Wisconsin‘s tax system ranks 19th overall on the 2025 State Tax Competitiveness Index. Wisconsin maintains competitive sales and property tax structures but ranks near the middle of the pack overall due to burdensome taxes on labor and investment.

Wisconsin does not offer first-year expensing for machinery and equipment investments, and its imposition of a throwback rule exposes an outsized share of in-state businesses’ income to the state’s high 7.9 percent corporate income tax rate. While lawmakers have reduced the state’s lower marginal individual income tax rates in recent years, Wisconsin is one of the only income tax-cutting states that stopped short of reducing its top marginal rate. At 7.65 percent, Wisconsin’s top marginal rate is high both regionally and nationally, putting the state’s pass-through businesses at a competitive disadvantage compared to several regional competitors that levy low, flat rates. While the marriage penalty in Wisconsin’s brackets is partially offset by a married couple credit, the credit is an imperfect solution, adding to the tax code’s complexity and creating a marriage bonus in some situations while leaving taxpayers with a marriage penalty in others.

Despite these shortcomings, Wisconsin ranks in the top half of states due to its relatively well-structured sales and property taxes. Wisconsin’s combined state and average local sales tax rate is among the lowest in the country, and its uniform state and local sale tax base, unified administration of sales taxes at the state level, and relatively low excise taxes put Wisconsin’s sales tax system in the top 10.

Wisconsin also outperforms many of its peers in its uniform application of the property tax across various classes of property, which is constitutionally required under the state’s Uniformity Clause, as well as in its recent decision to repeal the tangible personal property tax in its entirety. Moving forward, Wisconsin lawmakers could promote stronger economic growth in the Badger State by prioritizing reforms that improve individual and corporate income tax structure.

With reports that Republican legislative leaders and Wisconsin Gov. Evers (D) have reached a budget deal for FY 2026 and 2027, it is worth examining two significant tax relief proposals included in the plan.

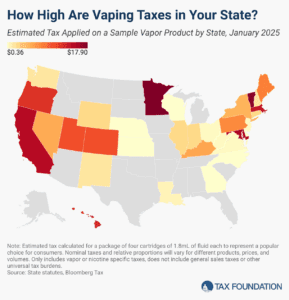

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.

The Senate’s version of the OBBB restores the benefit of avoiding the SALT deduction cap with PTETs for all pass-through businesses, while placing new limits on the extent of the workarounds.