Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readSouth Dakota is one of only two states to forgo individual income, corporate income, and gross receipts taxes. Consequently, the state relies heavily on its sales tax, which nevertheless retains a highly competitive rate, though one imposed on an overbroad base. It applies to most final personal consumption—which is appropriate—but also to a wide range of business inputs, which causes harmful tax pyramiding.

South Dakota relies on relatively high property taxes to fund local government, but the property tax base is competitive in that the property tax does not apply to tangible personal property or business inventory. Furthermore, the property tax applies to all classes of property uniformly, which is important for maintaining neutrality and preventing distortions, and the state does not have an estate or inheritance tax.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 2 | 0 | 7.71 |

| Corporate Taxes | 1 | 0 | 10.00 |

| Individual Income Taxes | 1 | 0 | 10.00 |

| Sales Taxes | 31 | 0 | 4.51 |

| Property Taxes | 8 | 3 | 5.94 |

| Unemployment Insurance Taxes | 20 | 1 | 5.32 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

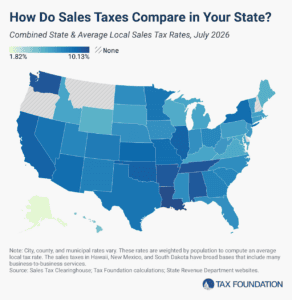

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read