On July 4, 2025, the One Big Beautiful Bill Act (OBBBA) was signed into law by President Trump, capping off the final step of the budget reconciliation process for the 2025 fiscal year.

While the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. law is expected to grow the US economy by making pro-growth policies like 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs. and research and development (R&D) expensing permanent, it misses an opportunity to address the growing deficit and focuses too heavily on political carveouts like the “no tax on” exemptions that further complicate the tax code.

We estimate the tax law will increase long-run GDP by 1.2 percent and increase the deficit by $3 trillion over the next decade when factoring in spending cuts and economic growth.

As America’s leading nonpartisan educational tax policy nonprofit, the Tax Foundation continues to educate lawmakers, journalists, and taxpayers on how this recent tax legislation may affect them and how policymakers can better improve the tax code. Below is a quick FAQ tax guide for the OBBBA.

The Basics

Congress passed the One Big Beautiful Bill Act (OBBBA) as part of the budget reconciliation process for fiscal year 2025, which permitted the Senate to pass the law via a simple majority.

In addition to spending changes related to health programs, homeland security, and defense, OBBBA addressed the looming expiration of the 2017 Tax Cuts and Jobs Act (TCJA) tax cuts at the end of 2025 by making those tax changes permanent.

The law also enacted many of President Trump’s campaign proposals to exempt certain types of income from tax (e.g., tips and overtime), and Congress made additional tax changes to international tax policy.

The OBBBA improved tax policy by making pro-growth tax provisions like full expensing permanent and by providing certainty to taxpayers through the extension of expiring TCJA measures. However, the law also worsened the tax code by increasing complexity and narrowing the tax base.

The TCJA reduced taxes for most individuals and businesses in 2017, but most of the individual tax changes were scheduled to expire at the end of 2025. These expirations would have increased tax burdens on about 62 percent of tax filers, and policymakers were motivated to avoid this tax increase by making the individual tax changes from the TCJA permanent.

The OBBBA makes the 2017 tax changes permanent, including the larger standard deduction, more generous child tax credit (CTC), lower ordinary tax rates, and tighter limitations to certain itemized deductions such as the deduction for home mortgage interest (HMID). Permanence for TCJA-related individual provisions makes up most of the value of the tax cuts in the OBBBA.

Permanence for the expiring TCJA provisions was one of the strong points of the OBBBA, avoiding a large tax increase and providing added certainty for individuals and businesses regarding the long-term structure of the tax code.

In addition to permanence for the 2017 tax cuts, the individual provisions of the law expand the standard deduction and child tax credit incrementally, temporarily provide a more generous deduction for state and local taxes (SALT) paid, create a new haircut for itemized deductions and limits for itemized charitable deductions, and create new temporary income tax deductions for tips, overtime income, seniors, and auto loans (all subject to income limits).

The more generous estate tax exemption from the TCJA (worth just over $14 million in 2024) is made permanent and increased to $15 million per decedent in 2026, reducing the number of estates subject to the estate tax.

For businesses, the law makes full expensing for short-lived and domestic R&D investment permanent and creates a new temporary 100 percent deduction for certain structures involved in tangible production. Tax credits associated with green energy production are phased out over the next few years, and scheduled international tax rate hikes were canceled along with other structural changes to international tax rules.

The law also made a series of smaller changes to the tax code, including a new set of tax-deferred savings accounts, changes to rules related to the child tax credit and earned income tax credit, a redesign to the excise tax on university endowment income, and a new 1 percent tax on remittances.

The OBBBA provides a mix of permanent and temporary policies for taxpayers to wade through. The TCJA’s expiring individual provisions and business items like 100 percent bonus depreciation, domestic R&D expensing, and a more generous interest limitation are made permanent. The expansions to the standard deduction and child tax credit, and alterations to the alternative minimum tax (AMT) are also permanent.

The new income tax deductions for overtime, tips, seniors, and auto loans are temporarily in effect from 2025 through 2028. The $40,000 SALT deduction limit reverts to $10,000 in 2030, and the new 100 percent deduction for business investment in certain structures expires for structures with construction beginning after December 31, 2028, or placed in service after December 31, 2030.

Permanency for the expiring 2017 tax provisions and for full expensing of domestic R&D and short-lived investments improved taxpayer certainty and the long-run growth potential of the law by improving incentives to work and invest.

