Arkansas ranks poorly on the Index despite multiple rounds of income tax rate reductions since 2015 and a resulting low top marginal individual income tax rate, due to a range of structural shortcomings in the state’s tax code. For instance, Arkansas only allows corporations’ net operating losses (NOLs) to be carried forward for 10 years, while most states either allow 20-year or uncapped carryforward periods. Arkansas also imposes a throwback rule, exposing some out-of-state activity of Arkansas-based corporations to the state’s corporate taxes, which increases their tax liability. Throwback rules penalize firms’ investments and instead incentivize them to relocate to states without these rules.

The state stands alone in having two different income tax rate schedules depending on taxpayer income.

Arkansas has the third-highest combined state and local sales tax rate in the nation at 9.48 percent. The state also imposes a tax on capital stock, at 0.3 percent of the apportioned net worth of corporations. Such taxes are increasingly rare, and Arkansas’s tax rate is the highest in the nation. The state also assesses property tax on businesses’ inventory, making the state even more of an outlier. Both taxes are assessed whether the firm makes a profit or loss in a particular tax year, which is harmful to small businesses seeking to scale up their operations, capital-intensive firms, and all firms during an economic decline. Finally, Arkansas offers no de minimis exemption for its tax on tangible personal property, making this tax exceptionally burdensome to small businesses.

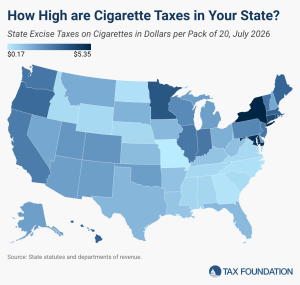

The highest state tax on cigarettes is levied by New York at $5.35 per pack of 20. The next highest tax jurisdiction is the District of Columbia at $5.07 per pack of cigarettes, followed closely by Maryland at $5.00 per pack, Rhode Island at $4.50 per pack, and Connecticut at $4.35 per pack.

Policymakers are increasingly considering taxes on data processing and other businesses’ digital services, but these taxes increase costs at many stages of the production process for virtually all businesses, not just tech-oriented businesses.