Connecticut’s tax code includes all major tax types, and the state has historically ranked among the bottom 10 on the Index. Connecticut has one of the most complex and least neutral individual income tax systems in the nation, featuring seven tax brackets with a top marginal rate of 6.99 percent and a recapture provision that eliminates the benefit of lower brackets, effectively taxing all income at the taxpayer’s highest marginal rate. Additionally, tax brackets and the personal exemption are not adjusted for inflation.

Connecticut’s baseline corporate income tax rate is high at 7.5 percent, though still lower than in other New England states, such as Massachusetts and Delaware. However, the state imposes a 10 percent surtax on businesses with gross proceeds of $100 million or more, or those filing as part of a combined unitary group, which increases the total tax burden for large corporations. The state does not comply with federal bonus depreciation treatment, requiring businesses to add back any first-year expensing of capital investment taken at the federal level. A minimum tax is also imposed on corporations’ capital stock. This provision was slated for expiration, but the phaseout has now been extended until 2028. Connecticut does, however, offer appropriate treatment of net operating loss carryforwards and forgoes a harmful throwback rule.

The state’s sales tax rate of 6.35 percent is competitive both nationally and regionally, but the base includes some business inputs and excludes many final consumption goods and services, which limits the revenue-generating potential and reduces the neutrality of the sales tax system.

Connecticut also has one of the highest property tax burdens in the nation (relative to personal income) and imposes harmful estate and gift taxes, making the state less attractive to homeowners and high-net-worth individuals.

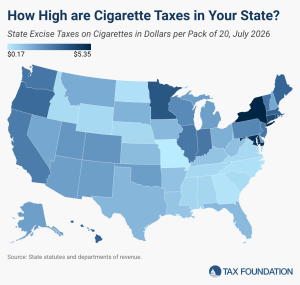

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.