The One Big Beautiful Bill Act (OBBBA) makes the expiring taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities. cuts from the 2017 Tax Cuts and Jobs Act (TCJA) permanent, along with several other changes to the tax code. While Congress worked on the OBBBA to cut taxes, President Trump imposed significantly higher taxes by placing tariffs on more than half of US imports. The tariffs now in effect threaten to offset much of the GDP growth from the tax cuts, while falling short of paying for them.

As of February 25, the tariffs currently in effect include a temporary Section 122 tariffTariffs are taxes imposed by one country on goods imported from another country. Tariffs are trade barriers that raise prices, reduce available quantities of goods and services for US businesses and consumers, and create an economic burden on foreign exporters. of 10 percent on about 34 percent of US goods imports and several Section 232 tariffs, including a 50 percent tariff on steel and aluminum, a 25 percent tariff on most autos and auto parts, and other sector-specific tariffs.

If the Section 232 tariffs in effect today are left in place permanently, we estimate they would reduce long-run GDP by 0.2 percent before retaliation, while raising about $635 billion in revenue from 2026 through 2035 on a conventional basis, or $490 billion on a dynamic basis, accounting for the GDP effect. The Section 122 tariff is scheduled to expire after 150 days and thus would not have any long-run economic impact. The Section 122 tariff would raise $25 billion in 2026.

We estimate the OBBBA will increase long-run GDP by 0.7 percent, while reducing revenue by $5.2 trillion from 2025 to 2034 on a conventional basis, or by $4.3 trillion on a dynamic basis, accounting for the GDP effect. Incorporating the CBO’s estimates of changes in non-interest spending, which total nearly $1.1 trillion of spending cuts over the decade, the OBBBA will increase deficits by $4.1 trillion on a conventional basis, or by $3.3 trillion from 2025 through 2034 on a dynamic basis, before added interest costs.

Altogether, we estimate tariffs offset a little less than one-third of the long-run economic effect of the OBBBA while paying for less than half its cost.

Table 1. Summary of Tariffs an the One Big Beautiful Bill Act

| One Big Beautiful Bill Act | Tariffs in Effect Feb. 25, 2026, Before Retaliation | |

|---|---|---|

| GDP | +0.7% | -0.2% |

| Capital Stock | -1.1% | -0.1% |

| Hours Worked in FTEs | 828,000 | -154,000 |

| Conventional Deficit Change, Before Interest Costs, 2025-2034, Billions | $4,100.0 | -$660.2 |

| Dynamic Deficit Change, Before Interest Costs, 2025-2034, Billions | $3,262.8 | -$514.9 |

Note: Totals may not sum exactly due to rounding.

