South Dakota‘s tax system ranks 2nd overall on the 2025 State Tax Competitiveness Index. South Dakota is one of only two states to forgo individual income, corporate income, and gross receipts taxes. Consequently, the state relies heavily on its sales tax, which nevertheless retains a highly competitive rate, though one imposed on an overbroad base. It applies to most final personal consumption—which is appropriate—but also to a wide range of business inputs, which causes harmful tax pyramiding.

South Dakota relies on relatively high property taxes to fund local government, but the property tax base is competitive in that the property tax does not apply to tangible personal property or business inventory. Furthermore, the property tax applies to all classes of property uniformly, which is important for maintaining neutrality and preventing distortions, and the state does not have an estate or inheritance tax.

Summer has arrived, and states are beginning to implement policy changes that were enacted during this year’s legislative session (or that have delayed effective dates or are being phased in over time).

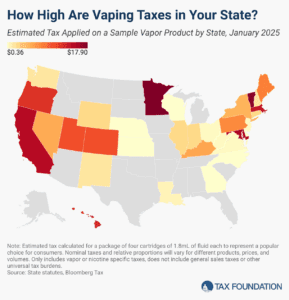

The vaping industry has grown rapidly in recent decades, becoming a well-established product category and a viable alternative to cigarettes for those trying to quit smoking. US states levy a variety of tax structures on vaping products.

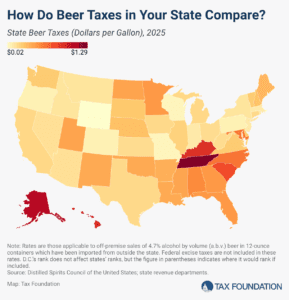

In the United States, taxes are the single most expensive ingredient in beer. The tax burden accounts for more of the final price of beer than labor and materials combined—the many different layers of applicable taxes combining to total as much as 40.8 percent of the retail price.