised tax base that, through quirks of state incorporation, bears very little resemblance to the federal base and almost nothing of its purpose.

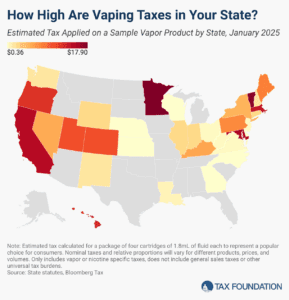

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.