However, the temporary tax cuts hide the full long-term fiscal cost of the law and create uncertainty for taxpayers benefiting from those tax deductions. Ideally, policymakers should strive for permanency (or allow unprincipled items to fully expire) in future tax policy debates.

We produced analysis on the revenue, economic, and distributional impacts of the OBBBA using the Tax Foundation Taxes and Growth Model to quantify the benefits, costs, and trade-offs of the law for taxpayers and the US economy.

Our analysis of the good, the bad, and the ugly of the OBBBA provides a summary of the law’s strengths and weaknesses from the perspective of sound tax policy.

Our budget reconciliation tax tracker compares the law with earlier versions of OBBBA as it made its way through the legislative process along with estimates associated with President Trump’s campaign proposals and TCJA permanence.

On The Deduction podcast, we cover the details of the OBBBA and what it means for tax policy debates in the coming years.

For Individuals

The OBBBA permanently preserves the lower ordinary income tax rates and adjusted bracket widths from the TCJA and provides a minor inflation adjustment for income subject to the 10 and 12 percent brackets, which cuts taxes slightly for income in these brackets. The top tax rate will remain at 37 percent next year, down from a scheduled increase to 39.6 percent absent this policy change.

The standard deduction is worth $15,000 for single filers and $30,000 for joint filers in 2025 and was scheduled to be cut in half next year. The OBBBA preserves the more generous standard deduction and increases it slightly to $15,750 for single filers and $31,500 for joint filers in 2025, indexed to inflation annually moving forward.

The more generous standard deduction improves tax simplicity by reducing the number of taxpayers who benefit from itemizing over taking the standard deduction. According to our estimates, about 14.2 percent of taxpayers will itemize in 2026 under the OBBBA, compared to about 32 percent itemizing that year if no action was taken on tax policy and the TCJA provisions expired.

The personal exemption provided a set deduction worth $4,050 per filer and dependent in 2017. The exemption was suspended as part of the 2017 tax law starting in 2018 and was scheduled to return at the end of 2025. The OBBBA makes permanent the suspension of the personal exemption.

The suspended personal exemption approximately offsets the tax value of the expanded standard deduction and child tax credit (CTC). This broad swap also simplified tax filing for most taxpayers by reducing the number of itemizers.

In 2017, the TCJA increased the exemption amount for the alternative minimum tax (AMT), reducing the number of taxpayers subject to the AMT. The exemption was raised from $54,300 for single filers and $84,500 for joint filers in 2017 to $70,300 for single filers and $109,400 for joint filers in 2018, adjusted for inflation thereafter.

Similarly, the TCJA increased the thresholds at which the AMT exemption begins to phase out, raising it from $120,700 for single filers and $160,900 for joint filers to $500,000 for single filers and $1 million for joint filers, adjusted for inflation each year. Both the higher exemption and phaseout thresholds were scheduled to expire at the end of 2025, increasing the number of filers subject to the AMT in 2026.

The OBBBA preserves the higher exemption amount and phaseout thresholds while adjusting the inflation indexing slightly for the phaseout thresholds. In 2026, the phaseout thresholds will be reset to the 2018 values of $500,000 for single filers and $1 million for joint returns, adjusted for inflation moving forward.

The AMT exemption phaseout rate was also increased from 25 percent under prior law to 50 percent from 2026 onward, meaning the exemption is reduced twice as fast once income exceeds the threshold.

Preserving the higher AMT exemption and phaseout threshold amounts reduced complexity by subjecting fewer filers to the AMT. Policymakers should consider further reductions in the scope of the AMT, ideally repealing it to simplify the tax system.

The OBBBA makes permanent the TCJA’s expanded child tax credit (CTC) per qualifying child, with some adjustments. The CTC was scheduled to revert to its smaller level worth up to $1,000 in 2026 prior to OBBBA, down from $2,000 in 2025. The law increases the maximum CTC amount to $2,200 in 2025 and adjusts the value of the credit for inflation moving forward, while tightening eligibility rules. Other family-related changes include a modest increase to the child and dependent care tax credit.

Permanency for the expanded CTC improves the predictability of the tax code for families with children, but falls short of full reform to simplify refundable credits in the tax code.

The OBBBA extends and makes permanent the Section 199A pass-through deduction, which allows pass-through business owners to deduct 20 percent of qualified business income when calculating taxable income. The law also provides a $400 minimum deduction amount for taxpayers with $1,000 or more of active qualified business income.

