Maine outperforms many of its Northeastern peers but nevertheless performs below average on the Index, with the property tax and corporate income tax being its least competitive tax types.

Maine’s property tax structure is among the least competitive in the nation due to high rates, its levying of both an estate tax and a real estate transfer tax, and its taxation of tangible personal property without a de minimis exemption. However, Maine’s high property taxes come as a trade-off for its lack of local sales taxes, which enables the state to maintain one of the lowest combined sales tax rates in the nation.

Maine includes global intangible low-taxed income (GILTI) in its corporate tax base, which will transition to a tax on net CFC-tested income (NCTI) when the state updates its conformity statute. Maine’s throwback rule raises the tax burden Maine-based businesses face when they sell tangible property into states with which they do not have nexus. Additionally, Maine’s lack of first-year expensing for C corporations discourages in-state investment, although its conformity to the Section 179 expensing allowance makes its treatment of small business investments more competitive than some of its peers.

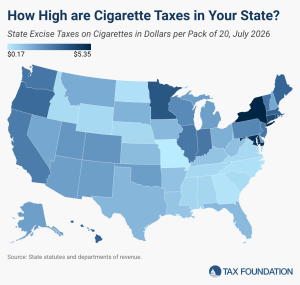

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.