Washington forgoes an individual income tax on wage income due to constitutional constraints, though the state recently imposed a tax on high earners’ capital gains income, a policy that raised constitutional questions but ultimately secured the assent of the state supreme court. It became a graduated rate tax in 2025, with a top rate of 9.9 percent for gains above $1 million. The constitution has been similarly interpreted as blocking a corporate income tax, but Washington instead imposes a high multiple-rate gross receipts tax, called the Business & Occupation Tax. Because it is based on gross revenues rather than net income (profits), it yields very high rates of taxation on low-margin businesses and leads to tax pyramiding, where goods and services have the tax embedded several times over, imposed on each transaction within the production process.

The state’s sales tax, imposed atop the gross receipts tax, is not just a high rate but is also imposed on a base that includes an unusual share of business inputs, particularly in the digital products space. In 2025, lawmakers adopted legislation further expanding digital products taxation and notably including digital advertising in the base, which raises legal concerns along with economic ones. Washington also levies a progressive real estate transfer tax and the nation’s highest-rate estate tax, with the top rate raised to 35 percent in 2025, rivaling the 40 percent top federal rate. High UI taxes and an uncompetitive UI tax structure also contribute to the state’s poor Index ranking despite the state forgoing an individual income tax, which might otherwise be expected to yield a much more competitive tax environment.

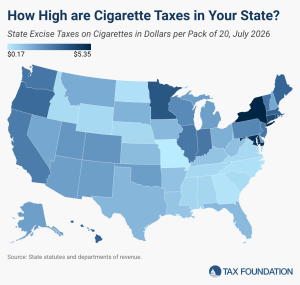

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.