The law provides stability for pass-through businesses, and 199A permanency contributes to OBBA’s pro-growth impact, but it misses an opportunity to simplify the tax treatment of pass-through businesses.

The law temporarily provides a more generous deduction cap for state and local taxes (SALT), increasing the cap from $10,000 to $40,000 from 2025 to 2029. The more generous SALT deduction cap is paired with an income limit starting at $500,000, which phases out the more generous deduction back down to $10,000 for taxpayers with incomes over $600,000. The deduction value and the income limit will increase by 1 percent each year through 2029.

Starting in 2030, the SALT deduction cap will revert to its prior law value of $10,000 for all filers ($5,000 for those married filing separately) permanently. The $10,000 SALT cap helps offset part of the other tax cuts in the law while also limiting the regressive impact of a more generous SALT deduction cap on the distribution of taxes paid.

The OBBBA also makes permanent other changes to itemized deductions made by the TCJA, such as the tighter limit on home mortgage interest deductions and miscellaneous itemized deductions. The law also introduces a new limitation on itemized deductions, limiting the value of the deductions to 35 cents on the dollar for filers in the top bracket.

Social Security benefits are treated identically under the OBBBA as under prior law, which means they are partially subject to income tax on up to 85 percent of benefits, depending on a taxpayer’s income.

However, the OBBBA provides a new $6,000 deduction for taxpayers age 65 and older per qualifying taxpayer, which phases out at a 6 percent rate when one’s income exceeds $75,000 for single filers and $150,000 for joint filers. The deduction is fully phased out at $175,000 for single filers and $250,000 for joint filers. The deduction is provided for all sources of income, including Social Security benefits, and will be available to both itemizers and non-itemizers.

The new senior deduction with the phaseout delivers a larger tax cut to lower-middle- and middle-income taxpayers compared to the original campaign promise of exempting all Social Security benefits from income taxation. But given the temporary nature of the policy, it will increase the deficit impact of the law without boosting long-run economic growth.

There are two major permanent changes to individual charitable deductions under the OBBBA: a new 0.5 percent of income floor for charitable giving before taxpayers can claim an itemized deduction for charitable giving, and a new charitable deduction worth $1,000 ($2,000 for joint filers) available to itemizers and non-itemizers alike.

The 0.5 percent income floor requires itemizers to omit the first 0.5 percent of income worth of charitable giving before the itemizer can deduct further charitable giving in the calculation of their taxable income, reducing the value of the itemized charitable deduction.

The new $1,000 charitable deduction will be available to taxpayers without regard to whether they itemize or take the standard deduction, which makes the deduction available to a much larger group of taxpayers, as only about 14 percent of taxpayers are projected to itemize under the OBBBA according to Tax Foundation estimates.

These two changes are of roughly similar size in terms of revenue effects but would change the tax incentives for charitable giving for taxpayers. The new deduction for non-itemizers narrows the tax base, and ideally the charitable deduction would be limited and tax rates lowered as part of a broader reform of the tax code.

The OBBBA created new savings accounts for children, allowing parents and others to contribute up to a combined $5,000 yearly (adjusted for inflation starting in 2027) for the child to use after turning 18 years old. The accounts include a $1,000 deposit made by the federal government for certain children born in 2025 through 2028, and employers are also allowed to contribute up to $2,500 tax-free to employee accounts.

The account grows tax-deferred until account owners make withdrawals, which can only start at age 18, and the account at that point essentially follows the rules in place for individual retirement accounts (IRAs). As such, withdrawals, net of after-tax contributions, made before age 59 ½ are subject to regular income tax and a 10 percent penalty, with many exceptions, including for college tuition (unlimited) and for a first-time home purchase (up to $10,000).

Due to the complex rules and limited tax benefits, Trump Accounts are unlikely to be widely used for saving. If the federal government really wanted to make saving more accessible for taxpayers, it would replace the complicated mess of savings accounts currently available with universal savings accounts.

Starting in 2026, the federal estate tax exemption was scheduled to fall by about 50 percent, from $14 million in 2025 to $7.1 million in 2026, increasing the share of estates subject to the estate tax. The OBBBA extends and makes permanent the expanded exemption amount and increases it to $15 million per decedent, indexed for inflation annually.

