Nebraska has taken strides to improve its income tax competitiveness in recent years by reducing its individual and corporate income tax rates. Currently, the state’s graduated individual income tax rates range from 2.46 percent to 5.84 percent, and its corporate income tax rate is now a flat 5.2 percent. Despite these improvements, Nebraska maintains an uncompetitive “convenience of the employer rule,” which can lead to double taxation (with no offsetting credit) for remote employees working for businesses located in Nebraska—ultimately a disincentive for businesses to locate in the state if they want to be able to hire across the country. Nebraska also requires individual income tax filing and withholding for nonresidents working even a single day in the state.

Notably, Nebraska’s property taxes are on the high side regionally and nationally, and Nebraska is one of the few states that continues to impose an antiquated capital stock tax, which is assessed against the net worth of Nebraska corporations and imposed regardless of whether a firm makes a profit. The Nebraska Occupation Tax, as it is known in the state, is collected every other year, which complicates the filing process, since firms must track their net worths across two tax years. Nebraska also retains an inheritance tax, albeit on a declining share of beneficiaries, and is the only state to have adopted but then abandoned a tangible personal property tax de minimis exemption.

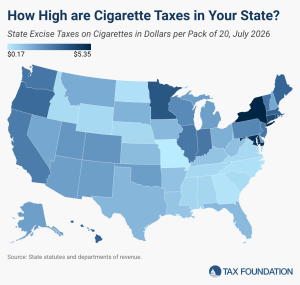

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.