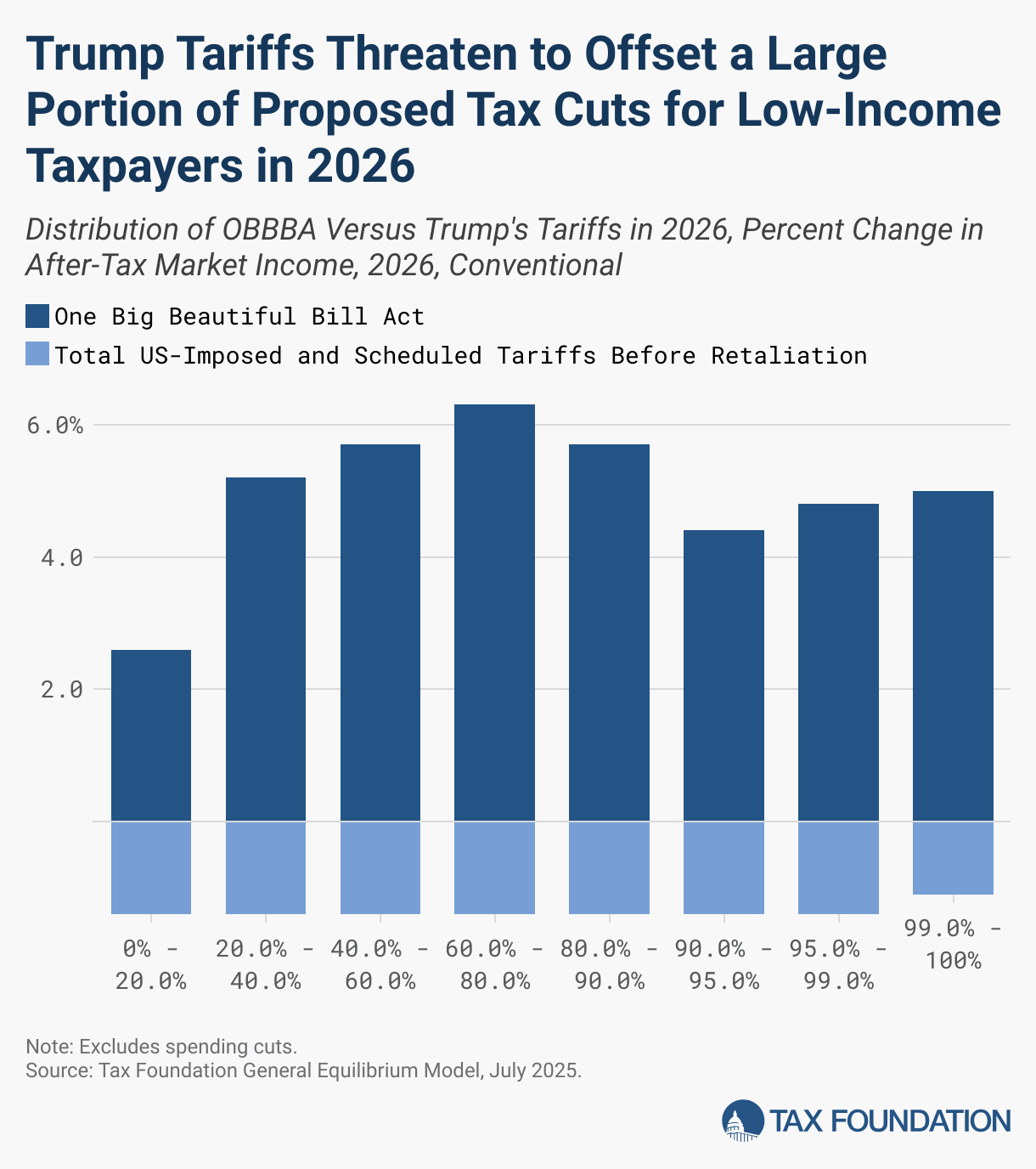

Because the combination of the OBBBA’s tax provisions and Trump’s tariffs significantly reduces federal taxes, it results in net tax cuts on average. But the effects are not the same across the income spectrum.