A permanent expanded estate tax exemption reduces the complications associated with the tax for most households, but ideally policymakers will take the final step and repeal the estate tax entirely in future reform efforts.

The OBBBA creates a new temporary deduction for tips when calculating taxable income worth up to $25,000 in tips, available to itemizers and non-itemizers. The deduction is in effect from 2025 through 2028 and phases out at a 10 percent rate when adjusted gross income exceeds $150,000 ($300,000 for joint filers). Tips qualifying for the income tax deduction will still be subject to tax reporting and payroll taxes.

Only 2.5 percent of the workforce works in tipped occupations, and only 5 percent of workers in the bottom 25 percent of earners do. As such, the policy would leave the vast majority of low- and middle-income earners out of the loop. The new deduction may increase complexity and require safeguards in regulation to prevent reclassification of income from wages to tips to take the deduction.

Up to $12,500 in overtime compensation is deductible when calculating taxable income under the OBBBA temporarily from 2025 through 2028, phasing out in value at a 10 percent rate when adjusted gross income exceeds $150,000 ($300,000 for joint filers).

Only employees who are not exempt from Fair Labor Standards Act (FLSA) overtime rules are eligible, and only the 0.5 “premium” portion of a time and a half is eligible for the deduction and will be available to both itemizers and non-itemizers.

Exempting overtime is a more complicated proposal than the deductions for tips and Social Security, which are both already subject to some tax reporting requirements. Instead, exempting a portion of wage income, based on hours worked, introduces an entirely new distinction in the tax code, requiring additional information reporting of hours, likely from employers and employees, as well as new administrative checks.

Interest paid on a financed new automobile will be deductible for amounts up to $10,000 from 2025 through 2028, phasing out at a 20 percent rate when income exceeds $100,000 for single filers and $200,000 for joint filers. The automobile must have been finally assembled in the United States to qualify for the deduction.

The auto loan interest deduction will be available to itemizers and non-itemizers alike. It is likely that dealerships will need to help taxpayers confirm that an automobile qualifies for the deduction based on the location of final assembly.

The OBBBA will increase after-tax incomes for taxpayers across all income levels in 2026 by an average of 2.9 percent. However, tax refunds are the difference between taxes remitted during the tax year and final tax liability owed during tax season.

Changes in tax refunds are not necessarily indicative of the change in a taxpayer’s liability, as withholding may also change over time. Regardless of whether an individual over-withholds or under-withholds, receiving a tax refund or owing the IRS come tax time does not tell you how much you paid in taxes and is not the best way to evaluate your income tax burden.

For Businesses

The OBBBA restores and makes permanent 100 percent bonus depreciation for short-lived asset investment, which allows businesses to fully and immediately deduct the cost of many investments when calculating taxable income. The TCJA temporarily provided 100 percent bonus depreciation through 2022, at which point the bonus amount began falling by 20 percentage points each year until it phased out entirely at the end of 2026.

The permanent restoration of 100 percent bonus depreciation is a big improvement for the tax code because it removes penalties for investment associated with delayed depreciation deductions, creating certainty and a degree of simplification for taxpayers, and preserving the large pro-growth benefit of bonus depreciation over the long term.

Historically, research and development (R&D) investment has been immediately deductible from taxable income. However, starting in 2022, these investments were required to be amortized over five years for domestic investment and 15 years for foreign R&D investment as part of the TCJA tax changes.

The OBBBA restores full and immediate deductibility of R&D expenses for domestic R&D, leaving in place the 15-year amortization for foreign R&D. The law also provides some retroactive R&D expensing for R&D investments made between 2021 and 2025 for certain firms or, as an alternative option, allows those investments to be deducted over one or two years.

Permanent R&D expensing removes the tax penalty on R&D investment in the US, creating certainty and stability in the tax code and providing a pro-growth boost to the US economy. Ideally, foreign R&D investment would also be expensed given the synergies that often exist between domestic and foreign R&D activity.

The OBBBA created a new, temporary 100 percent deduction for investment in certain structures associated with tangible production of goods in the US. For qualifying structures beginning construction after January 19, 2025, and before January 1, 2029, and placed in service before January 1, 2031, 100 percent of the value of that investment can be deducted from taxable income.

