Maryland’s tax code is complex and includes all major tax types. The state has traditionally ranked among the bottom 10 states on the Index. Maryland has a progressive individual income tax system. Legislation retroactive to January 1, 2025, increased the state’s individual tax progressivity by expanding to 10 tax brackets, creating a new top marginal tax rate of 6.5 percent, and establishing a 2 percent capital gains surcharge for individuals with federal AGI exceeding $350,000. High-rate county income taxes, with new rates up to 3.3 percent, yield a substantially above-average income tax burden for Maryland residents.

The state’s corporate income tax rate is 8.25 percent, considerably higher than regional competitors Virginia and West Virginia. Like DC, Maryland has included global intangible low-taxed income (GILTI) in its corporate tax base, making it an outlier nationwide, and under the One Big Beautiful Bill Act, the taxation of GILTI converts to taxation of net CFC-tested income (NCTI) and further increases state tax liability. The state does not allow full expensing within its corporate income tax. Unusually, Maryland also limits first-year expensing for pass-through businesses to $25,000 in annual expenses, whereas most states offer $1 million. However, Maryland does not impose harmful gross receipts or capital stock taxes and has a competitive sales tax system with a general rate of 6 percent.

In addition to complexities with traditional taxes, Maryland is currently the only state to impose a digital advertising tax, which is nonneutral, difficult to comply with, and subject to numerous legal disputes. Maryland is also the only state that imposes both estate and inheritance taxes, with maximum rates of 16 and 10 percent, respectively, making the state less attractive for high-net-worth individuals. These factors further exacerbate Maryland’s relatively poor tax competitiveness. Finally, the 2025 budget adopted a new 3 percent tax on a range of business digital products, further undercutting the state’s competitiveness.

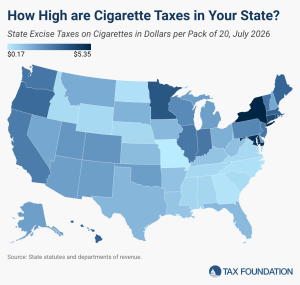

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.