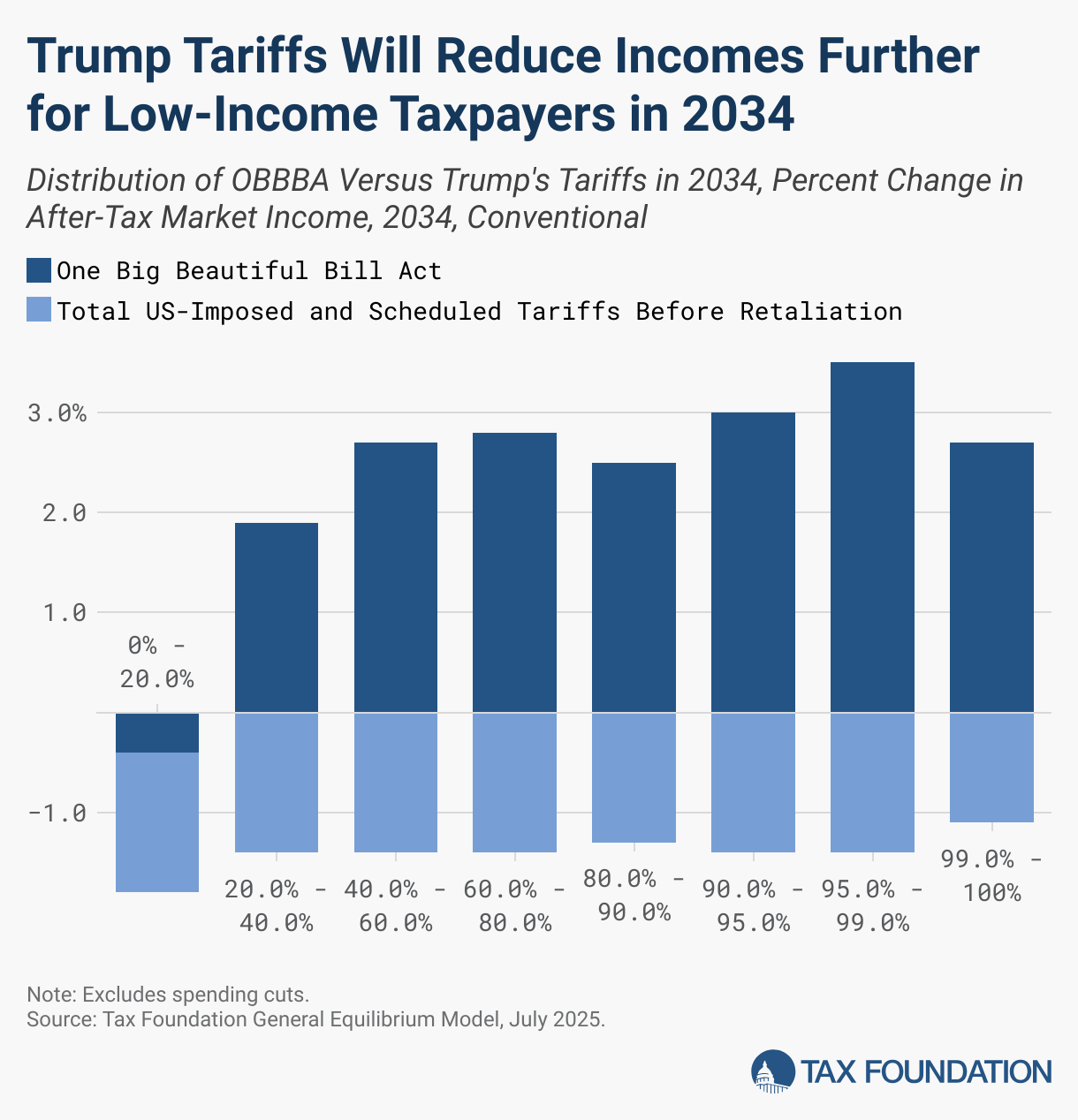

The tariffs offset a larger portion of the tax cuts for lower- and middle-income taxpayers than for higher-income taxpayers. Because several of the OBBBA’s tax provisions expire at the end of 2028, by 2034, the bottom quintile will actually see a net reduction in after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings. under the OBBBA on a conventional basis, which would be exacerbated by the tariffs if they remain in place in 2034. Note also that these estimates do not include the distribution effects of the spending cuts, which would further reduce after-tax income for the bottom quintile.

Percent Change in After-Tax Income Under OBBBA and Tariffs in 2026

| Market Income Percentile | OBBBA 2026, Conventional, | Tariffs, 2026, Conventional |

|---|---|---|

| 0% - 20.0% | 1.8% | -0.5% |

| 20.0% - 40.0% | 3.2% | -0.5% |

| 40.0% - 60.0% | 3.3% | -0.5% |

| 60.0% - 80.0% | 3.8% | -0.5% |

| 80.0% - 100% | 4.4% | -0.5% |

| 80.0% - 90.0% | 3.5% | -0.5% |

| 90.0% - 95.0% | 4.1% | -0.5% |

| 95.0% - 99.0% | 4.8% | -0.5% |

| 99% - 99.9% | 4.9% | -0.4% |

| 99.9% - 100% | 5.9% | -0.4% |

Stay informed on the tax policies impacting you.

Subscribe to our free newsletter to get the latest tax data, news and analysis.

Subscribe