This provision improves the cost recovery for structures that usually have long depreciation lives, often up to 39 years to fully recapture the cost of the investment under current law. The new deduction for certain structures should boost investment while the provision is in place. The provision will require clear guidance from the IRS and Treasury Department on qualifying structures to ensure the benefit is targeted consistent with the intent of the law.

Ideally, a simple adjustment to the value of depreciation deductions for structures or full expensing for all structures would become a permanent component of tax law in future reforms.

The TCJA put into place a new limit on the amount of interest deductible from business tax returns for firms that engage in debt-financed investment. The limit was set at interest worth up to 30 percent of earnings before interest, taxes, depreciation, and amortization (EBITDA) from 2018 through 2021.

Starting in 2022, this interest limit was tightened to 30 percent of earnings before interest and taxes (EBIT), excluding the value of depreciation and amortization from the calculation and mechanically lowering the amount of interest deductible.

The OBBBA permanently reverses this tightening of the interest limitation, restoring the EBITDA-based limitation at 30 percent. The EBITDA-based limit is more common internationally and provides some tax relief for firms dealing with debt-financed investment in a higher interest rate environment.

One of the largest areas of reform in OBBBA is the repeal or early phaseout of many of the Inflation Reduction Act’s (IRA) green energy tax credits. These changes raise about $500 billion over a decade, reducing the cost of the green energy credits by about half. Several IRA credits—like those for electric vehicles (EVs) and residential energy products—are repealed so they no longer apply beyond this year, while most others are restricted or phased out on an accelerated schedule over the next few years. However, the law expands the carbon oxide sequestration credit and extends the clean fuel production tax credit, while introducing additional compliance challenges for many credits.

The administration is now working through regulatory guidance and interpretation for businesses planning to take the expiring credits over the next two years, which will require close monitoring by taxpayers who desire to comply with the tax law while also claiming residual credits prior to their expiration.

The OBBBA makes many permanent changes to international tax policy, notably by canceling the larger scheduled tax increases built into the tax code in 2026 and keeping the effective tax rates on international income closer to current policy values.

The law restructures the tax on global intangible low-taxed income (GILTI) and the deduction for foreign-derived intangible income (FDII) by repealing the deduction for qualified business asset investment (QBAI). Repealing QBAI effectively raises taxes on physical capital deployed abroad by US firms, while lowering taxes on capital in the US used for exports.

The law also makes a variety of small “bug fixes”: changes that greatly simplify at small cost, clarify longstanding issues, or remove unintended consequences. This includes adjustments to expense allocation, a partial fix to the foreign tax credit haircut, and making the “look through” tax rule permanent policy.

As part of the process, the administration also successfully negotiated the US international tax system to be acknowledged as compliant with the Organisation for Economic Co-operation and Development’s (OECD) Pillar Two minimum tax rules, preventing the inclusion of retaliatory tax rules in OBBBA that would have harmed foreign investment.

The new law increases the existing excise tax on the net investment income of certain colleges and university endowments. Prior law imposed a 1.4 percent excise tax on universities with more than 500 students and an endowment worth $500,000 per student.

Under OBBBA, universities will face a graduated set of tax rates up to 8 percent on net investment income for all institutions that hold at least $500,000 per student in endowment and have at least 3,000 students in the tax year. According to one estimate from scholars at AEI, “The average endowment eligible for the tax earned roughly 6.6 percent of its total value in annual taxable income.”

