Sales Tax Holidays by State, 2026

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min readOhio is an outlier in its reliance on a gross receipts tax, the Commercial Activity Tax (CAT), as its primary business tax. Gross receipts taxes are generally more economically harmful than corporate income taxes because they apply to firms regardless of whether they earn a profit in a given year, and they cause harmful tax pyramiding, because this results in the same final good or service being taxed at multiple points along the production process.

Notably, however, Ohio’s CAT is imposed at a low 0.26 percent rate and was adopted as a replacement for a corporate income tax, a capital stock tax, and the tangible personal property tax, so despite its structural shortcomings, its adoption represented a meaningful tax cut for many businesses. In 2025, Ohio’s CAT exclusion was doubled to $6 million. Ohio ranks well on the property tax component, bolstered by its uniform assessment of different classes of property, its lack of tangible personal property taxes, and its lack of an estate or inheritance tax.

In recent years, Ohio has adopted significant individual income tax relief, lowering the top rate to 2.75 percent as of 2025. This has helped the state’s individual tax component score, but high-rate income taxes levied at the local level increase tax costs and compliance burdens for residents and nonresidents, especially since nonresident filing and withholding are required for many individuals who work even a single day in the state.

| Category | Rank | Rank Change | Score |

|---|---|---|---|

| Overall | 39 | 0 | 4.78 |

| Corporate Taxes | 45 | 0 | 3.96 |

| Individual Income Taxes | 33 | 2 | 4.91 |

| Sales Taxes | 44 | -1 | 3.97 |

| Property Taxes | 5 | 0 | 6.15 |

| Unemployment Insurance Taxes | 11 | 2 | 5.66 |

Get facts about taxes in your state and around the US

However well-intended they may be, sales tax holidays remain the same as they always have been—ineffective and inefficient.

12 min read

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.

7 min read

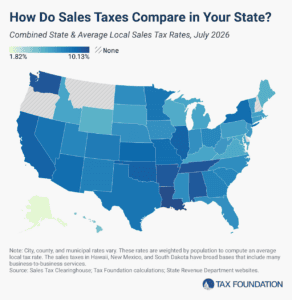

The five states with the highest average combined state and local sales tax rates are Louisiana (10.13 percent), Tennessee (9.61 percent), Washington (9.57 percent), Arkansas (9.48 percent), and Alabama (9.46 percent).

8 min read