New Mexico has a graduated state individual income tax with a top rate of 5.9 percent. A new lower-rate bracket was created in 2025, though the top rate was left untouched. Also in 2025, New Mexico replaced its graduated-rate corporate income tax with a top rate of 5.9 percent to a single-rate tax of 5.9 percent on all income, a relatively rare case of a corporate income tax rate increase in recent years.

New Mexico also has a 4.875 percent tax on sales, with an average combined state and local rate of 7.67 percent. As a hybrid between an ordinary sales tax and a gross receipts tax, this tax does not apply to all intermediate transactions like a pure gross receipts tax but does apply to many more business inputs than are included in a typical sales tax, including manufacturing machinery and research and development (R&D) equipment. When this gross receipts-like tax applies to business-to-business transactions, it causes tax pyramiding throughout the supply chain, hampers investment, and negatively affects low-margin businesses.

The state’s corporate income tax also features a throwback rule, which exposes in-state businesses to additional tax when they sell into other states with which they do not have nexus, discouraging some businesses from locating operations in New Mexico. The state conforms to the federal treatment of capital investment under its corporate income tax.

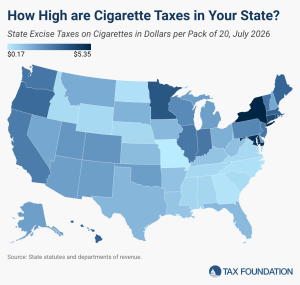

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.