Impact

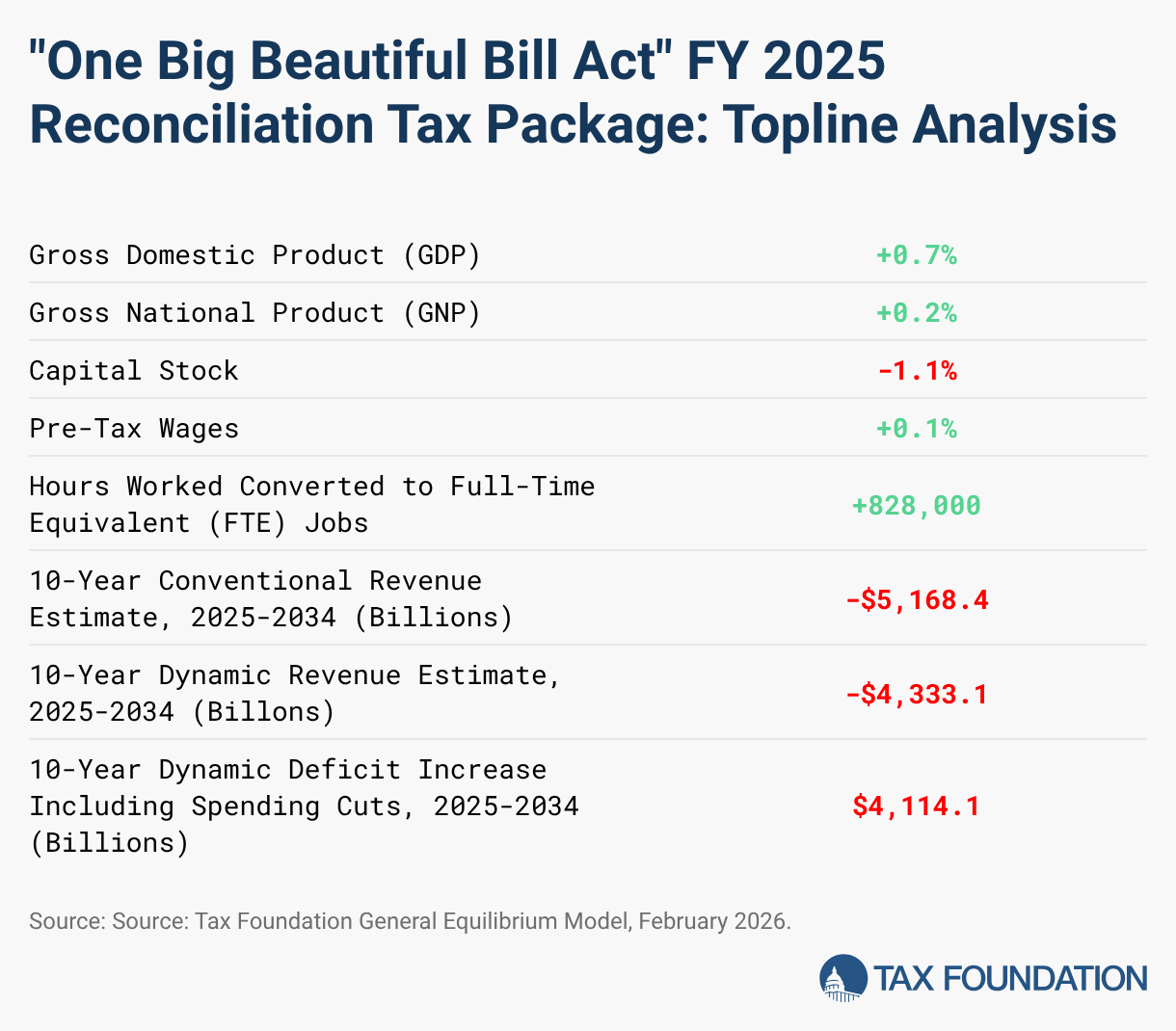

We estimate the major tax provisions we modeled lower marginal tax rates on work, saving, and investment in the United States, leading to a 1.2 percent expansion in the size of the long-run economy, a 0.7 percent increase in the capital stock, a 0.4 increase in pre-tax wages, and an increase in hours worked equivalent to 938,000 full-time jobs.

Though economic output, as measured by gross domestic product (GDP), would expand due to increased incentives to work, save, and invest, American incomes, as measured by gross national product (GNP), would not rise to the same degree. The law would increase federal borrowing by pushing deficits $3.8 trillion higher (including added interest costs, on a dynamic basis) over the next decade, and increased foreign claims on future US output would reduce American incomes by nearly 0.6 percent, leaving American incomes 0.9 percent higher.

We estimate the major tax provisions modeled will reduce federal revenues by $5.0 trillion between 2025 and 2034. Most of the revenue reduction comes after 2025, when the major provisions of the TCJA are scheduled to sunset.

On a dynamic basis, incorporating the projected increase in long-run GDP of 1.2 percent, the revenue loss falls by about 19 percent, or $940 billion, to $4.1 trillion over the 10-year budget window.

Incorporating the Congressional Budget Office (CBO) estimates of changes in non-interest spending, which total nearly $1.1 trillion over the decade, the OBBBA will increase deficits by $3.0 trillion from 2025 through 2034 on a dynamic basis, before added interest costs.

We estimate additional borrowing due to higher deficits will increase interest costs by $917 billion on a conventional basis or by $725 billion on a dynamic basis. Incorporating the changes in interest spending, the OBBBA will increase total deficits over the 2025 through 2034 budget window by $4.9 trillion on a conventional basis or by $3.8 trillion on a dynamic basis.

We estimate the law would increase average after-tax incomes for taxpayers by 2.9 percent in 2025 and 5.4 percent in 2026. The income increase is higher in 2026 because the TCJA individual tax provisions are not scheduled to expire until after the end of 2025.

Because several tax cuts are available only on a temporary basis, the law would raise market incomes by a smaller 2.8 percent in 2034. However, factoring in the economic growth driven by the plan’s permanent provisions, the law would raise market incomes by 3.6 percent in 2034 on a dynamic basis.

Middle-income quintiles see the largest income increases in 2026 due to the combination of the individual TCJA extensions and the handful of targeted tax breaks for specific types of income, like overtime and tips as well as the bonus deduction for seniors (which provide large tax reductions to targeted groups of taxpayers in the middle quintile).

Meanwhile, larger after-tax incomes in 2034 are attributable to the permanent individual cuts from TCJA, permanent enhancements of certain provisions, and permanent expensing for equipment and R&D investment.

After-tax income for the bottom quintile in 2034 falls by 0.4 percent on a conventional basis as tighter rules for premium tax credits, the earned income tax credit (EITC), and the child tax credit (CTC) take effect. However, after accounting for economic growth, after-tax income for the bottom quintile increases by 0.5 percent in 2034.

Preliminary Distributional Effects of Major Provisions in the One Big Beautiful Bill Act

| Market Income Percentile | 2025, Conventional | 2026, Conventional | 2034, Conventional | 2034, Dynamic |

|---|---|---|---|---|

| 0% - 20.0% | 1.5% | 2.6% | -0.4% | 0.5% |

| 20.0% - 40.0% | 3.1% | 5.2% | 1.9% | 2.7% |

| 40.0% - 60.0% | 3.6% | 5.7% | 2.7% | 3.5% |

| 60.0% - 80.0% | 3.9% | 6.3% | 2.8% | 3.5% |

| 80.0% - 100% | 2.3% | 5.0% | 2.9% | 3.8% |

| 80.0% - 90.0% | 3.7% | 5.7% | 2.5% | 3.3% |

| 90.0% - 95.0% | 1.9% | 4.4% | 3.0% | 3.8% |

| 95.0% - 99.0% | 1.5% | 4.8% | 3.5% | 4.3% |

| 99.0% - 100% | 2.1% | 5.0% | 2.7% | 3.6% |

| Total | 2.9% | 5.4% | 2.8% | 3.6% |

Source: Tax Foundation General Equilibrium Model, June 2025.

The OBBBA is estimated to increase long-run GDP by 1.2 percent, while increasing the deficit on a conventional basis by $4.0 trillion (accounting for spending cuts but excluding interest costs) from 2025 to 2034. Accounting for the effects of economic growth reduces the deficit impact (excluding interest costs) to $3 trillion over that period. Altogether, the tariffs imposed and threatened by the Trump administration are estimated to offset a little more than half the cost of the OBBBA on a dynamic basis and reduce the net long-run economic growth effects to 0.4 percent.

If the tariffs in effect today are left in place permanently, they will reduce long-run GDP by 0.5 percent before retaliation, while raising about $2.1 trillion in revenue from 2025 through 2034 on a conventional basis.

If the reciprocal tariffs and the Section 232 copper tariff take effect on August 1 as scheduled, they will reduce GDP by an additional 0.3 percent while raising $401 billion in additional revenue (a relatively small increase as imports would fall substantially under those rates).

In total, before accounting for retaliation, the tariffs imposed and threatened will reduce long-run GDP by 0.8 percent, raising about $1.7 trillion in revenue from 2025 through 2034, measured on a dynamic basis, accounting for slower economic growth.

The Trump tariffs threaten to offset much of the economic benefits of the new tax cuts, while falling short of paying for them. We estimate that current US-imposed and scheduled tariffs will undermine two-thirds of the OBBBA’s 1.2 percent boost in long-run GDP while offsetting only about half the cost of the OBBBA (on a dynamic basis and before retaliation). Low-income taxpayers would be worse off under the combination of tariffs and the OBBBA by the end of the budget window.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe